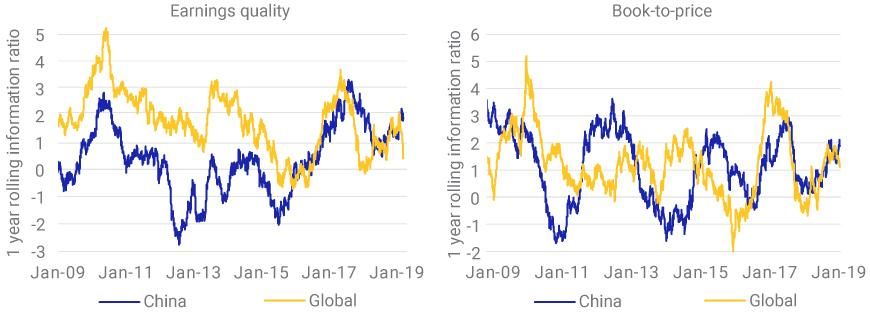

The rise of fundamental factors in China A shares

- Our research suggests fundamental factors gained traction in China-A-share strategies.

- For factors such as value and quality, risk-adjusted returns for China A shares and global equities converged over the last two years.

- Institutional investors' increased presence likely helped to tip the scales away from local, sentiment-driven retail investors.

2018 | Unnamed: 1 | Unnamed: 2 | 2019 year to date | Unnamed: 4 |

|---|---|---|---|---|

2018 Dividend Yield | Unnamed: 1 2.4 | Unnamed: 2 None | 2019 year to date Momentum | Unnamed: 4 1.33 |

2018 Investment Quality | Unnamed: 1 2.27 | Unnamed: 2 None | 2019 year to date Earnings Variability | Unnamed: 4 1.18 |

2018 Book-to-Price | Unnamed: 1 1.59 | Unnamed: 2 None | 2019 year to date Beta | Unnamed: 4 0.91 |

2018 Profitability | Unnamed: 1 1.41 | Unnamed: 2 None | 2019 year to date Book-to-Price | Unnamed: 4 0.77 |

2018 Earnings Quality | Unnamed: 1 1.4 | Unnamed: 2 None | 2019 year to date Earnings Quality | Unnamed: 4 0.45 |

2018 Long-Term Reversal | Unnamed: 1 1.27 | Unnamed: 2 None | 2019 year to date Investment Quality | Unnamed: 4 0.11 |

2018 Beta | Unnamed: 1 1.24 | Unnamed: 2 None | 2019 year to date Long-Term Reversal | Unnamed: 4 0.03 |

2018 Momentum | Unnamed: 1 0.57 | Unnamed: 2 None | 2019 year to date Liquidity | Unnamed: 4 0.02 |

2018 Leverage | Unnamed: 1 0.53 | Unnamed: 2 None | 2019 year to date Dividend Yield | Unnamed: 4 0.01 |

2018 Size | Unnamed: 1 0.05 | Unnamed: 2 None | 2019 year to date Growth | Unnamed: 4 -0.1 |

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.