Alternative Views of Equity-Market Liquidity During COVID-19

Blog post

August 26, 2020

- Liquidity measures based on overall traded volume reflect overall liquidity but may not fully capture all the trading dynamics that influence rebalancing decisions.

- Alternative measures like the Amihud illiquidity ratio, bid-ask spread and transaction costs may provide a more comprehensive view of market liquidity.

- These complementary measures indicated that the markets were under liquidity stress during the onset and recovery from the COVID-19 crisis, although liquidity improved more recently.

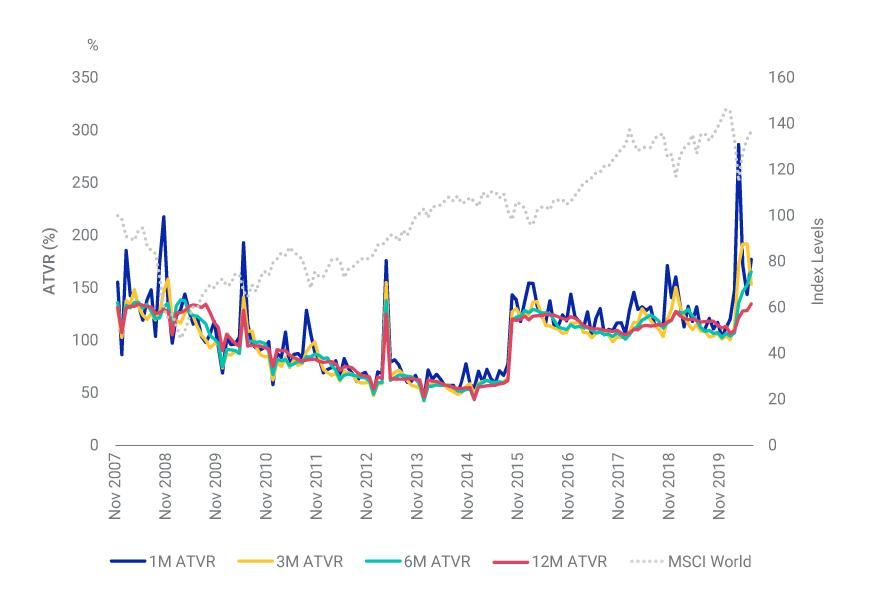

Measures of Relative Traded Value May Not Always Be Adequate

The annual traded-value ratio (ATVR) used in the MSCI Equity Index methodologies1 reflects average traded value relative to the free-float-adjusted market capitalization of a security over a specific period. Its approach seeks to account for the varying size of securities and mitigate the impact of extreme daily trading volumes. ATVR also can be aggregated at the index level as a proxy for overall market liquidity.

In a normal market environment, this measure has been a good proxy for liquidity. During periods of heightened market volatility, however, trading volumes may increase while the cost of trading also increases (as reflected by the alternative measures shown later). We saw this phenomenon, which shows some of the limitations of ATVR, during the recent market stress related to the coronavirus crisis.

ATVR Spiked During the Market Correction at the Onset of COVID-19

Focus on the Evolution of Equity-Market Liquidity

To observe the historical liquidity trend in isolation, we assumed both a constant portfolio and constant level of trading. For the portfolio, we create a global equity universe based on the MSCI World Index that we call "World Common Securities."2 For the level of trading, we use a constant proportion (number of shares traded divided by the overall number of free-float shares) for each security over the entire study period from November 2007 to July 2020. This constant proportion depends on assumptions of the overall trade value for the common securities within the MSCI World Index — USD 100 million, USD 500 million and USD 1 billion3 as of July 31, 2020. This is then scaled historically for each analysis date by the security's returns. For all scenarios, we assume trading is completed in a single day.

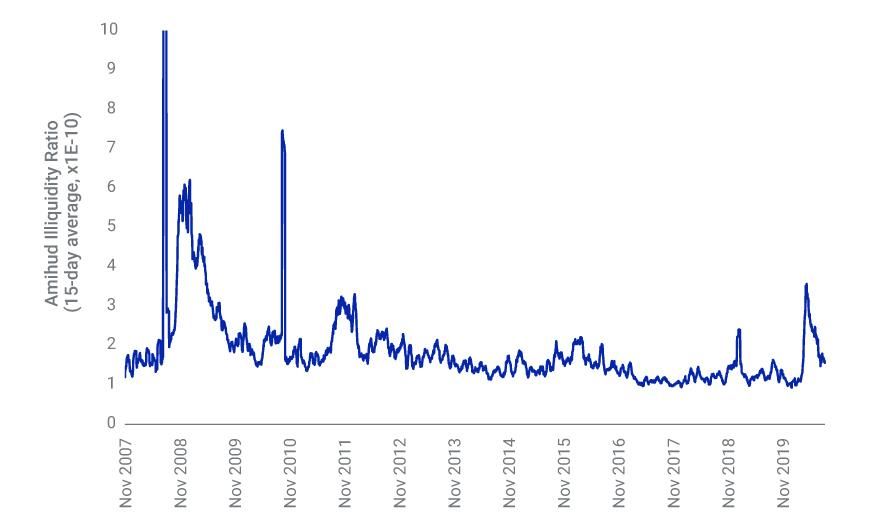

Market-Impact Costs as Measured by Amihud Illiquidity Ratio

To begin our exploration into alternative liquidity measures, we evaluate the market-impact costs of our hypothetical World Common Securities portfolio using an observable market measure, the Amihud illiquidity ratio. This measure reflects how sensitive prices were to trading volumes and therefore the extent to which a market was moved by trading activity.4 This can be aggregated for our portfolio using each security's Amihud illiquidity ratio and free float-adjusted market capitalization weight.

As seen in the exhibit below, the Amihud illiquidity ratio spiked during the market correction in March (indicating less liquidity), but it was lower than some of the peaks during the 2008 global financial crisis (GFC). And it's been coming down steadily since the spike, indicating greater liquidity.

Amihud Illiquidity Ratio Spiked in March, but Stayed Below Level During GFC

Data from November 2007 through July 2020.

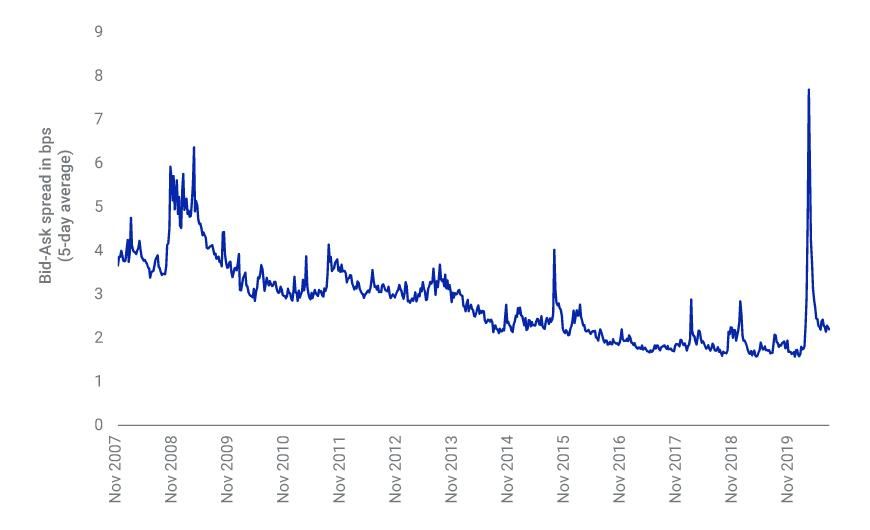

Transaction Costs as Measured by Bid-Ask Spread

Next, we estimate transaction costs for our hypothetical World Common Securities portfolio. The first method is to aggregate another market observable measure, each security's bid-ask spread where the spread is calculated using a five-day time-weighted average of market prices. The bid-ask spread has historically widened during periods of market volatility, increasing the cost of executing trades.

Indeed, during the recent market correction in March, the bid-ask spread increased to levels higher than those during the GFC (and at a faster pace), as shown in the exhibit below. We can also see, however, that the spread reduced considerably in April and in subsequent periods, again at a faster pace than during the GFC.

Bid-ask Spreads in March Soared Higher and Faster than During the GFC but Declined Rapidly

Source: Virtu, MSCI

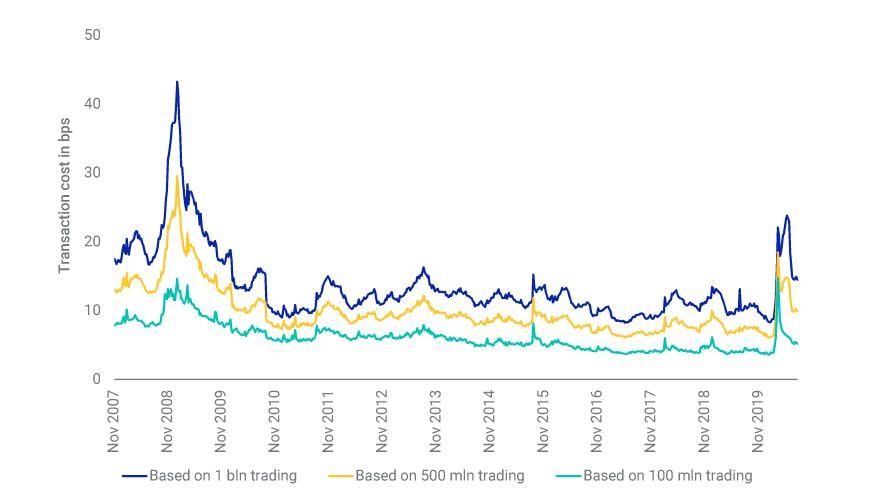

Transaction Costs as Measured by Bid-Ask Spread Plus Model-Driven Market-Impact Cost

Bid-ask spread has been useful at lower levels of assets under management (AUM). To cover a broader spectrum of AUM, however, we complement the bid-ask measure with the market-impact cost from the MSCI's RiskMetrics® LiquidityMetrics model.5 Doing so can help directly quantify the liquidity impact, but the effectiveness of calculating transaction costs depends on the model used to estimate the market impact cost as well as the assumed size of the trade.

Transaction costs calculated using this method surged recently, although they were still lower than the levels seen during the GFC. Unlike the market-observable liquidity measures (Amihud illiquidity ratio and bid-ask spreads), transaction costs continued to rise even after the equity market rebounded, though they have eased since the beginning of June. A contributing factor may be that the liquidity model measures historical volatility based on the past 60 days; this rise in market-impact costs reflected the low-volatility days being replaced by days with more volatile returns as the markets rebounded.

Transaction Costs Surged in Spring, but Have Declined Since Early June

Source: Virtu, MSCI

Summing It Up

There are multiple liquidity measures that institutional investors can use to assess overall liquidity and gain insights into the practical impact of liquidity on rebalancing costs. Some of these measures are market-observable (ATVR, the Amihud illiquidity ratio and bid-ask spread), while others (transaction costs) may benefit from an analytical model, which can provide cost estimates across different AUM levels.

Despite higher overall trading activity as reflected by ATVRs this year, the complementary measures indicated that liquidity worsened during the recent market correction, but the market rebound since April 2020 helped alleviate the liquidity stress. On a relative basis, the global equity market's liquidity seemed greater than that exhibited during the GFC.

While none of these measures tells the whole story, together they can provide a more comprehensive view of liquidity.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Details on ATVR computation can be found in the MSCI Global Investable Market Indexes Methodology. In 2015, MSCI started using consolidated volumes for calculating relative traded volumes for securities in the U.S. and Canada.2Liquidity characteristics may sometimes get distorted due to a few securities that may get added to or dropped from the MSCI World Index, so we consider only the securities that were part of the index for the entire study period. This approach produces a universe of 874 securities, comprising 73.5% of the index weight as of July 31, 2020.3USD 1 billion of trade value, for example, reflects a 2% two-way turnover for a USD 50 billion hypothetical portfolio of World Common Securities.4Amihud, Y. 2002. "Illiquidity and Stock returns: Cross-section and Time-series Effects." .5Transaction cost is measured as half of the bid-ask spread plus the market-impact cost. For the market-impact cost, LiquidityMetrics uses the Virtu ACE model, based on the implementation-shortfall approach introduced by Andre Perold in 1988, which is defined as the appropriately signed difference between the average execution price and prevailing price at the start of the order execution.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.