COVID-19’s Uneven Impact on Office Vacancy

- The vacancy rate of offices in the MSCI Global Annual Property Index rose to 10.4% in 2020. This was lower than the previous cycle's peak vacancy rate, but the percentage of fully leased buildings reached an all-time low.

- In our analysis, 55% of offices saw no change in 2020 — the lowest in the index's 20-year history. At the same time, 26% of offices reported increased vacancy. This was the highest percentage since the index's inception and surpassed the 21% of 2009.

- Offices that remained fully leased through 2020 outperformed the index's overall office return, but properties that significantly reduced vacancy saw even better outcomes, even though their year-end vacancy rate was higher.

Vacancy Rate Below Past Peaks but Fully Leased Properties at Record Low

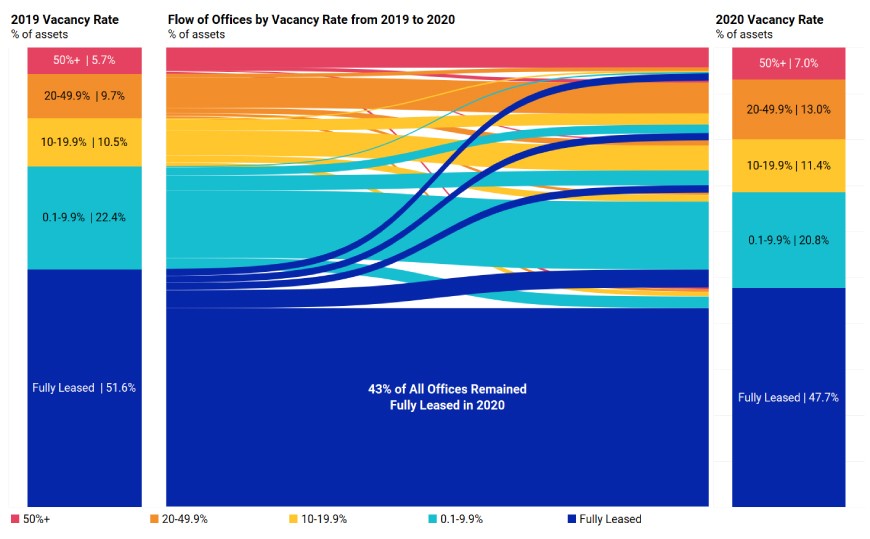

That there were fewer fully leased buildings at the end of 2020 than at the beginning does not mean every office property's vacancy rate rose. As the overall vacancy rate experienced its biggest one-year move since the 2008 global financial crisis, a larger percentage of office buildings experienced a shift in their vacancy rate than in previous years. At the end of 2020, there was a lower percentage of offices with a vacancy rate below 10%. While 43% of offices in the index remained fully leased throughout 2020, vacancies increased in 26% of office properties — the highest level in the index's 20-year history, surpassing the 21% of 2009.

At the same time, 55% of offices saw no change during the year, the lowest percentage since the index's inception in 2001. In 2009, 66% of offices reported no change in vacancy.

It wasn't all bad news, though. Despite the pandemic and increased work from home, 19% of office properties saw their vacancy rates improve during 2020. This is above the 2009 figure, when only 13% of offices managed to reduce vacancy.

Vacancy Up in 2020 as Fewer Offices Reported Stable Vacancy

Source: MSCI Real Estate

Uneven Flow: 43% of Offices Remained Fully Leased Though 2020

Source: MSCI Real Estate

Uneven Impact on Vacancy Bled Through to Returns

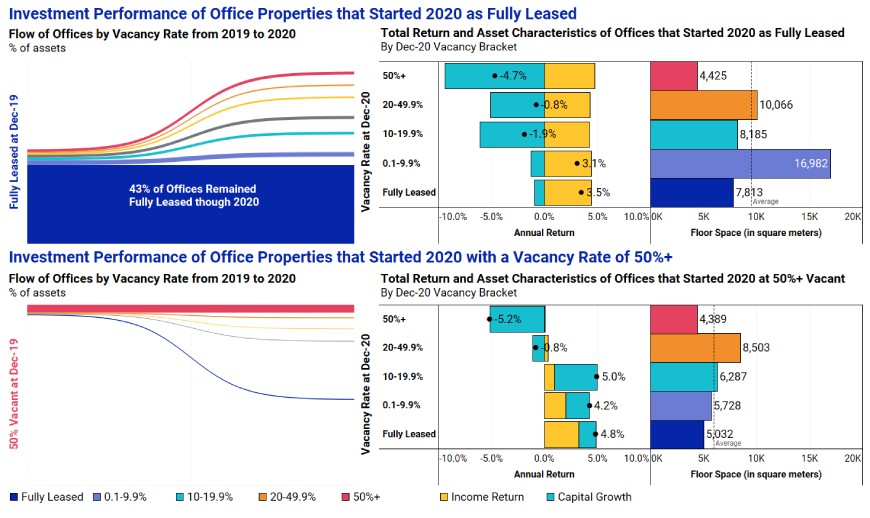

At the start of 2020, 52% of office buildings in the sample were fully leased. Those that remained fully leased throughout the calendar year produced a total return of 3.5%. This was 90 basis points more than the overall office total return of 2.6% recorded by the MSCI Global Annual Property Index.

The uneven impact on the office sector's vacancy rates and returns suggests that other factors also affected performance. Irrespective of starting vacancy, smaller assets will tend to have fewer tenants and are therefore more likely to be either fully leased or significantly (50% or more) vacant. We see smaller assets in the fully leased and 50%+ buckets for both charts in this exhibit.

Assets that started 2020 fully leased had similar levels of positive income return but their capital growth progressively deteriorated as vacancy increased. Meanwhile, offices that started 2020 at least half empty all had varying levels of comparatively weak income return. We found that office properties that significantly reduced vacancy produced better returns, even if their year-end vacancy rate was higher.

Comparing the two bottom brackets (50%+ and 20%-49.9%) of each bucket (starting fully leased and >50% vacant) reveals a similar total return. The difference was that offices that became more vacant during the year experienced much weaker capital growth. For these properties, income return was a saving grace and offset much of the negative capital growth.

Outperformance by Offices that Managed to Reduce Vacancy

Source: MSCI Real Estate

Even as more and more companies welcome back their office-based employees, many of the offices that emptied during the pandemic remain vacant, raising doubts over the office segment's future and concerns about a structural step-change in demand. As occupiers continue to consider their physical-office needs, new opportunities and risks might emerge. Investors may benefit from understanding how vacancy trends and their impact on returns vary across the market.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1We based our analysis on a sample of 7,461 office properties from the MSCI Global Annual Property Index. To be included, properties had to be held for all of 2019 and 2020. Developments and transacted properties were excluded, as were those with no recorded floor area and/or vacancy rate.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.