Aramco IPO shows importance of timely index inclusion

Blog post

February 4, 2020

- Country indexes offer investors a mechanism to create strategies that allow them to tailor their emerging-market (EM) allocations on a country-by-country basis.

- However, there could be gaps between a country's equity index exposure and the underlying drivers of its economy.

- Such gaps could be even more important for large companies, as with the recent example of Saudi Aramco's inclusion in the MSCI Global Investable Market Indexes (GIMI).

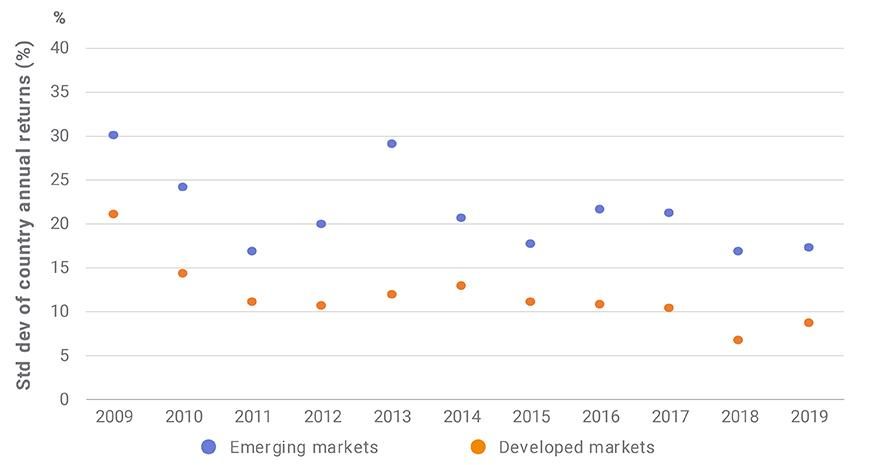

EM countries were less correlated and more diverse than those in developed markets

Investors can take multiple approaches for their EM portfolio allocations depending on their conviction and investment philosophy. We have previously highlighted why an investor with strong convictions might use active managers or funds that aim to replicate single-country indexes to build tailored EM exposure. Here, we build on that discussion.

We looked at average pairwise correlation among EM countries, and found it was consistently and significantly lower than that of developed-market (DM) countries, which indicates individual EM markets were less likely to rise or fall together. Additionally, examining dispersion of returns highlighted higher divergence between EM countries compared to DM. Higher dispersion in returns may provide opportunity for investors to take an active view in their country allocations.

Pairwise correlation and dispersion of country returns, EM vs. DM

Three-year rolling country correlations in emerging and developed markets

Cross-sectional dispersion of annual country returns within emerging and developed markets

Timely updates of the investment opportunity set

New, smaller securities may be included as part of regular index reviews, as it is important to group index turnover at designated times, and usually such smaller securities have, individually, had a correspondingly smaller impact on index composition. On the contrary, large IPOs can significantly change the opportunity set and therefore might be included in equity indexes outside the scheduled index review cycles. (MSCI GIMI works to maintain relevant index composition in this way.)1

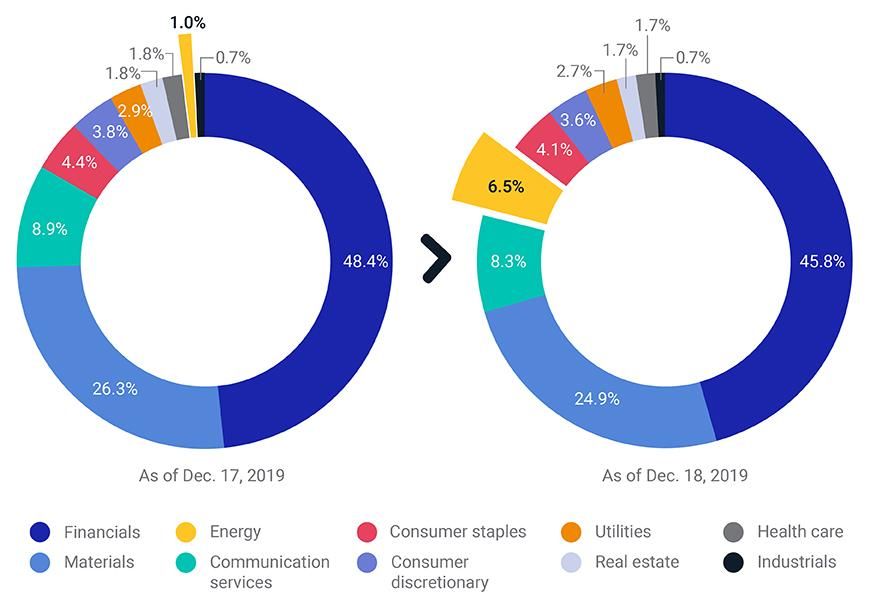

For example, Saudi Aramco had a full-company market capitalization of USD 1,877 billion as of the close of business on Dec. 11, 2019, its first trading day. This made it the largest company globally, more than 1.5 times the size of Apple Inc., the second largest company. Aramco had a low free float of 0.5% — but, helped by its high total market capitalization, it was added to MSCI GIMI on Dec. 18, 2019. On that date, the company accounted for only 0.02% of the MSCI ACWI Index and 0.16% of the MSCI Emerging Markets Index, but contributed 6.37% to the MSCI Saudi Arabia Index.2 As such, it stands as an example of how timely index inclusion of newly eligible large companies could be very important for investors focusing on a specific country.

Better reflection of the underlying economy

This inclusion of Aramco also had a significant impact on the sector composition of the MSCI Saudi Arabia Indexes. As shown in the exhibit below, the energy sector previously had very low representation in the MSCI Saudi Arabia IMI, comprising less than 1% of the index. Again, even with Aramco's low free float, the weight of the energy sector rose to 6.5% after inclusion, bringing closer alignment between the country's economy and the publicly listed investment universe.

Aramco's inclusion increased the energy sector's weight in the MSCI Saudi Arabia IMI

Sector weights in the MSCI Saudi Arabia IMI before and after Saudi Aramco's inclusion.

Additionally, index methodology changes may be considered if substantial portions of the investable opportunity set are missing from country indexes due to market evolution or other developments. One such development is that, over time, a substantial number of companies, especially in EM, chose to list their stocks in countries different from their domicile. Excluding such companies from their domiciled country indexes eventually resulted in a notable gap in coverage. To work to bridge that gap in the MSCI GIMI, for example, Chinese companies such as Alibaba and Baidu Inc. (both listed in the U.S.) were included in MSCI China Indexes and other regional indexes (of which China is a part) to reflect the information technology sector's significant contributions to China's economy.

Mind the gap

While a timely inclusion of large companies and those listed outside their home countries can help align the publicly listed investment universe with a country's economy, gaps could remain. As stated above, the inclusion of Saudi Aramco raised the energy sector's index weighting to 6.5%, but the extraction of crude oil and natural gas contributed to approximately 40% of Saudi Arabia's GDP in 2017, as per Saudi Arabia's General Authority for Statistics. In due course, such a gap may be bridged with an increase in free float, an easing of investment restrictions or greater liquidity. Each of these remedies lies outside the control of index providers and investors but, when paired with a focus toward timely inclusion, could help in bridging the gap.

The author thanks Pavlo Taranenko and Jean-Maurice Ladure for their contributions to this research.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1For a company to be considered a large IPO, it should clear the minimum thresholds specified in the MSCI Global Investable Market Indexes Methodology.2MSCI provided inclusion details for Saudi Aramco in MSCI GIMI in a Dec. 11, 2019, announcement.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.