Corporate Disclosure in a TCFD World

Blog post

September 24, 2018

In June 2017, the Task Force on Climate-related Financial Disclosure (TCFD) released climate-related disclosure recommendations to companies and investors that included a framework for better company disclosure and a request for climate scenarios as part of that disclosure.1 But for investors looking to incorporate environmental risk into their process, there might be a pretty big catch: We mapped over 140 MSCI ESG Research climate-related data points to the TCFD framework and found a significant gap between what investors need to know under these recommendations and what companies are telling them.

BETTER DISCLOSURE IS STILL A WORK IN PROGRESS

Backed by the Bank of England Governor Mark Carney, the TCFD framework has been widely endorsed by many of the world's largest investors as a critical step forward allowing for effective capital allocation and asset pricing in the face of growing climate related risks.2 The most extensive data available is carbon data, specifically scope 1 and 2 emissions, which have steadily improved looking backwards through our CarbonMetrics data. As of August 2018, over 55% of the constituents of the MSCI ACWI Index had reported on their carbon emissions, up 10% since 2016.

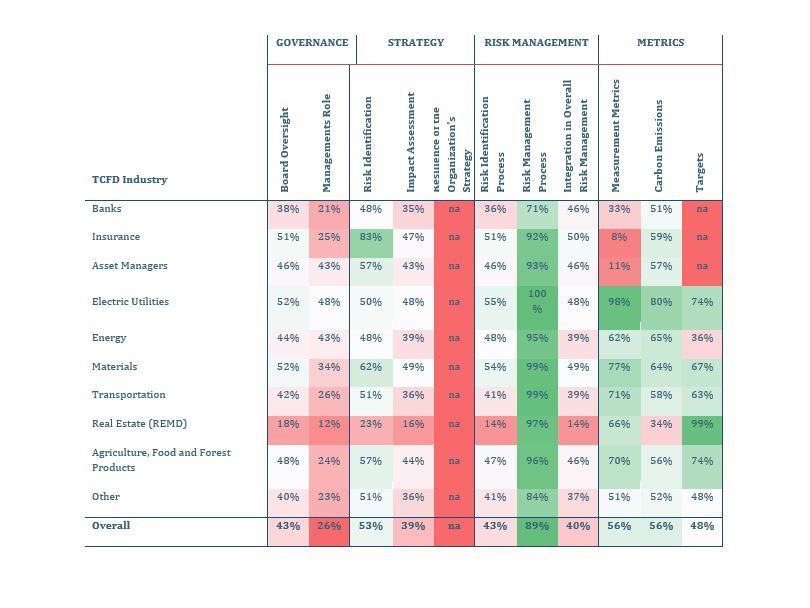

We also were surprised to find that the number of qualitative disclosures around governance and risk management have increased as well. In fact, 89% of the companies we analyzed reported at least some measures for managing carbon-related risks, though these were typically limited to energy efficiency measures or sourcing renewable energy.

MSCI ACWI Index constituents disclosing TCFD criteria

Data as of August 2018

However, if carbon and climate governance represent the best of TCFD-related disclosure today, the data our clients viewed as most valuable during our consultations3 with them still is out of reach. Forward-looking disclosure around strategies and targets, a part of the TCFD recommendations, represent the weakest disclosures in our analysis. Only 11% of MSCI ACWI Index constituents disclosed all TCFD recommended information regarding their carbon emissions reduction target. Of the remaining firms:

- 51% had not disclosed any carbon emissions target.

- 38% had disclosed targets without further specifying the base year, targeted reduction per annum or target year.

- Fewer than 3% of the constituents of the MSCI ACWI Index as of Aug 18 had mentioned scenario considerations and/or analysis in their disclosures.

- Even for companies that disclosed forward-looking indicators, almost none in the set had science-based targets aligned to a 2⁰C warming scenario as of Aug. 31, 2018.

Oil & gas and exploration & production companies conducting scenario analysis

Data as of August 2018

HOW CAN INVESTORS MEASURE WHAT THEY CANNOT SEE?

As investors look to implement TCFD's recommendations, narrowing the disclosure gaps might be a key focus. This may come through direct engagement with non-disclosing or poorly disclosing companies, as with the O&G sector, or through collective engagement schemes such as the Climate Action 100+, which has been backed by 296 institutional investors representing USD 31 trillion in assets.7 But engagement can be a long process and it is likely to take years for companies' scenario reporting to generate comparable, investment-relevant information. So what options are available for investors who are not willing to wait?

Some institutional investors are using proxies to measure the resilience of their portfolios and allocate to investment strategies informed by climate change data. Using our ESG Ratings data, it is possible to approximate companies' vulnerability to climate risks based on the specifics of their business activities and location of their physical assets; and stringent targets – combined with a track record meeting past targets – can provide a proxy of a company's adaptability and preparedness relative to peers.

These types of measures may be effective interim tools as engagement processes unfold and disclosure (hopefully) improves.

1 "Recommendations of the Task Force on Climate-related Financial Disclosures." (2017).

2 List of TCFD Supporters as of August 2018

3 In August and September 2018, MSCI consulted with 55 institutional investors around the use of climate scenarios including 29 asset managers, 20 asset owners, and 6 other stakeholders (investment consultants, etc.). The consultation included 30 participating institutions in Europe, 20 institutions in the Americas, and 5 institutions based in the Asia-Pacific region

4 Task Force on Climate-related Financial Disclosures. (2017). "Technical Supplement: The Use of Scenario Analysis in Disclosure of Climate-related Risks and Opportunities,"

5 Source: MSCI ESG Research; Ranked by market cap as of August 2018

6 MSCI ESG Research based on analysis of 97 shareholder resolutions tied to '2-degree scenarios' and 'reporting on climate change financial risks'.

7 Climate Action 100

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.