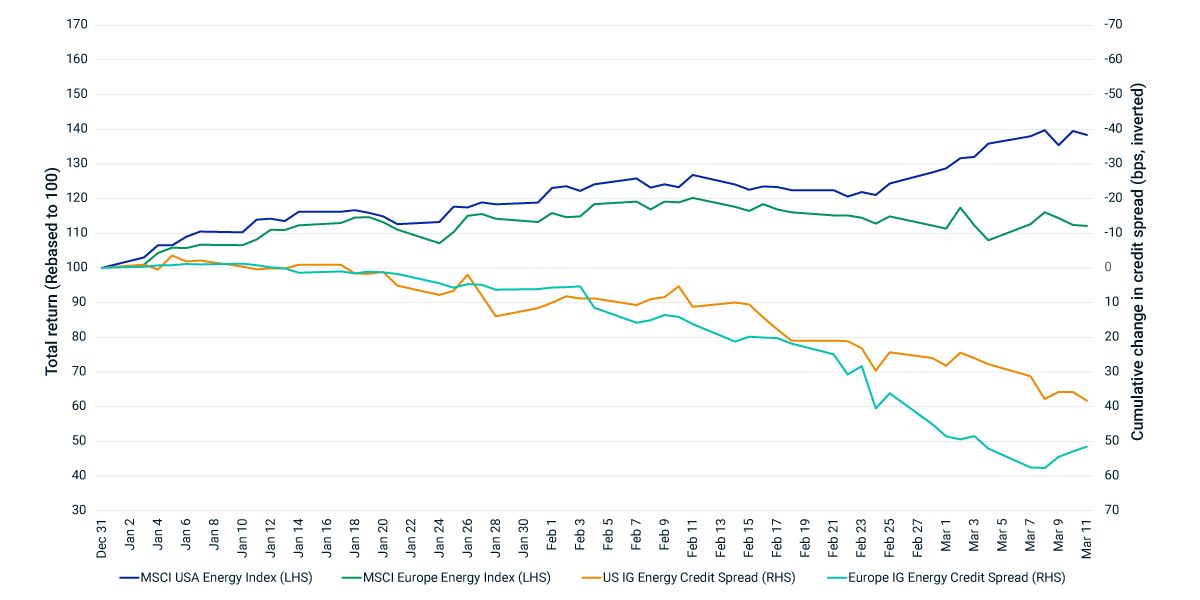

Higher Energy Prices Fueled Equities More than Bonds

Higher energy prices have benefited developed-market energy-sector equities, generally, as illustrated by the fact that the MSCI USA Energy Index and the MSCI Europe Energy Index have significantly outperformed their respective broader market benchmarks, year to date through March 11. Investment-grade energy-company bonds, on the other hand, have not benefited as much from this tailwind, as the credit-spread expansion in the exhibit below shows.

While equity and corporate-bond returns of the same issuer have historically been positively correlated over the long term, this relationship may break down over shorter periods.1 One reason for the latest divergence may be the expectation that near-term earnings windfalls may accrue disproportionately to shareholders through dividends and share buybacks.1 Additionally, while both energy-company equities and corporate bonds were positively affected by higher energy prices in the near term, bonds (especially those from European issuers) have been negatively affected by the rising risk of default reflected in the widening credit spreads, due to the ongoing developments of the Russia-Ukraine war.

Energy sector: Equity returns vs. investment-grade credit spreads

Simulated credit-spread performance of U.S. and European energy-sector issuers in the MSCI USD Investment Grade Corporate Bond and the MSCI EUR Investment Grade Corporate Bond Indexes, respectively. Data from Dec. 31, 2021, to March 11, 2022. For market-illustrative purposes during this period only. May not represent long-term index performance.

Subscribe todayto have insights delivered to your inbox.

Research and Insights

Our investing insights explore the topics that matter most, whether on climate and ESG, current market trends or global investing and risk management across asset classes.

1 Ilmanen, Antti. 2003. “Stock-Bond Correlations.” Journal of Fixed Income, 13: 55-66.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.