Backtesting Expected Shortfall

Blog post

March 17, 2015

When RiskMetrics, now a part of MSCI, announced Value-at-Risk (VaR) as its stated measure of risk in 1996, it initiated an industry standard for institutional risk management that was quickly adopted by the Basel Committee on Banking Supervision for its internal capital adequacy models.

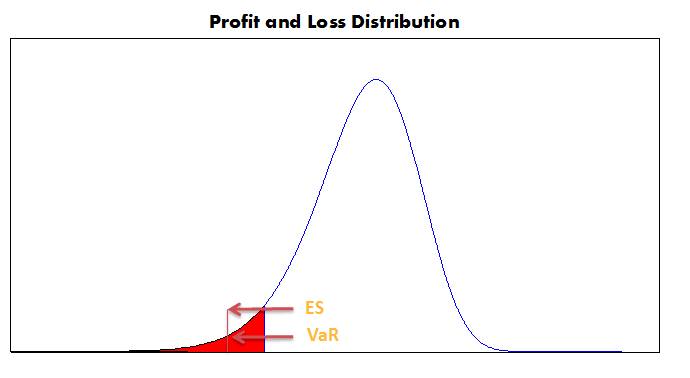

By 1998, however, academic researchers began to critique VaR as a risk measure with structural drawbacks, saying it should be replaced by a "coherent" risk measure. In 2001, an alternative was proposed: Expected Shortfall (ES), which is more sensitive to the shape of the loss distribution in the tail, as can be seen in the exhibit below. Practitioners worldwide adopted ES in parallel with VaR, citing how ES could detect tail risk and offered better mathematical properties for portfolio risk aggregation.

Expected Shortfall Shows Greater Sensitivity to Downside Risks than VaR

For the next 15 years, academic debates over VaR versus ES often reached impassioned levels.

During this time, VaR was the measure required by regulators. However, in May 2012, the Basel Committee proposed an overhaul and rationalization of its capital adequacy rules, after finding discrepancies in the ways banks measured losses in a period of significant financial stress. Part of the Basel proposal was to change the measurement from VaR to ES, which regulators believed would better capture the extreme losses that can occur during times of systemic turmoil.

At the same time, however, some critics said that Expected Shortfall did not possess a mathematical property called elicitability, which caused some to believe that the measure could not be backtested like VaR. Our research shows otherwise, opening the door to a transition to ES from VaR..

We introduced three model-independent, nonparametric backtest methodologies that proved more powerful than the standard Basel VaR test in our research. Our three ES backtests generally required the storage of more information, but we found no conceptual limitations or computational difficulties. In fact, one of the proposed backtests did not require any additional storage of data from a normal VaR backtest.

Read the paper, "Backtesting Expected Shortfall."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.