Beyond headlines: How markets responded to US-China trade talks

Blog post

May 9, 2019

For more than a year, investors have confronted risks arising from U.S.-China trade tension and the possibility of a full-on trade war. This week, risks appeared to rise even further as headlines warned of a pending escalation of hostilities. The market volatility resulting from this ongoing trade dispute has had substantial, real-life impact on equity portfolios, but also provided a wealth of data to examine the impact of trade-war risk on global markets. Our analysis suggests that changes in equity-market valuations, analysts' consensus earnings estimates and data on companies' revenue exposure are metrics that provided insight into recent market and sector performances.

Did low relative valuation boost Chinese stocks?

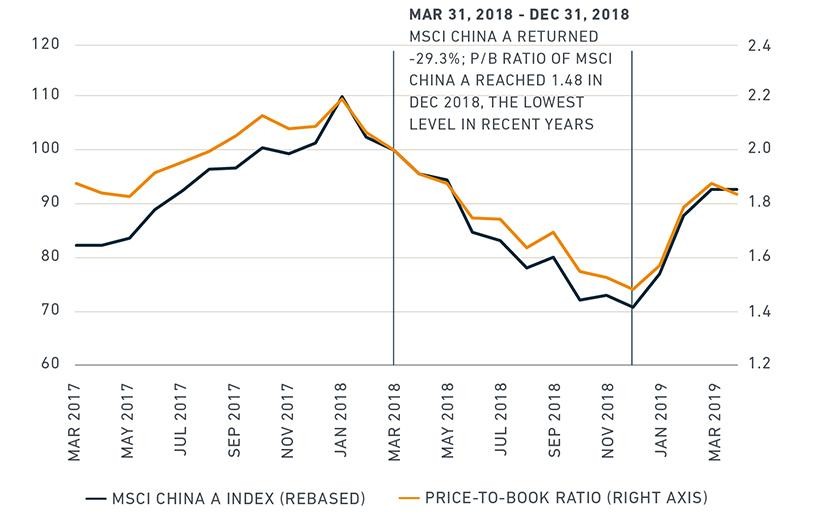

The rally in Chinese equities earlier in the year might have been partly due to their lower valuations relative to global markets after sharp declines during the last quarter of 2018. Since the start of the trade dispute to the end of 2018, the China A shares market, represented here by the MSCI China A Index, declined more than 25% — to a four-year low — compared to the MSCI USA Index. And as shown in the exhibit below, the 2018 selloff also compressed the A shares' average price-to-book ratio to a multiyear low.

Market valuation and performance of China A shares during the past two years

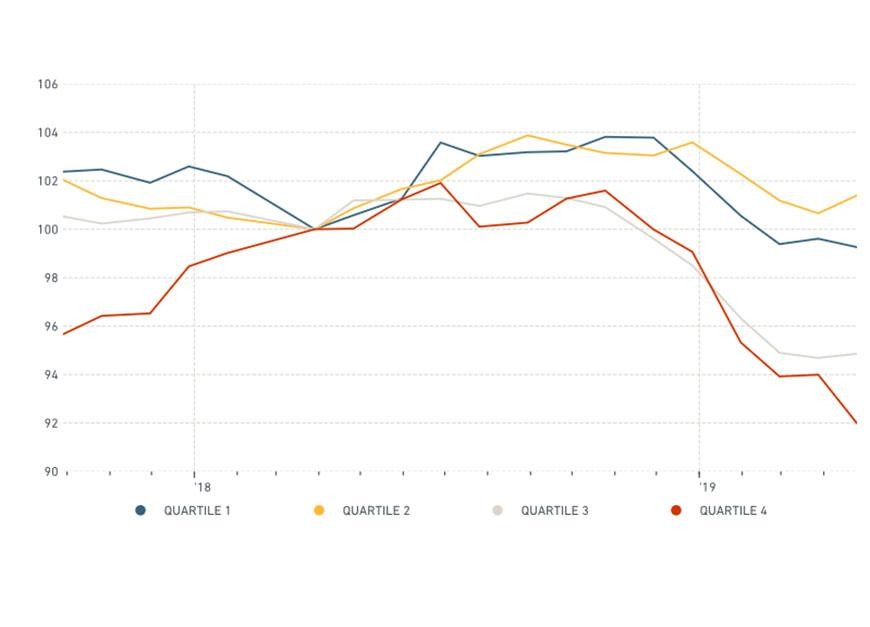

Trade-war risk might have driven revisions to analysts' earnings estimates

The exhibit below shows the historical revisions of 2019 earnings estimates for companies in the MSCI USA Index — broken down into quartiles based on their revenue exposures to China.1

Until mid-2018, it appears that analysts were gradually revising their 2019 earnings estimates upward for the U.S. companies most exposed to China (quartile 4). During the second half of 2018, however, consensus earnings for companies with above-average exposure to China (quartiles 3 and 4) got revised downward, amid rising perceived risk of an imminent trade war. Heading into the reporting seasons in January, 2019 earnings estimates were revised further downward — and more significantly for companies with higher China exposure, as many of them cited a negative outlook due to the impact of the U.S.-China trade conflict.2,3

Earnings revisions for MSCI USA Index companies ranked by revenue exposure to China

Note: Quartile 1 (4) comprises the 25% of MSCI USA Index stocks with the lowest (highest) revenue exposure to China. Average revenue exposures to China for stocks in quartiles 1-4 are 0.1%, 3.1%, 7.0% and 19.1%, respectively, based on MSCI Economic Exposure Data Methodology, as of March 28, 2019.

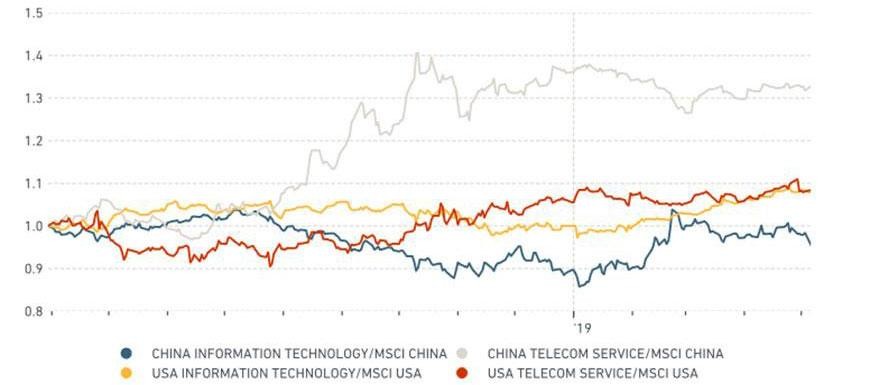

Economic exposure appears to have mattered

Companies' particular economic exposures seem to have made them more or less sensitive to trade-war risk. We used the MSCI Economic Exposure Data Methodology to try to identify potential trade-related risks and opportunities at the sector and stock levels.4 For example, as shown in our earlier blog post, the information-technology sectors in both the MSCI USA and MSCI China indexes were highly exposed to the Chinese and U.S. markets, respectively.5 By comparison, the communication-services sectors in both indexes derive a much smaller portion of direct revenues from the other country.

As a result, information technology underperformed, while communication services outperformed, in both the MSCI USA and MSCI China indexes during Q2-Q4 of 2018, when there was heightened risk of an imminent U.S.-China trade war. The information-technology sector in both indexes reversed 2018 underperformance during Q1 2019, when there appeared to be positive progress in the U.S.-China trade negotiations.

Relative performance of information-technology and communication-services sectors in MSCI USA and MSCI China indexes

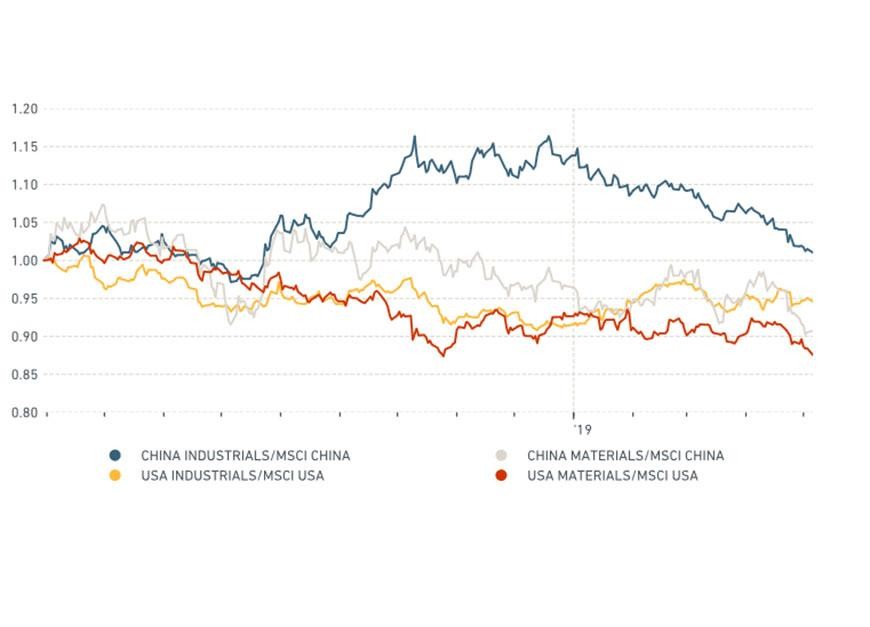

In addition, the MSCI USA Index's industrials and materials sectors had much higher revenue exposure to China than the MSCI China Index's industrials and materials sectors had to the U.S. This difference in risk exposures contributed to better relative performance of both sectors in the MSCI China Index than that of their U.S. counterparts during Q2-Q4 of 2018.6

Relative performance of industrials and materials sectors in MSCI USA and MSCI China indexes

Looking beyond headline risk

Whether or not China and the U.S. strike a trade deal in 2019, the potential for geopolitical conflict between the world's two largest economies represents an ongoing risk to global economic growth and market performance. Investors may wish to consider reading beyond the news headlines to understand what drives the underlying equity-market performance.

The author thanks Chin Ping Chia for his contribution to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The calculation is based on median estimate of pre-tax-profit figures from the I/B/E/S Estimates database. We rebase the aggregate earnings estimate number to 100 as of March 29, 2018, for a better comparison.2For instance, see: “What we learned from this earnings season: Trade war is clouding outlook.” CNBC, Feb. 14, 2019; “Bunge's Latest Profit Warning Shows the Toll of the U.S.-China Trade War.” Bloomberg, Jan. 22, 2019.3We did a similar analysis for MSCI China Index companies and found that Chinese companies with more than 25% revenue exposure to the U.S. saw more than 50% downward revisions in 2019 earnings since early 2018.4 “MSCI Economic Exposure Data Methodology.” MSCI (2013).5These examples are based on Global Industry Classification Standard (GICS®) sectors. A similar analysis can be conducted at the individual stock level.6This relative outperformance may have been even stronger if one adjusts for the high market beta of both sectors.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.