All FAANGs are Not Created Equal

Blog post

August 3, 2018

FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) make up nearly 40% of the NASDAQ 100 index, and smaller but significant weights in many others. Commonly grouped as tech stocks or growth companies, it seems reasonable to assume they share many similar characteristics. However, when examined through the lens of performance-driving factors, their characteristics are far from homogeneous.

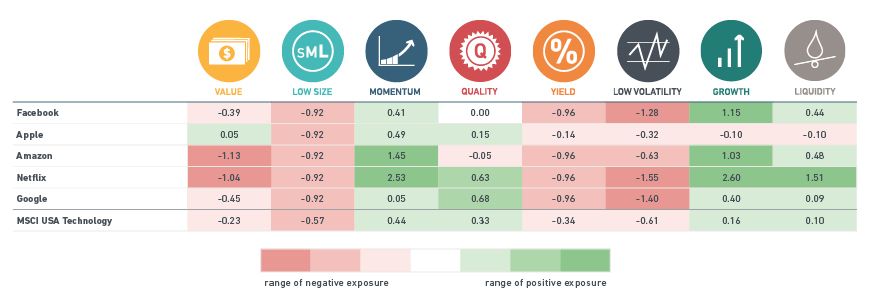

The table below displays the MSCI FaCS characteristics of the FAANG stocks as of July 27, 2018, as well as the exposures of the MSCI USA Technology Index (for reference). FaCS measures the degree to which a company or portfolio tilts, or is "exposed," to factors that have been shown to be important drivers of portfolio risk and return.

FAANG factor tilts relative to the benchmark

Source: MSCI FaCS. The values are provided in units of standardized exposure, or how far away from the benchmark index (MSCI ACWI IMI), which has an exposure of zero, the given stock or portfolio is tilted. Individual company exposures typically vary from -3 to +3, while diversified portfolios are typically in the range of -1 to +1.

Breaking these big tech firms into smaller pieces through factor exposures shows significant variability. For example:

- Quality (a measure of the strength, efficiency and stability of a company's operating performance and use of capital): Exposure ranged from -0.05 for Amazon to 0.68 for Google.

- Momentum (price performance over the last 12 months excluding the most recent month): While all the FAANG stocks showed a positive exposure to momentum, they varied from the very-near neutral 0.05 for Google to +2.53 for Netflix.

- Value (price relative to book value, earnings, cash flow and other measures): Apple was the only FAANG with a positive exposure.

- Growth (historical earnings and revenue growth plus forecast earnings growth): Apple had a slight negative exposure, while Netflix had a very large one.

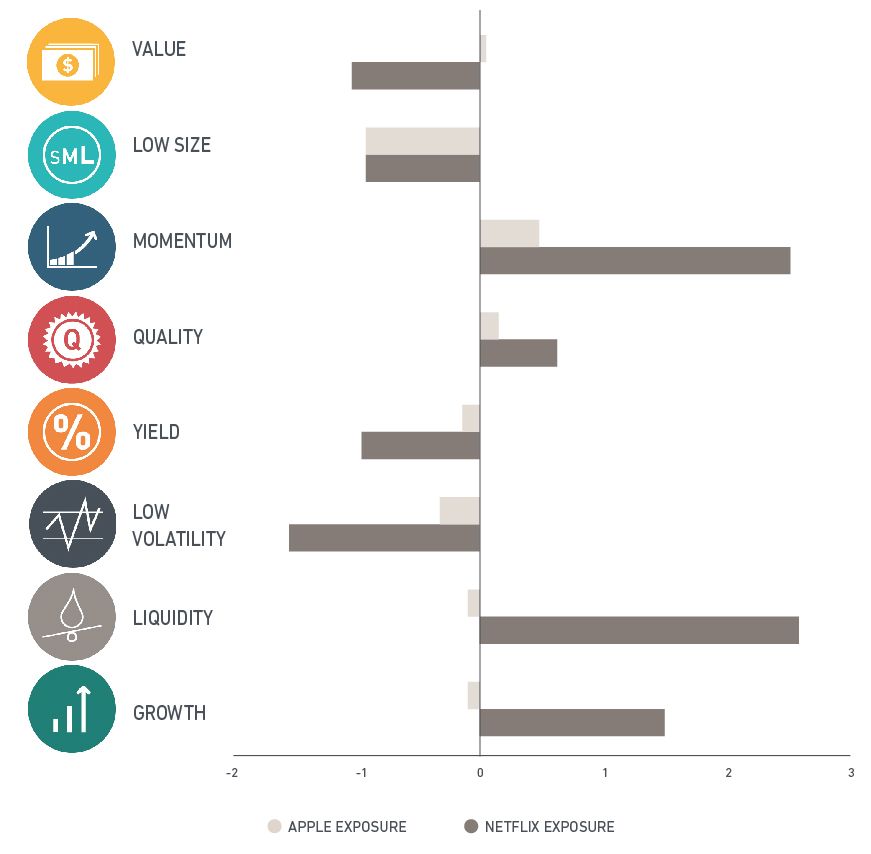

Apple and Netflix FaCS Exposures

Source: MSCI FaCS. The MSCI FaCS size and volatility factors are displayed in the Factor Box as low size and low volatility. Therefore, negative exposure to low size or low volatility means there is a positive exposure to the factors size or volatility. For example, negative exposure to low size represents heightened exposure to larger market capitalization companies.

FACTOR EXPOSURES CHANGE OVER TIME – EVEN FOR INDIVIDUAL STOCKS

Also important to note is that factor exposures have varied not only across seemingly similar stocks, but have also been quite dynamic and changed over time for individual companies. In the exhibit below we take Apple – which saw its stock price rise on strong second-quarter earnings even as other FAANGs, such as Facebook, fell – as an example. Our analysis shows select MSCI FaCS exposures over time, focusing on the quality, momentum, value and growth factor groups for legibility purposes.

Select FaCS Exposures for Apple

As we can see, in the early 2000s, as Apple sought to redefine itself, it had negative exposures to all four factor groups at times. It was relatively expensive, had relatively low earnings and revenue growth and relatively weak and inefficient operating performance. After the success of their new products in the mid-2000s, almost everything surged – growth, profitability, stock price and valuation ratios. In the last few years, growth has slowed, valuations have come down significantly, operating performance has strengthened and they have been more conservative in use of capital.

Breaking the FAANGs into bite-sized pieces revealed the importance of analyzing securities and portfolios beyond questions of sector or value versus growth. These unique factor fingerprints offered improved understanding of critical drivers of portfolio risk and return.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.