CDS Hedging: Exploring all the Options

Blog post

January 23, 2019

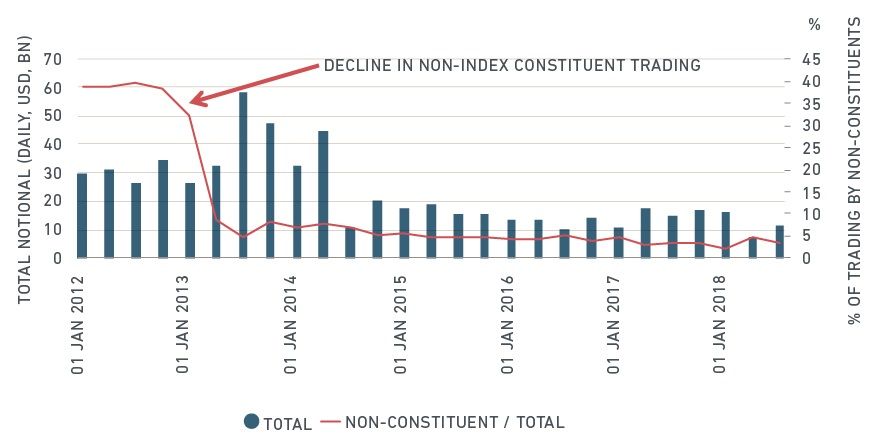

The credit-default swap (CDS) market previously offered a cost-effective means to make short-term hedges or place bets on an individual issuer's credit. However, since 2014, trading in these derivative products has been concentrated in members of basket CDS indexes, such as Markit CDX and Markit iTraxx, as illustrated in the exhibit below. Investors looking to hedge individual credit exposure may want to scrutinize the effectiveness of using CDS as a hedging strategy and consider all the options available to hedge risk.

Decline in single-name CDS trading

Bond spreads may provide deeper insights

In certain cases, bond spreads have provided a more reliable source of insight than CDS spreads.

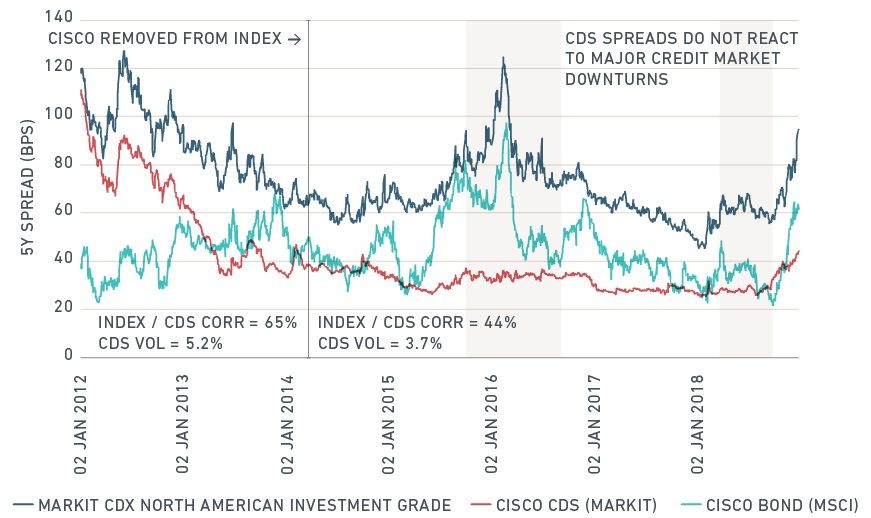

Let's consider technology group Cisco Systems, which was removed from the Markit CDX North American Investment Grade Index in March 2014 (see exhibit below). Prior to its removal, the CDS spread generally tracked the overall investment-grade market spread level (as measured by the Markit CDX index spread). Since its removal, the CDS spread has failed to track the Markit CDX index spread. In contrast, Cisco's bond spread has continued to track overall market spread levels since 2014.

Cisco CDS spreads have not reacted to recent credit market downturns

The behavior of spread volatility – the variation in spread levels – is the key input to understanding risk exposures. The CDS spread return correlation with the Markit CDX index declined from 65% to 44% after Cisco was removed from the index, and its risk declined from 5.2% to 3.7%.2 The bond spread risk was more consistent: prior to 2014, the spread volatility was 9.6%; after 2014, it was 9.0%. The reduction in CDS spread volatility offered a misleading signal that Cisco credit had become less volatile after 2014.

A scarcity of trading activity in the CDS market has historically meant that dealers had less incentive to publish reliable quotes. Consequently, the quoted spreads of non-index constituents have not necessarily reflected the true cost of CDS protection. In contrast, the bond market has provided more meaningful insights in recent periods. The bond market differs from the CDS market in a number of ways: although it can be challenging and/or costly to trade an individual bond, reliable bond prices are necessary for official net asset value (NAV) reporting across broad index universes, for benchmarked managers and ETFs.3 An aggregate issuer bond spread curve built from the most liquid bond prices offers a robust measure of issuer credit.

Access to liquidity may not be that easy

However, if there is general concern about an individual issuer credit exposure, it may not be feasible to exit a cash bond position quickly or cheaply enough.4 So for a short-term hedge for a large issuer exposure, apart from the CDS market, what alternatives exist?

One possibility is an equity option. Historically, large credit and equity downturns tended to occur simultaneously. Should this relationship continue to hold, which may or may not occur, then an out-of-the-money put option on the issuer's equity would provide an alternative credit hedging mechanism. The drawback is that the correlation between equity and credit downturns is only in the extreme, so this may be less effective as a mark-to-market hedge. However, in contrast to the default event underlying the CDS, the equity price underlying an option is more transparent, so if the equity price declines, it is contractually guaranteed to be reflected in the option value.

For credit investors looking to use CDS as an effective tool for hedging risk, as part of their overall portfolio management, our analysis highlights the value in reviewing all available options.

1 This publication includes and/or relies on Trade Information Warehouse data ("TIW Data") provided by The Depository Trust & Clearing Corporation and/or its affiliates. Use of TIW Data is subject to the Terms of Use set forth at http://www.dtcc.com/terms.

2 Risk is measured as the weekly relative spread return standard deviation; correlation is between the weekly relative spread returns.

3 For example, the Markit iBoxx USD Liquid Investment Grade Index contains roughly 400 issuers and nearly 2,000 bonds, compared to 125 issuers in the Markit CDX North America Investment Grade Index.

4 Based on the MSCI Bond Liquidity Model, the most liquid Cisco bond issued since 2016 has a relative price bid/ask spread of 11.5bps (CISCO SYSTEMS INC 2.2 02/28/2021). .

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.