Are rates and equities losing their balance?

Blog post

September 16, 2019

- Asset allocators are focused on the risk that a secular shift in the relationship between interest rates and equity could undermine the safety of balanced portfolios, especially risk-parity strategies.

- A new macroeconomic model derives this relationship from the behavior of growth and inflation and enables us to project this changing relationship into future scenarios.

- These projections suggest that conditions are still far from a flip in the rates-equity correlation, which stays positive for the next decade in more than three-quarters of model scenarios.

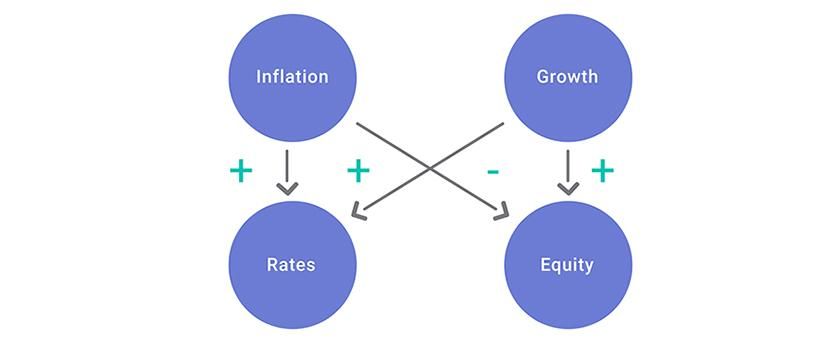

Markets are driven asymmetrically by macroeconomic factors

Our new model explains the behavior of interest rates and equity in terms of underlying macroeconomic factors. In this simplified view, shocks to inflation and growth have opposite effects on rates and equity; the rates-equity correlation is derived from the relative magnitude of the different causes.

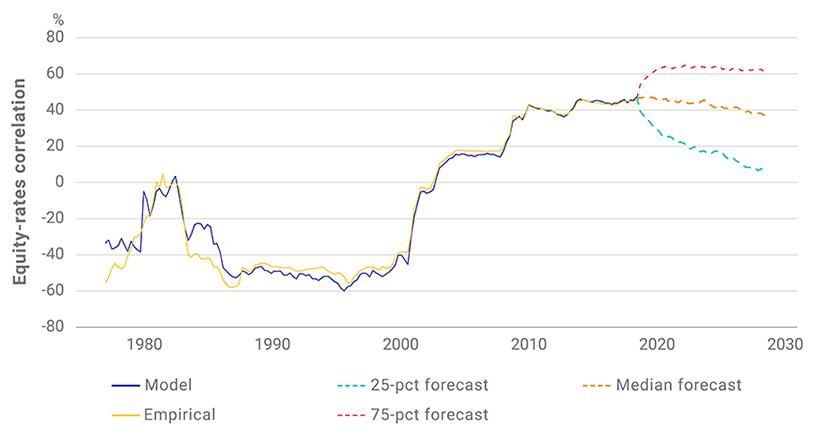

The exhibit below shows the evolution of the rates-equity correlation over the past 40 years, along with the macroeconomic model's implied correlations, which have closely matched the empirical values. In this view, growth has been the primary driver of both equity and rates in the era of strong central-bank policy and moderate inflation, while higher inflation uncertainty was responsible for the negative rates-equity correlation in previous eras. What is the risk of returning to a similar environment?

Projecting the macro view to future scenarios

The realized and projected correlations between the MSCI USA Index and 10-year U.S. Treasury rates. Source: MSCI, Federal Reserve Bank of St. Louis FRED.

The model implies a threshold for the rates-equity correlation to fall to zero: It would require a doubling in inflation uncertainty; returning to historical negative correlations would require even higher levels of inflation risk. Looking forward, projections of macroeconomic scenarios over the next decade tend to show a moderate decline in the rates-equity correlation, but more than three-quarters of the projected scenarios retain a positive correlation for the full decade ahead.

Given its central role in asset allocation, the recent focus on the rates-equity correlation is well justified. A new macro view lets us deconstruct this important relationship, understand the underlying economics driving it, and project its evolution into macro scenarios.

Our analysis suggests there is some likelihood of a weakening relationship between rates and equity, but a return to the correlations of the last century would likely also require a return to the weak central-bank policy and high inflation of those times.

The author thanks Andrea Amato, Andrew DeMond, Milan Horvath and Chenlu Zhou for their collaboration on this research.

1 Our model relates rates and equity to macroeconomic factors, including growth and inflation expectations, and it models the dynamics and interactions of these factors over different horizons. In addition to factors for realized growth and inflation, the model has factors reflecting changing forward-looking expectations. Sensitivities to macro shocks change very slowly over time, while stochastic, time-dependent shock volatilities result in time-dependent correlations among market variables. The most important driver of changes in the rates-equity correlation is the volatility of inflation expectations, which is channeled into rates via policy, and into equity via both discounting and growth expectations.

Further Reading

Subscribe todayto have insights delivered to your inbox.

2 Bond prices rise as bond yields fall, so the bond-equity correlation is opposite to the rates-equity correlation.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.