“New investors will fully share in Google’s long term economic future but will have little ability to influence its strategic decisions through their voting rights,” wrote Larry Page and Sergei Brin in their famous “2004 Founders’ IPO Letter.”1

Nearly 15 years after Google’s initial public offering, the debate about listed companies that offer unequal voting rights to outside investors rages on. A number of high-profile technology companies including Dropbox Inc., Spotify and Snap Inc. have recently listed shares with unequal voting rights, adding fuel to the debate.2 Meanwhile, investors are trying to determine if they should shun the stock issued by these companies or include them in equity portfolios.

Company founders argue that retaining superior voting power protects them from market pressure to deliver short-term results, allowing them to focus on long-term performance. Equity investors counter that voting power enables them to express their views and participate in important corporate governance decisions.3 Caught between the two are stock exchanges and index providers. Exchanges are increasingly under pressure to relax listing requirements as they compete to include companies looking to keep voting power in the hands of insiders after they go public.4 Index providers are considering whether voting power should become a criterion for index inclusion, to help ensure that indexed investors can express their views through engagement and voting.5

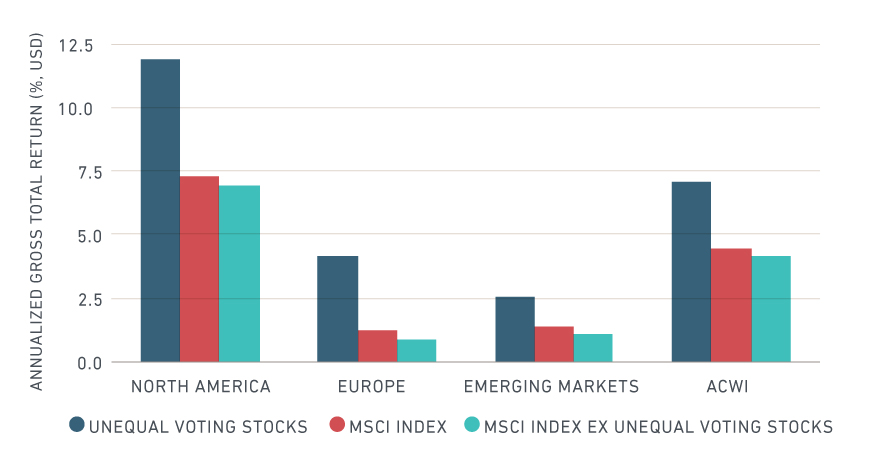

Unequal voting stocks have outperformed

Our research shows that unequal voting stocks in aggregate outperformed the market over the period from November 2007 to August 2017, and that excluding them from market indexes would have reduced the indexes' total returns by approximately 30 basis points per year over our sample period. In this blog post, we examine the characteristics of unequal voting stocks across global equity markets to determine what was behind their outperformance. Do unequal voting stocks, as a group, share common characteristics that affect their performance? We observe some commonality in the country, sector and style factor exposures of these stocks. However, we find that these common characteristics only partially explained performance, while stock-specific effects had a greater impact.

Performance of MSCI Indexes and unequal voting stocks

Data from November 2007 to August 2017

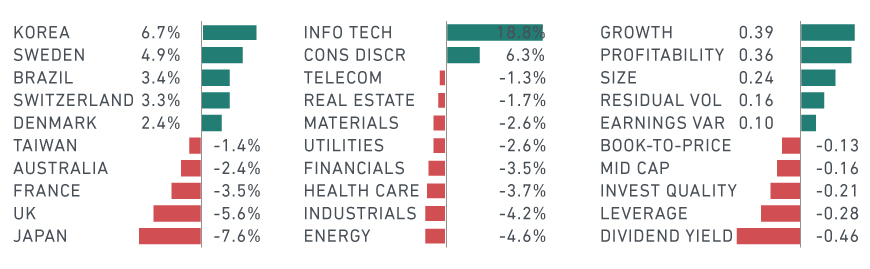

A closer look at unequal voting stocks

The MSCI ACWI Index, which covers both developed and emerging markets, contained 243 stocks with unequal voting rights6 out of a total of 2,493 index constituents as of September 2017; that is, 11.2% of the index. The five largest companies on this list were Alphabet, Facebook, Berkshire Hathaway, Samsung and Visa. In the exhibit below, we compare the country, sector and style factor characteristics of the float-market-cap-weighted portfolio of unequal voting stocks against the MSCI ACWI Index.

Top 10 country, sector and factor exposures of unequal voting stocks vs. MSCI ACWI Index

Data as of Sept. 1, 2017

The largest country overweights were in Korea and Sweden, while the largest underweights were in Japan and the U.K. In terms of sectors, we observe substantial overweights in information technology and in consumer discretionary. The factor analysis shows that unequal voting stocks had high growth and profitability and were relatively large, but also had higher earnings variability and higher stock-specific risk.7 What’s more, these companies experienced faster asset growth, were less leveraged and offered lower dividend yield compared to other companies in the MSCI ACWI Index.

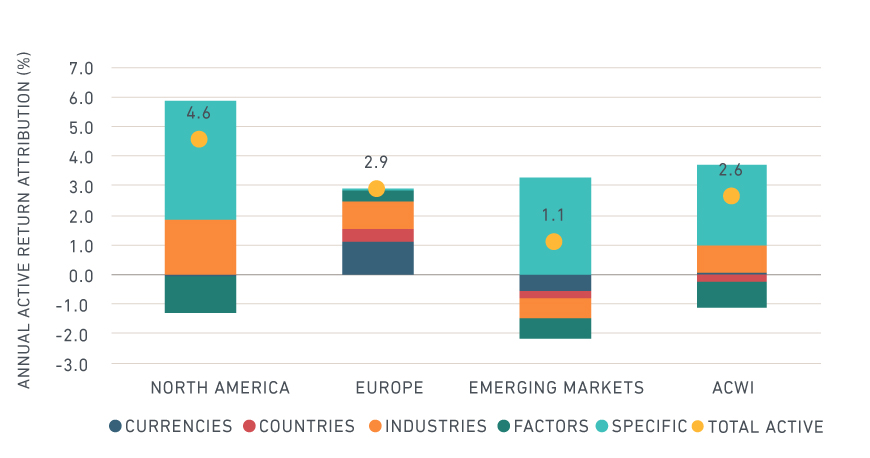

Why unequal voting stocks have outperformed

Did unequal voting stocks outperform because of their country, sector and factor characteristics? For example, did the substantial overweight in information technology explain most of the relative performance? Or did company-specific characteristics explain the good performance of these stocks? Our analysis, shown in the next exhibit, reveals that common characteristics accounted for some, but not all, of the outperformance of unequal voting stocks. In fact, the majority of outperformance was due to company-specific effects, though the degree varied in different regions.

In North America, where unequal voting stocks outperformed by 4.5% annually, stock-specific effects accounted for 4% (with sectors adding 2% and style factors detracting about 1.5% per year), while in emerging markets all of the outperformance was attributed to stock-specific influences. Europe was the exception, where all of the outperformance of unequal voting stocks was due to exposure to common factors.

What drove the performance of unequal voting stocks?

Data covers the period from November 2007 to August 2017

What’s next?

The outperformance of stocks with unequal voting rights was partly explained by the fact that the technology sector, in general, enjoyed strong performance over the period we examined, and many unequal voting stocks were issued by technology companies. However, given the fact that most of the difference in performance was due to company-specific effects, we ask: Are companies with unequal voting rights better managed because of concentrated voting power or in spite of it? Could voting power become a new risk and performance factor? These are questions that investors will increasingly confront if companies continue to come to market with unequal voting.

The author thanks Roman Kouzmenko for his contributions to this blog post.

1 https://abc.xyz/investor/founders-letters/2004/ipo-letter.html

2 “Dropbox IPO is yet another corporate governance low point.” Financial Times, March 19, 2018, https://www.ft.com/content/4333c554-279a-11e8-b27e-cc62a39d57a0

3 https://www.cii.org/dualclass_stock

4 “Hong Kong and Singapore succumb to the lure of dual-class shares.” The Economist, March 10, 2018

5 “Should equity indexes include stocks of companies with share classes having unequal voting rights?”

6 For a precise definition of voting rights, see “Should Equity Indexes Include Stocks of Companies with Share Classes having Unequal Voting Rights?”

7 For more detailed risk analysis of the basket of unequal voting stocks, please see the above paper.