Creating a common language for factor investing

Investors need a clear and consistent way to talk about factors. For more than 40 years, MSCI has defined how investors use factors to analyze risk and return, from individual stocks to entire portfolios. Factors are important drivers of portfolio performance and are well documented in academic research. They are used to quantify how much risk and return is attributable to different countries, sectors and styles. With the recent growth in factor investing (also known as "smart beta"), investors increasingly are using "style factors," such as value, quality and momentum, to understand performance and create investment strategies. But there are a host of style factors used in the investment world, with varying definitions. This lack of consistent definitions has created demand for a common language and standards to describe these powerful influences on security and portfolio performance. In response, we have introduced a new standard, MSCI FaCS, for analyzing and reporting style factors in equity portfolios. In addition, we have created the MSCI Factor Box, an interactive tool using MSCI FaCS data to view factor exposures in funds compared to selected benchmarks. MSCI FaCS: The standard creates a common language and definitions around factors to be used by asset owners, managers, advisors, consultants and investors. Managers can use the framework to analyze and report factor characteristics, while investors and consultants can use the data to compare funds and monitor exposures over time using common definitions. The standard is based on the factor structure in MSCI's latest global equity factor risk model, the Barra Global Total Market Equity Model for Long-Term Investors (GEMLT). The standard groups the 16 factors of GEMLT into eight factor groups – Value, Size, Momentum, Volatility, Quality, Yield, Growth and Liquidity. The style factors in GEMLT are comprised of 41 individual metrics, or "descriptors." We display the structure of MSCI FaCS in the exhibit below.

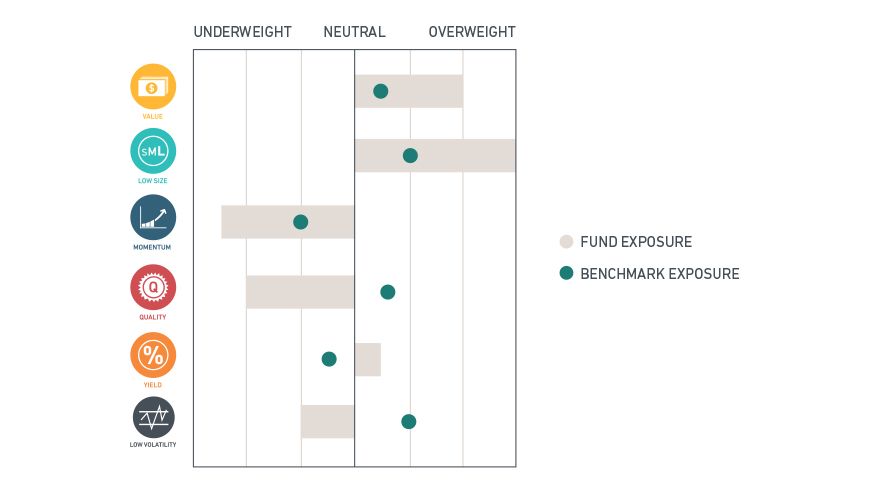

These style factors and groupings are relevant to actual equity portfolios, as an examination of over 3,000 actively managed mutual funds revealed . While fund exposures were generally highest to the target factor group implied by their fund names, we also saw that funds often had significant exposures to other factor groups. MSCI Factor Box: The Factor Box takes the data available from MSCI FaCS and presents it in an easy-to-use interactive format. This way, investors can readily compare factor exposure between funds and their benchmarks. Each of the six factors used have historically offered a return premium over long time periods (though results have varied over shorter timeframes). We display each of these factors — value, low size, momentum, quality, yield and low volatility — on the vertical axis. Investors can see how their fund compares to a benchmark. Meanwhile, stars indicate the chosen benchmark's exposure to each of the six factors.

Factor Box analysis of a hypothetical fund's factor exposures

MSCI FaCS offers the structure and standardization for evaluating, implementing and reporting on equity factors. While standards for countries and industries have existed for some time, a standard for style factors has not. We created MSCI FaCS to fill this gap. The MSCI Factor Box leverages the MSCI FaCS framework, providing investors with a new tool that can help them better understand factor exposures in current and potential holdings.

The author thanks Leon Roisenberg, Raman Aylur Subramanian and Dimitris Melas for their contributions to this post.

The author thanks Leon Roisenberg, Raman Aylur Subramanian and Dimitris Melas for their contributions to this post.

Further reading:

Introducing MSCI FaCS - read the research papers Introducing our latest Factor Innovation – MSCI FaCSTM What is factor investing? Measuring the impact of factors Improving stock selection in the age of big data Bridging the gap: Adding factors to indexed and active allocations Using Systematic Equity Strategies

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.