Beware high dividend yield traps

Blog post

October 25, 2019

- With interest rates and bond yields at near-term historical lows, some investors may seek yield through high dividend-paying equities.

- A simple selection strategy based on trailing yields could have exposed investors to "yield traps" that resulted in below-expectation delivered yield, especially in volatile market conditions.

- A dividend strategy that filtered stocks based on additional aspects such as dividend sustainability and persistence, technicals and quality safeguarded investors against yield traps while maintaining high yield levels.

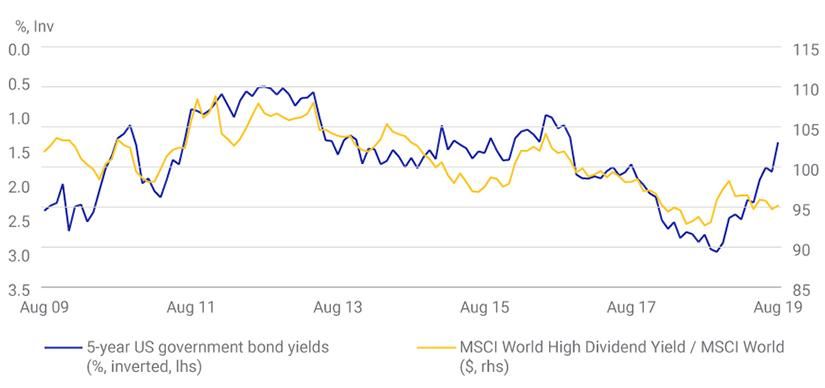

Worldwide high dividend yields outperformed when medium term U.S. bond yields declined

However, an overly simplistic approach of selecting securities based only on high trailing dividend yield could have exposed investors to potential "yield traps." That is, companies with high trailing dividend yields were not always able to deliver on the expected yield in the following period, especially during periods of heightened market volatility.

In periods of general economic distress, the share prices of companies might correct significantly in a short time frame. In such a situation, the trailing yields could artificially spike only to be abruptly reduced upon the occurrence of reduced or discontinued dividends. This precise scenario played out during the GFC as some banks cut or stopped paying dividends for balance sheet and regulatory capital reasons. In fact, many of the initially highest trailing yield stocks in the banking sector stopped paying dividends for a significant time period during and after the GFC.

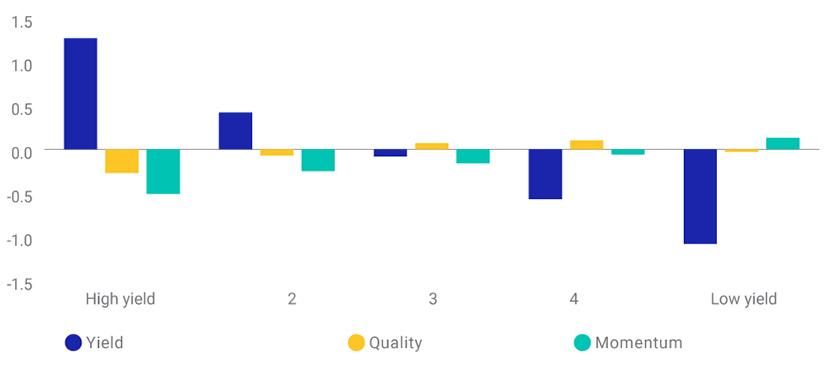

Top quintile yield did not equal top quality

A recent simple yield analysis of MSCI World Index constituents shows that top-quintile yield companies had lower quality characteristics, based on data from June 2019 (see exhibit below). Interestingly, the top quintile also had a negative exposure to active momentum. As both quality and momentum have been academically recognized as risk premia factors (Gupta et al., 2015),1 Lim et al., 2015),2 this analysis indicates that a simple screen based on high yield faced headwinds.

Companies with high dividend yield had low exposure to quality and momentum

Can you screen for yield traps?

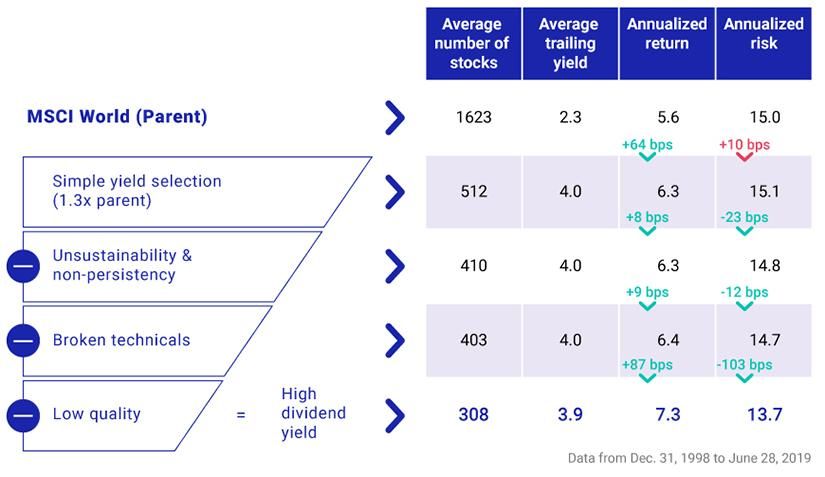

Screening for potential yield traps may be accomplished by filtering out companies with unsustainable or non-persistent dividend payouts, broken technicals and low quality. To assess the incremental added value of four potential screens, we generated different simulations over the past 20 years using the MSCI World Index as the parent index, each one incrementally building on the one before (see exhibit below). The four screens were:

1) Simple yield selection. We included only securities that offered a higher than average dividend yield (at least 30% higher for the new constituents) relative to the parent index.

Using this screen, our universe declined to slightly less than a third of the initial 1,600 stocks, while the dividend yield rose from 2.3% to 4%. This approach returned an extra 64 basis points (bps) per year versus the MSCI World Index during our study period, corroborating the presence of a yield premia. However, it was marginally riskier with a volatility of 15.1%.

2) Unsustainable and non-persistent payouts. We excluded securities with extremely high payout ratios or negative earnings (unsustainable payouts), and firms with volatile payout policies (non-persistent dividend record).

On average, this screen excluded another 100 stocks and left the yield unchanged, but it added another 8 bps of outperformance and reduced risk compared to the index with only the first screen during the past 20 years.

3) Broken technicals. Within the universe of securities with negative one-year price return, we excluded the bottom 5% of securities by price momentum.

Although this screen excluded only seven stocks on average, it was enough to reduce the negative momentum exposure to almost neutral and it further enhanced the risk/return trade-off compared to the index with the first two screens (+9 bps per year of return and -12 bps per year of risk) during our study period.

4) Low quality. We excluded securities with weak fundamentals, such as negative quality Z-scores based on a composite of return on equity, earnings variability and debt to equity.

This screen excluded another 100 stocks on average. The yield remained almost unchanged at 3.9%, but the risk/return trade-off improved vastly and pushed quality exposure into positive territory. The return of the final simulation, combining the four screens ("high dividend yield approach" hereafter) increased to 7.3% per year from 5.6% for the MSCI World Index (parent index) while volatility dropped from 15.0% to 13.7%.

Impact of yield traps screening

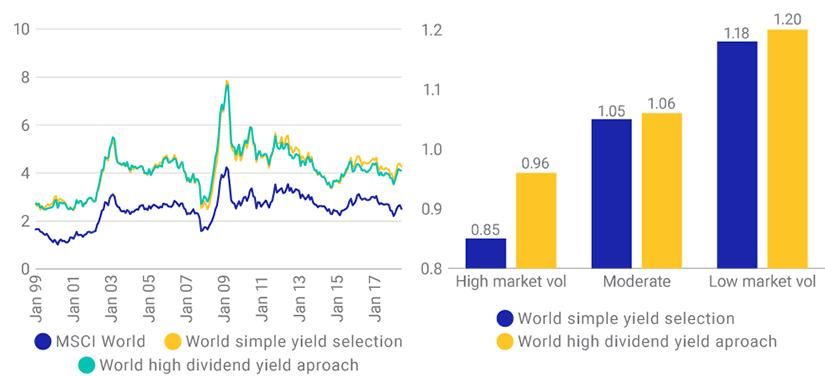

Comparing the simple yield selection and high dividend yield approaches in term of dividend yields, we see the high dividend yield approach appeared to give up 10 bps of trailing yield. However, the realized yield3 was, in fact, the same as it was for the simple yield selection. Additionally, the realized yield delivered by the high dividend yield approach was more consistent and stable compared to expectations based on trailing yield.

Of particular significance was that, during periods of high market volatility,4 the average realized yield-to-trailing yield ratio for the simple yield selection approach dropped by 15%. The high dividend yield approach, on the other hand, was more resilient and delivered, on average, 96% of the trailing yield during high volatility conditions.

High dividend yield approach proved more resilient

Realized yield (%) Realized-to-trailing yield ratio

As seen earlier, the high dividend yield approach also performed better in terms total return and lower volatility over the past 20 years. It outperformed the simple yield selection by over 100 bps per year with a volatility 1.3 percentage points lower. The robustness of the approach was particularly visible during periods of economic and market stress, such as the GFC, the European sovereign debt crisis in 2011 and more recent periods.

Performance of high dividend yield approach proved more resilient

Relative performance of high dividend yield strategy vs. simple yield selection approach

Screening the investment terrain

With central banks continuing to cut rates and bond yields at near term historical lows, many institutional and retail investors have turned to high dividend-paying equities to seek their income needs. While trailing high-yield equities could be a decent proxy for investors looking for yield, there is some reason for caution. Although a simple yield selection produced some good results, supplementing it with yield trap screenings helped identify potentially more stable higher-yield securities. In our analysis, doing so helped improve total returns with lower volatility and without compromising on delivered yield — particularly during highly uncertain economic and market times.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Gupta, A., Balint, I., Jain, V., and Melas, D. “Riding on Momentum: Understanding Factor Investing.” MSCI Blog, Dec. 15, 2015.2Lim, E., Hung, R., Chia, C., Barman, S., and Muthukrishnan, A. 2015. “Flight to Quality: Understanding factor investing.” MSCI Research Insight.3Defined as the yield delivered in the following 12 months based on return differential between gross and price return series.4High-market volatility regime is defined as the period in which the average (over a period of one year) Cboe Volatility Index (VIX) levels are in the top 10th percentile of historical rolling average VIX levels. Low-market regime corresponds to the bottom 10th percentile of historical rolling average VIX levels.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.