Are Emissions Rising or Falling in Equity Indexes?

- As carbon reporting becomes more widespread, investors will increasingly need a better understanding of why carbon emissions are changing in portfolios and indexes.

- We analyzed recent changes in Scope 1 and 2 emission intensity of companies and were faced with a puzzle: Index-level intensity increased recently, even though emissions of individual index constituents generally fell.

- Index-level emission-intensity change was driven by the growing weight of the three most emission-intensive sectors and decreasing weight of some low-intensity sectors.

Rising emission intensities without a rise in emissions

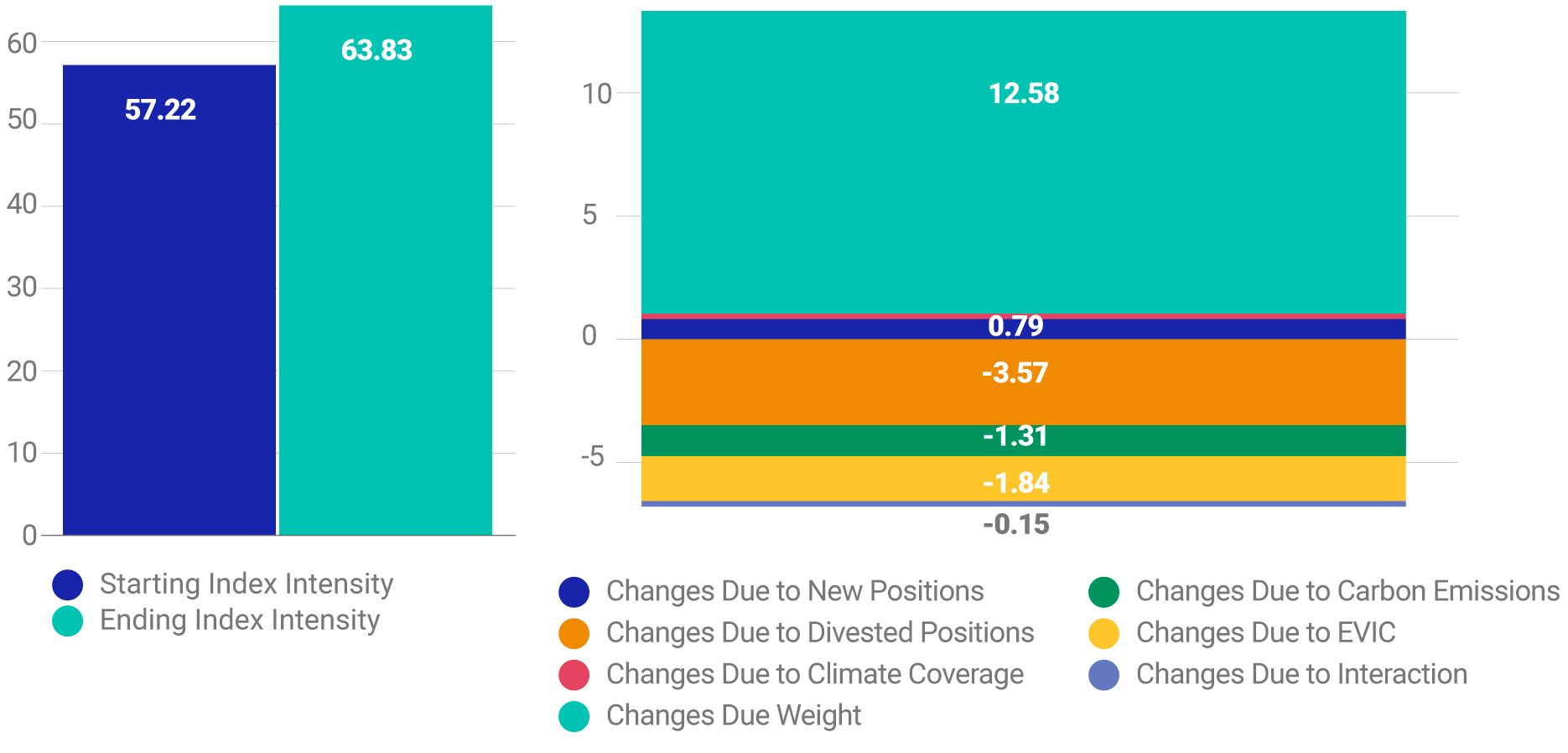

Average emission intensity3 increased by more than 10% between Nov. 30, 2021, and April 29, 2022, for the MSCI ACWI Investable Market Index (IMI), as the exhibit below shows.4 This increase reversed a trend, as the MSCI ACWI IMI's intensity had been falling by roughly 10% annually since 2015.5 One might wonder if this means that the index constituents' total emissions increased in recent months. After aggregating Scope 1 and 2 emissions, however, we see no evidence of an overall increase. Since carbon-intensity reporting is becoming more widespread, investors will likely confront similar "puzzles" in their portfolios more often in the years ahead. The attribution methodology presented in this blog post may provide more clarity on such occasions.

Absolute emissions measures the release of harmful greenhouse gases into the atmosphere, which affects the remaining global carbon budget. In contrast, portfolio-level emission intensity is monitored because it is a measure of carbon efficiency and can also be viewed as an indicator of financial-market risk, including the risk that more stringent climate policy could potentially affect valuations.

EVIC-based emission intensity rose in recent months

Evolution of Scope 1 and 2 intensities and Scope 3 intensities (emissions over enterprise value including cash, or EVIC) of the MSCI ACWI Investable Market Index, from May 29, 2020, to April 29, 2022. EVIC-based intensity is recommended by the Partnership for Carbon Accounting Financials.

Attributing the changes in emission intensities

We used MSCI Climate Lab Enterprise to attribute the past five months' increase in the MSCI ACWI IMI's Scope 1 and 2 carbon intensity to various drivers. We looked at the effect of the change in one variable, while assuming the other variables remained constant. As shown in the exhibit below, the intensity change of +6.6 tons of CO2 equivalent/USD 1 million of EVIC was primarily driven by changes in market-value weights of the index (12.58 tons/USD 1 million EVIC), while the contribution from absolute emissions was slightly negative (-1.31 tons/USD 1 million EVIC) during this period.6 It is worth noting that the divested-positions bucket had some offsetting effect (-3.57 tons), which was driven by the removal of all Russian securities from the index by MSCI after client consultations in response to Russia's invasion of Ukraine.

Decomposition of change in index emissions intensity by source

Attribution of the intensity change of Scope 1 and 2 emissions (in tons of CO2 equivalent/USD 1 million of EVIC) of the MSCI ACWI IMI, between Nov. 30, 2021, and April 29, 2022.

To further understand how the different sectors of the index contributed to this change, we use a Brinson attribution.7 The intensity change was mostly driven by a sector-allocation effect: The weight of the energy, materials and utilities sectors, which are the three most emission-intensive sectors, increased. This gain was modestly offset by a negative-selection effect, as the energy and utilities sectors in the index got somewhat cleaner.8

Brinson attribution of the five-month change in emission intensity

Brinson attribution of the intensity change for Scope 1 and 2 emissions of the MSCI ACWI IMI, between Nov. 30, 2021, and April 29, 2022.

Looking more closely at the sector effects, we see below how changes in index composition impacted index intensities. In the equity market, the relative underperformance of the information-technology, consumer-discretionary and communication sectors pushed down their weights in the index over our period of analysis. These sectors all have relatively low emission intensities, so their lower index weights contributed to a rise in the index-level carbon intensity. In addition, the increased weights in energy, utilities and materials — combined with their high emission intensities — also contributed to the rise in index-level carbon intensity.

How did sectors contribute to intensity change?

The left-hand chart shows the change in sector weights of the ACWI IMI, from Nov. 30, 2021, to April 29, 2022. The right-hand chart shows the Scope 1 and 2 emission intensity of the index on Nov. 30, 2021, and the red line shows the average portfolio intensity.

Solving the puzzle

Investors monitoring the average emission intensities of their portfolios and indexes might want to keep in mind that they are not solely dependent on the emissions of the constituents. Changes in portfolio and index composition and changing sectoral weights pushed up average emission intensities and masked position-level declines in absolute emissions, over the period of study.

The authors thank Jason Mirsky for his contribution to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Frankel, Ken, Shakdwipee, Manish, and Nishikawa, Laura. 2015. “Carbon Footprinting 101: A Practical Guide to Understanding and Applying Carbon Metrics.” MSCI Research Insight.2Scope 1 represents direct emissions, Scope 2 emissions are from electricity consumption and Scope 3 emissions are from the value chain. “Carbon Emissions Estimation, Methodology and Definitions.” MSCI Research Insight, June 2021.3Weighted average carbon intensity here is defined as equity-market-cap-weighted average of constituents’ Scope 1 and 2 emissions over enterprise value including cash, or EVIC.4Although this blog post focuses on the MSCI ACWI IMI, emission intensities also increased markedly during this time frame for MSCI Europe IMI, MSCI World IMI and MSCI USA IMI.5Average Scope 1 and 2 emission intensity of the MSCI ACWI IMI roughly halved to 77 tons/USD 1 million of EVIC between January 2015 and January 2020.6The decline in contributions from absolute emissions was partly driven by the incorporation of more 2020 emission data in the calculation. Companies’ emissions data is reported infrequently — usually annually. EVIC data is typically updated once in a fiscal year and constituent market weights daily. As of November 2021, 53% of index constituents had emissions data from 2019, while 47% had data from 2020. By the end of April 2022, 94% of constituents had emission data from 2020 and 2% from 2021. Of those constituents with 2020 emission data, 54% showed a decline in emissions7Brinson attribution was originally developed for performance attribution and is based on active weights. In the form we used, we attributed the intensity change of the index as of April 29, 2022, compared to the index as of Nov. 30, 2021, to allocation, selection and interaction categories of drivers. For a particular sector, for example, a positive allocation effect means an increase in emission intensity over the period could be attributed to allocating more weight to that sector, compared to the earlier version of the index.8This effect was partly driven by the exclusion of Russian securities.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.