Chinese convertibles: Equities in fancy dress?

Blog post

October 14, 2019

- The market for bonds that convert to China A shares has grown considerably in the last two years.

- Some characteristics of A-share convertible bonds may lead investors to consider them essentially as equities.

- But our analysis illustrates the importance of these bonds' non-equity-like characteristics, which dedicated modeling could help investors understand.

Chinese companies overtook US peers in convertible issuance in 2019

Source: Reuters

Common characteristics of China convertibles

Even at their time of issue, many of these securities act more like equities than bonds, because of specific features particularly prevalent in China2:

- Low conversion price (strike price): A low strike price means conversion probability can be relatively high even at the time of the convertibles' issue.

- Dilution protection: If additional equity is issued at a price lower than the current price, the conversion price may be lowered, mitigating the adverse effect of dilution.

- Dividend protection: Investors may be compensated for missing the dividend payments the underlying stock provides (to which they are otherwise not entitled until conversion) by the lowering of the conversion price. (This has become the norm for non-Chinese markets too.)

- Compensation if no conversion: Some convertibles may redeem above par (110% of notional amount, for example), which may partially mitigate the downside risk that the underlying equity underperforms and the bond is not converted.

- Annual reset: In order to mitigate the effect of declining equity markets, issuers may periodically lower the conversion price, so that conversion becomes more beneficial to bondholders.

The importance of resets: Out-of-the money convertibles can go in the money

Equity-like is not the same as equity

Does this reset feature make these bonds behave essentially like equities? Not really. According to our analysis using MSCI's convertible-bond model, there are more to A-share convertibles than just their equity-like characteristics.

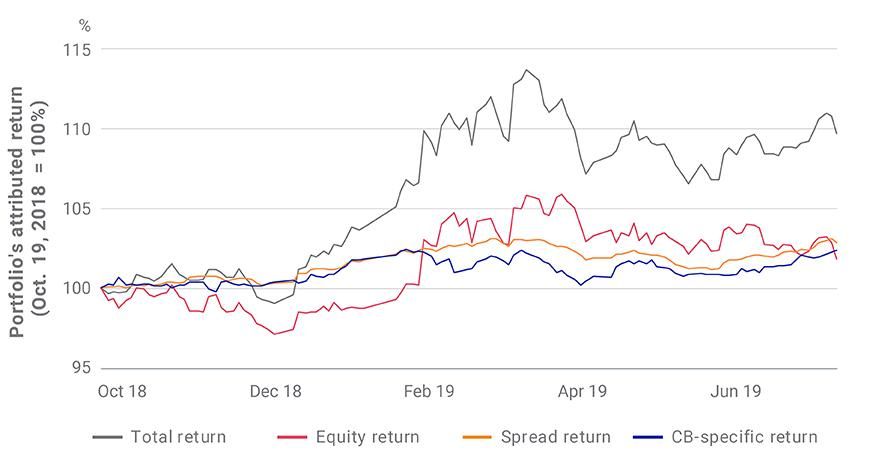

We analyzed a hypothetical portfolio consisting of all bonds that convert to A shares.3 We then used performance attribution to analyze return drivers since October of last year. We looked at traditional factors, such as equity and spread, plus an additional convertible-specific factor, which accounts for peculiarities of the Chinese market.

The importance of non-equity drivers in Chinese convertibles' total returns

The weights of our hypothetical portfolio are proportional to the total outstanding amount. Our performance period spans Oct. 19, 2019, through Aug. 1, 2019. Source: Reuters

A-share convertibles' non-equity-like features are complex

One can immediately see that, beyond the equity factor, the spread and convertible-specific factor were important contributors to these convertible securities' total returns during the period of our analysis. These last two contributors may reflect particular features of these convertibles, specifically the annual resets that serve to increase the value of convertibles as the underlying equities are declining. The spread and convertible-bond-specific factors may have also been driven by increased demand from yield-hungry fixed income investors.

If A-share convertibles' issuance remains strong, these securities may become a bigger part of global bond portfolios. Because of these securities' China-specific features, they warrant dedicated analysis. Investors can use models that account for these features to derive insight into this market and support their portfolio decisions.

The author thanks Michael Hayes, Andy Sparks and Tong Yu for their contributions to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1China A shares are offered by companies in mainland China that trade on the Shanghai Stock Exchange and Shenzhen Stock Exchange.2There is nothing stopping European or U.S. companies from issuing convertible bonds with these features, but these features are more prevalent in China than in other markets.3The universe of bonds was restricted to those bonds with a minimum quality threshold for price data.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.