Beware of FRTB Cliff Effects. Sharp Curvatures Ahead.

Blog post

June 20, 2019

- The revised Basel Committee on Banking Supervision market-risk capital standard contains a small surprise with potentially big implications for banks: Cliff effects remain in the framework, despite the committee's attempt to remove them.

- Banks with more exposure to derivatives and other assets with optionality are more vulnerable to these cliff effects — or steep changes in the capital charge arising from minor variations in portfolios or market conditions.

- Prior to trading in and out of assets with optionality, banks' risk managers can model the impact of any new positions through "what-if" calculations.

Curvature cliff effects: One source eliminated, another remains

In March 2018, the committee reopened the 2016 version of the FRTB for consultation with the industry and other stakeholders.2 The BCBS did so, in part, to address a discontinuity in the aggregation of the curvature capital charge in the standardized approach.3, 4 The 2019 revised standards eliminated what was previously identified as a source of cliff effects in the curvature-charge aggregation, yet left the basic functional form unchanged.5 As a consequence, the curvature risk capital can still be unexpectedly sensitive to changing portfolio composition. The 2022 target date for the global implementation of the FRTB is approaching, and banks face new European Union reporting obligations as early as 2020. To help with these demands, banks may choose to consider this sensitivity in their pre-trade processes.6

When trade size matters more than expected

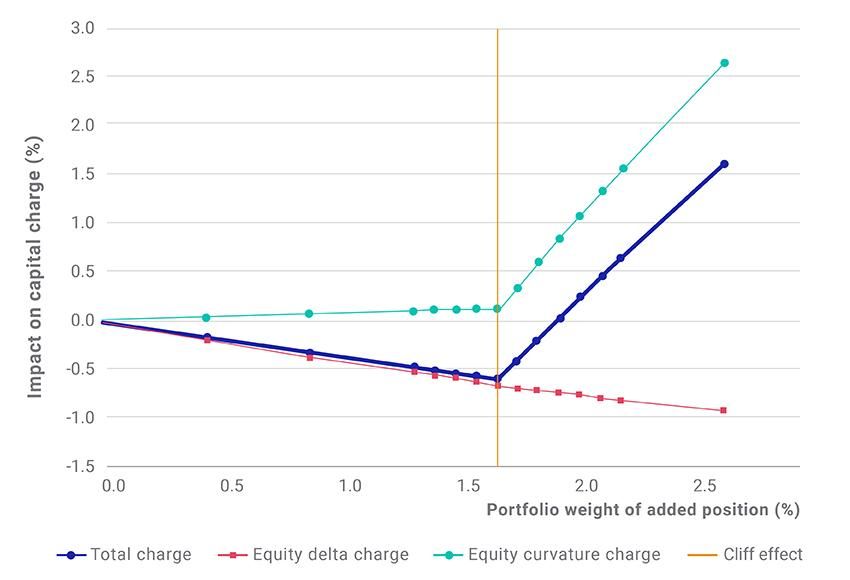

We analyzed the impact of adding a new equity-option position to a hypothetical portfolio of 99 options on constituents of the MSCI USA Index. The blue curve in the exhibit below shows the percentage impact on the total capital charge as a function of the weight of the added position. This function is highly nonlinear: around a 1.6% weight for this specific portfolio. Rules of thumb don't work well here: Even doubling the size of the what-if position to 2% from 1% changes the sign of the capital impact. The curvature charge is responsible for the behavior, as indicated by the separately shown impacts on equity delta and curvature charge (the red and turquoise curves below).

What-if analysis of adding a derivative position to a portfolio

Source: Our calculations used the FRTB module of MSCI's RiskMetrics® RiskManager®. Weights were measured as delta-adjusted gross notional values.

Yesterday's capital-charge impact is not a guarantee of today's

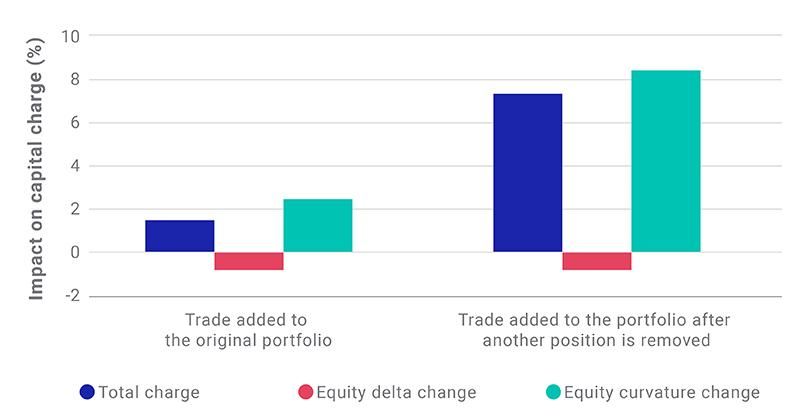

We also examined the cliff effect from a complementary viewpoint. In the left-hand side of the exhibit below, we display the capital-charge impact of a given trade, upon adding it to a hypothetical portfolio of 97 stock options on the MSCI USA Index's constituents. On the right-hand side, we display the impact of the same trade, added to the same portfolio, but with one of the 97 stock options removed. The removal more than quadrupled the effect of the new trade, even though the removed trade only had a 1.4% weight.

Again, the curvature charge is responsible for the unexpected increase, while the delta charge is hardly affected. Market movements may similarly alter the impact due to the cliff effect in the aggregation, even for an unchanged portfolio.

Effect of changing the portfolio on the what-if analysis

Our calculations used the FRTB module of MSCI's RiskMetrics® RiskManager®. Weights were measured as delta-adjusted gross notional values. The weight of the what-if position is 4.0% of the original portfolio.

Any optionality warrants accurate pre-trade checks

The observed behavior is an inherent property of the FRTB's square-root formula used for curvature aggregation, while the delta and vega4 charges are not affected, according to our analysis. We can expect cliff effects when the charge is zero or near zero for a regulatory "bucket" of risk factors,7 causing the sensitivity of the curvature charge to abruptly jump from very low to very high. Our observations are pertinent to all options — including swaptions, foreign-exchange and commodity options — not just equities, because the requirements are identical for all risk classes. Risk managers may therefore wish to be aware of the importance of pre-trade checks, to accurately gauge the impact of any new positions with optionality.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 The BCBS initiated the “fundamental review of the trading book” (FRTB) following the 2007-09 crisis to address structural shortcomings of the earlier framework for market-risk capital requirements. See: “Minimum capital requirements for market risk.” Basel Committee on Banking Supervision, Feb. 25, 2019.2 “Consultative Document: Revisions to the minimum capital requirements for market risk.” BCBS, March 22, 2018.3 The FRTB’s standardized approach applies to the trading book of all banks, either directly or by providing a floor value for more sophisticated approaches. It is based on the portfolio’s sensitivities to market movements and determined using regulatory risk weights and aggregation formulas.4 The delta charge capitalizes portfolio losses due to potential changes in market-risk factors based on linear sensitivities. The curvature charge captures additional risk in option positions whose value is a nonlinear function of risk factors. The vega charge is assigned on the basis of sensitivities to changes in implied-volatility risk factors.5 “Explanatory note on the minimum capital requirements for market risk.” BCBS, Jan. 14, 2019.6 “Regulation (EU) 2019/876.” European Parliament, May 20, 2019.7 A related issue with the delta charge in an early draft of the FRTB was described in an industry comment letter: “ISDA/GFMA/IIF further response to the BCBS’s TBG on sensitivity based approach (firm wide quantitative impact study).” ISDA, Global Financial Markets Association and Institute of International Finance, July 31, 2014.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.