A smoother ride? Looking at factor-based asset allocation

Blog post

September 3, 2019

- Traditionally, many investors have made strategic asset-allocation decisions with a holdings-based approach.

- Our analysis shows that the holdings-based approach resulted in greater-than-expected fluctuations in risk contributions.

- Further, a factor-based approach that targets a stable risk contribution resulted in less fluctuation in risk contributions and total portfolio risk.

Stable asset-class weights ≠ stable risk contribution

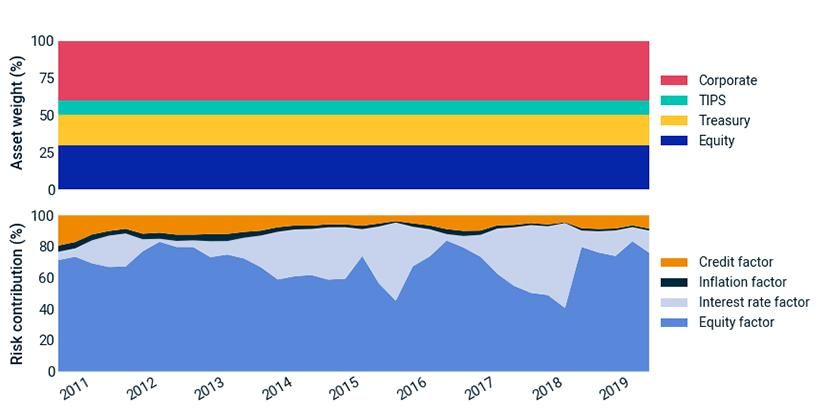

We consider a hypothetical holdings-based allocation with a relatively low weight in equities compared to a 60/40 equity/fixed-income portfolio. Our hypothetical portfolio is designed to resemble the relatively low-equity asset allocation an insurance company might provide. The target weights are shown in the exhibit below.

Target weights of a hypothetical portfolio

Asset class | Target weight |

|---|---|

Asset class Global equity | Target weight 30% |

Asset class U.S. Treasury | Target weight 20% |

Asset class Inflation-linked bonds (TIPS) | Target weight 10% |

Asset class Investment-grade corporate bonds | Target weight 40% |

We rebalance the hypothetical portfolio to the target weights on a quarterly basis, between Q1 2011 and Q1 2019. The exhibit below shows the stable-by-design asset weights (top) and the risk contributions (bottom) of equity, interest-rate, inflation and credit factors.3

Two observations are notable. First, with the equity allocation at just 30%, the risk contribution from equity averaged about 70% throughout the period. Second, the factor risk contributions exhibited significant fluctuations. Most striking, by the beginning of 2018, a bull market pushed the equity risk contribution to a decade-low level of 40%, while the interest-rate factor risk contribution increased; however, rising risk in the aftermath of the February 2018 market sell-off quickly boosted the equity factor risk contribution to nearly 80%.

Steady asset weights, volatile risk levels

Holdings-based allocation

Source: For bond sectors, ICE Data Indices, LLC; used with permission: ICE BofAML US Treasury Index (G0Q0), ICE BofAML US Inflation-Linked Treasury Index (G0QI), ICE BofAML US Corporate Index (C0A0). The equity market is represented by the MSCI ACWI Index. Risk contribution is calculated with the MSCI factor model. Top and bottom panels show the asset allocation and the risk contribution, respectively. The interest-rate factor is mapped to Treasurys, TIPS and corporate credit assets.

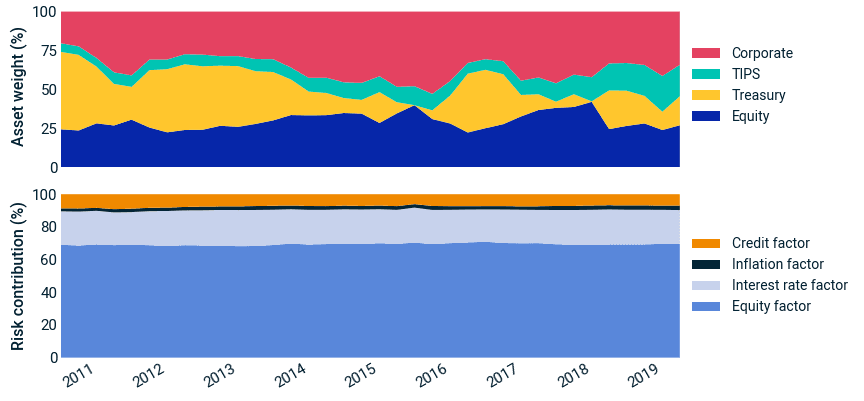

What if, instead of setting asset-class weight targets, we set factor allocation targets, defined as the target risk contribution from each factor? Since factor risk contributions add up to total portfolio risk, this effectively allowed the hypothetical investor in our example to assign a "risk budget" — rather than a "capital budget" — to each factor. Intuitively, if investors expected that factor returns justified the amount of risk each factor contributes to the total portfolio risk, they could have inversely budgeted the risk contributions based on their expected factor returns.4 Assuming relatively stable expected returns, a stable risk-contribution profile may have been desirable.5 The exhibit below illustrates such a dynamic hypothetical portfolio composition (top), where asset-class weights responded to the changing factor regime and achieved a stable risk contribution (bottom).6

Dynamic asset weights, steady risk levels

Factor-based allocation

Source: For bond sectors, ICE Data Indices, LLC; used with permission: ICE BofAML US Treasury Index (G0Q0), ICE BofAML US Inflation-Linked Treasury Index (G0QI), ICE BofAML US Corporate Index (C0A0). The equity market is represented by the MSCI ACWI Index. Risk contribution is calculated with the MSCI factor model. Top and bottom panels show the asset allocation and the risk contribution, respectively. The interest-rate factor is mapped to Treasurys, TIPS and corporate credit assets.

We note that dynamic portfolio composition could result in a significantly higher portfolio turnover rate, which may be mitigated through constraints.

What about total risk and returns?

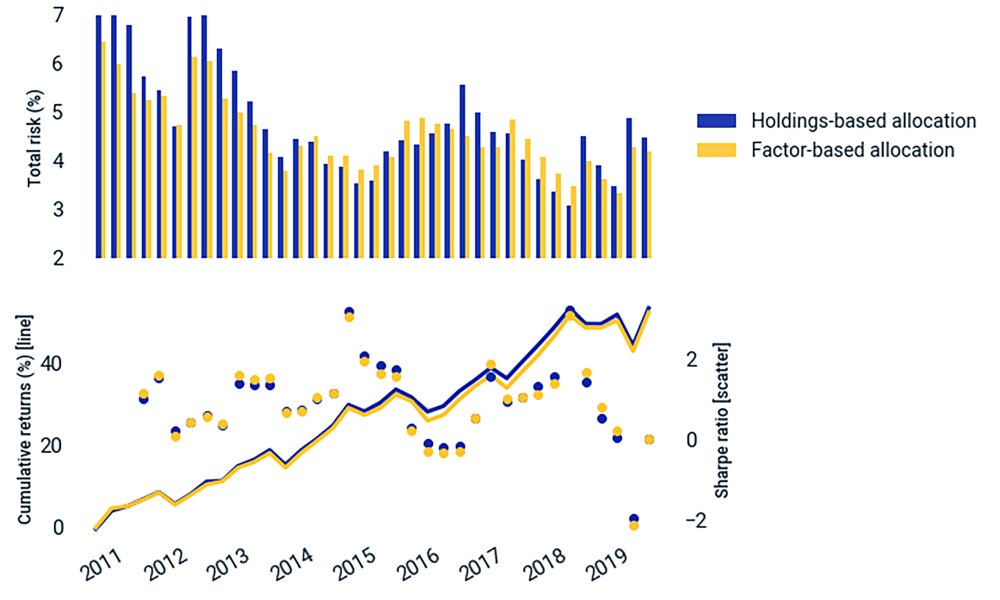

When it comes to risk and returns, the results were mixed. As we might expect, the factor-based allocation had more consistent total risk over the full period. However, as we see in the bottom panel of the exhibit below, which shows the Sharpe ratio (risk-adjusted return) on an annual rolling basis, each portfolio outperformed in different periods. In 2013 and late 2017 the factor-based approach had higher risk-adjusted returns, while in 2015 and 2016 the holdings-based approach outperformed.

Further research can help us gain a more comprehensive understanding of the sources driving these behaviors, but intuitively one can understand when either approach performed better: The holdings-based approach was effectively a buy-losers, sell-winners strategy, which was advantageous when returns exhibited mean reversion — as the equity market did in 2016. The factor-based approach, on the other hand, allocated more weight to an asset when the relevant factor volatility decreased. It outperformed while the low volatility lasted, as happened during late 2017's persistent equity bull market.

Risk-adjusted returns were mixed between the two approaches

Top panel shows the total risk of the two portfolios. The bottom panel shows the cumulative performance of the two portfolios (left axis), both scaled to an ex-ante volatility target of 4.7% at each rebalancing date. By rescaling, we can compare the portfolio performance on a risk-adjusted basis. The bottom panel also presents the Sharpe ratio on an annual rolling basis (scatter plots, right axis).

Our analysis shows that the holdings-based asset-allocation approach used here resulted in greater-than-expected fluctuations in risk contributions. The factor-based approach, on the other hand, targeted a stable risk contribution by design, whereby asset-class weights varied in response to regime changes.

1 For example: Brinson, G.P., Hood, L.R., and Beebower, G.L., 1995. "Determinants of portfolio performance." Financial Analysts Journal 51(1): 133-138.

2 This report contains analysis of historical data, which includes hypothetical, backtested or simulated performance results. There are frequently material differences between backtested or simulated performance results and actual results subsequently achieved by any investment strategy. Past performance — whether actual, backtested or simulated — is no indication or guarantee of future performance. None of the information or analysis herein is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision or asset allocation and should not be relied on as such.

3 We use the MSCI Multi-Asset Class (MAC) Factor Model Tier 1 factors in the analysis. They reflect the high-level drivers of risk and returns across asset classes and markets. Factor risk contribution is defined as: factor exposure × factor risk × factor correlation with the portfolio.

4 Bruder (2012) proved that if an asset allocation is mean-variance optimal, the return contribution of each asset is proportional to its risk contribution. A similar proof can be applied to risk budgeting across factors. Bruder, B. and Roncalli, T. 2012. "Managing risk exposures using the risk budgeting approach." SSRN.

5 A structural shift in the market could change this assumption. Here we present a hypothetical example for illustrative purposes.

6 The target factor allocation was chosen so that the holdings- and factor-based approaches have about the same average risk contribution throughout the analysis period.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.