Are Russian Stocks Worthless?

- International investors in Russian securities have faced significant restrictions in managing and valuing their positions since the beginning of the Russia-Ukraine war, making the market an unviable investment option for many.

- Certain types of Russian securities, such as credit-default swaps (CDS), may be more accessible to foreign investors than cash bonds and equities.

- Under certain assumptions, it's possible to infer a theoretical equity price based on CDS prices that may suggest that Russian stocks are essentially worthless.

Bridge between equity and credit markets

If a firm's equity price goes to zero, it will choose to default on its debt. This idea can be formalized by considering equity as a call option on a firm's value (equity plus debt).1 In this framework, a company's default risk is driven by the firm's value relative to its level of debt. Models based on this concept have been commonly used to compute default probabilities from equity prices, but they can also be used to infer equity prices from default probabilities — which we do in this blog post.

We find that trading in Russian corporate CDS has surged since the Russia-Ukraine war began. Increased trading activity may indicate that the CDS market contains information not present in the equity market. Thus, our research incorporates the CDS market's implied default probabilities to model Russian equity prices.

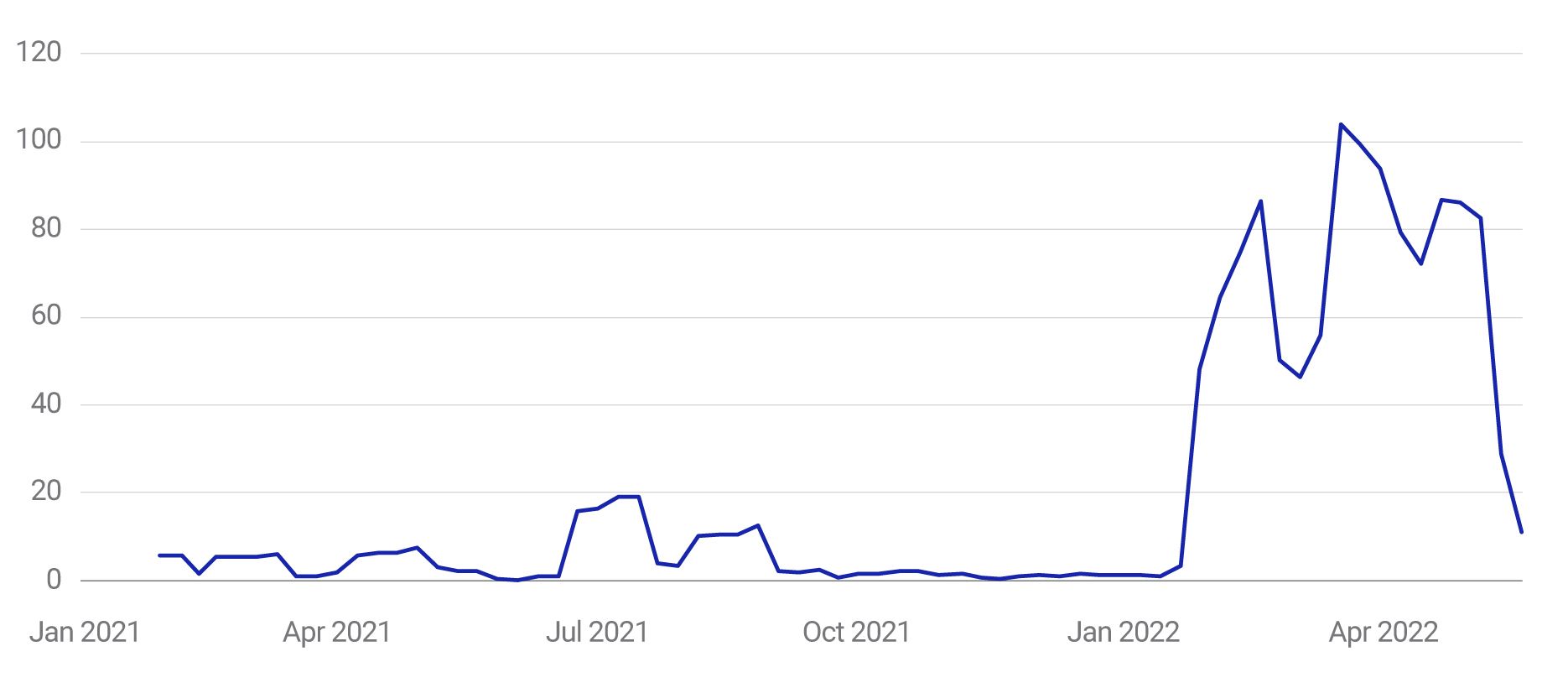

The rapid change in trading of Russian corporate CDS

Monthly average (in USD millions) for Gazprom USD-denominated credit-default swaps. Source: S&P Global Market Intelligence

What the CDS market suggests about Russian equities

While Russian equity prices, as reported by the Moscow Exchange, declined around 40% since the invasion, the prices consistent with the CDS market were essentially zero (as shown in the exhibit below). A basic explanation for the disconnect is that investors trading on one market are not trading on the other. Most foreigners are unable to trade Russian stocks, and CDS are only accessible to institutional investors.

Divergence of Russian stocks and CDS prices

Sample includes the four-largest Russian stocks with CDS quotes: PJSC Gazprom, PJSC Rosneft Oil Company, PJSC Sberbank and The PJSC Lukoil Oil Company.

It's worth noting that the model's results may be a result of the CDS market experiencing its own distortions due to the Russia-Ukraine war. If a default triggers a CDS payout, the underlying bonds would have to be auctioned. Difficulty in transferring these bonds due to sanctions or other market frictions may inflate the premium required for default protection and hence the CDS implied default probability. Furthermore, impediments in making bond payments due to sanctions could trigger a technical default, where the firm is not actually bankrupt but is unable to pay coupons or principal for other reasons.

Trying to bring a distorted market into focus

In a tightly-restricted market such as Russia, every part of the market has experienced some degree of distortion. However, the disconnect between equity and CDS markets is striking and may reflect divergent valuations due to multiple factors. Russian companies may continue to operate, generate revenue and pay dividends, which means they may have value to the small fraction of investors who can invest in them. In contrast, Russian stocks appear to be worthless from the perspective of CDS investors. This lack of value may be emblematic of a combination of technical-default fear, failure of the CDS auction mechanism, restrictions on trading CDS linked to the securities of sanctioned companies, and a lower perceived value of Russian equity for CDS investors. Greater price consistency is possible if Russian markets and the economy reopen and reintegrate, and the extensive international sanctions are lifted. In the meantime, a deeper picture of what is driving prices in equities may be uncovered by searching beyond a single asset class.

The authors would like to thank László Arany for his contribution to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Merton, Robert C. 1974. “On the Pricing of Corporate Debt: The Risk Structure of Interest Rates.” , 29:449-470.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.