Could Investment Grade Be as Risky as High Yield?

- The gap between the market risk of high-yield (HY) and investment-grade (IG) corporate-bond indexes has narrowed to almost zero when measured by traditional value-at-risk models.

- One key reason for this convergence is the increasing duration of IG debt, but HY and IG's having nearly the same risk may still be puzzling to investors.

- We found that explicitly incorporating measures of default risk significantly increases risk levels in HY relative to IG and could potentially give investors a better picture of the risk of holding corporate debt.

IG and HY Risks Are Comparable, According to Traditional Market-Risk Models

Fixed-income investors often use models to forecast future distributions of interest rates and spreads to estimate their bond investments' market risk. As reflected by market-weighted benchmarks, we found that the IG and HY corporate-bond markets now have comparable market risk when measured by MSCI-derived VaR at the 99.9% quantile.

How extraordinary is the current situation? To answer this question, we plotted below the 99.9% market VaR for a one-year horizon estimated for every quarter back to 2016. During the early stages of the COVID-19 market crisis, HY risk increased significantly compared to IG. Since then, markets calmed substantially. Though convergence of HY and IG risks is not unprecedented, the difference between them was at its lowest level of the past two years, as of February 2021.

Recent IG/HY Market-Risk Convergence Is Noteworthy Though Not Unprecedented

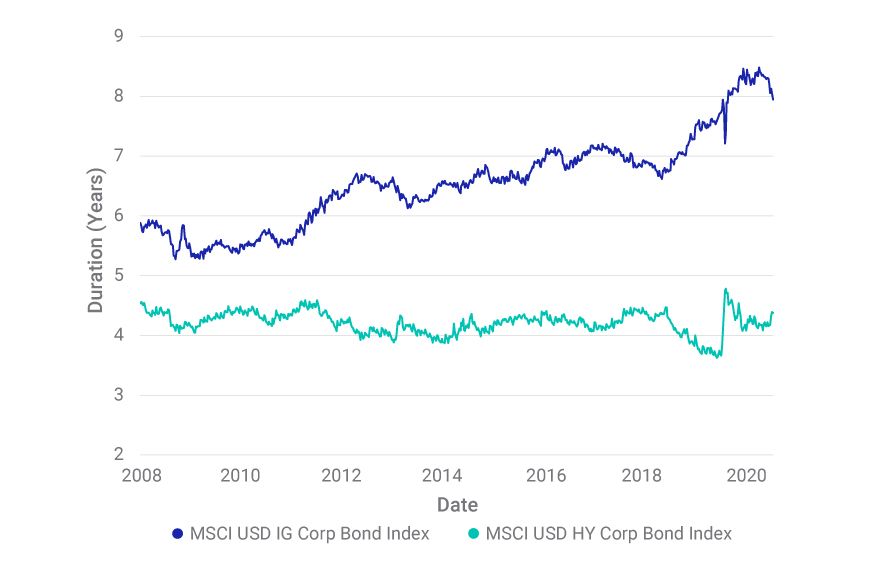

Long Duration of the IG Benchmark Increased Market Risk

Model-derived measures of market risk partly reflect volatility in credit spreads and government-bond yields. But market risk is also affected by bond-market duration.1 The duration of the IG market sharply increased over the past two years. As of the first quarter of 2021, it has risen to around 8 years — a record high and about twice the HY index's duration, which has been fairly stable over the years, as the exhibit below shows. The convergence in market risk between HY and IG can be mostly explained by this divergence in bond durations between the two credit segments.2

Between IG and HY, Duration Divergence Helps Explain Risk Convergence

Consideration of Defaults Allows a Fuller Comparison

While measures of market risk may be similar between the two credit segments, the HY long-term average default probability is approximately 20 times higher than that of the IG index's universe.3 Market-VaR models incorporate the variations in default expectations via credit-spread volatility, but they might fail to account for the dynamics of actual defaults. Such jump-to-default events have low probability, but are associated with large losses; they therefore are important in determining a portfolio's tail risk.

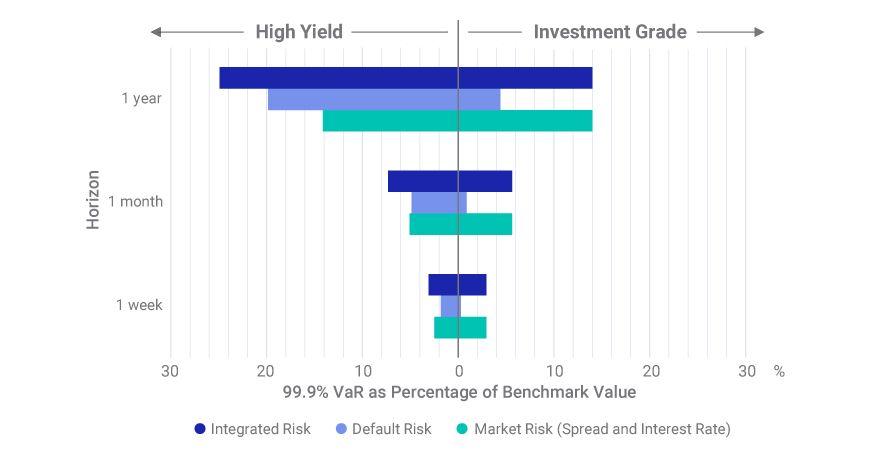

To explore how explicit consideration of default events could impact measured risk, we compared three measures: the MSCI market VaR; a credit VaR measuring default risk only;4 and an integrated VaR capturing movements of both market-risk factors and default events.5 The exhibit below shows the results (green bars for market VaR, light blue bars for credit VaR and dark blue bars for integrated VaR). We analyzed three different horizons: one week, one month and one year.

Different Models Produce Different Views of IG and HY Risk

We used the MSCI USD Investment Grade Corporate Bond Index and MSCI USD High Yield Corporate Bond Index as benchmarks to represent HY and IG markets.

As the risk horizon is extended beyond one week, defaults turn into a key risk driver for HY. At the one-year horizon, the pure default risk (19.8%) outweighs the market risk (14.1%), and the integrated market-default risk (24.9%) becomes almost twice as large as the market risk itself. In the case of IG, default risk remains modest even at the one-year horizon (4.4%), and the integrated risk is indistinguishable from market risk.

In short, investors might want to consider explicitly including defaults in their risk modeling, which may help better differentiate the HY and IG bond universes in long-term risk management and asset allocation.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Duration measures the (first-order) sensitivity of bond price to changes in yields or spreads. For fixed-coupon bonds, it increases with maturity.2Chappatta, Brian. “Bond Market’s Scariest Gauge Is Worse Than Ever.” Bloomberg, Jan. 14, 2021.3Based on market-value-weighted averages of default probabilities of benchmark constituents from Moody’s average one-year credit-rating transition matrices, for 1983 to 2019.4We used MSCI’s RiskMetrics® CreditMetrics® portfolio credit model, assuming par value for non-default securities and a fixed recovery amount for defaulted issues.5In this model, we simulated default events alongside interest-rate and credit-spread risk with the same Monte Carlo engine. We priced non-default securities according to the simulated market scenarios, while we assigned a fixed recovery amount to the defaulted ones.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.