Credit binge hangovers have historically been a challenge

Blog post

November 9, 2018

Credit spreads and debt issuance are at historical levels, as credit markets show signs of overheating. History has shown that following an overheated credit market, long-term credit returns have been generally weaker, in absolute terms and relative to U.S. Treasurys; particularly for high yield (HY). Given the intensity of past credit binge hangovers, long-term investors may want to review their current asset allocation strategies.

HIGH AND TIGHT

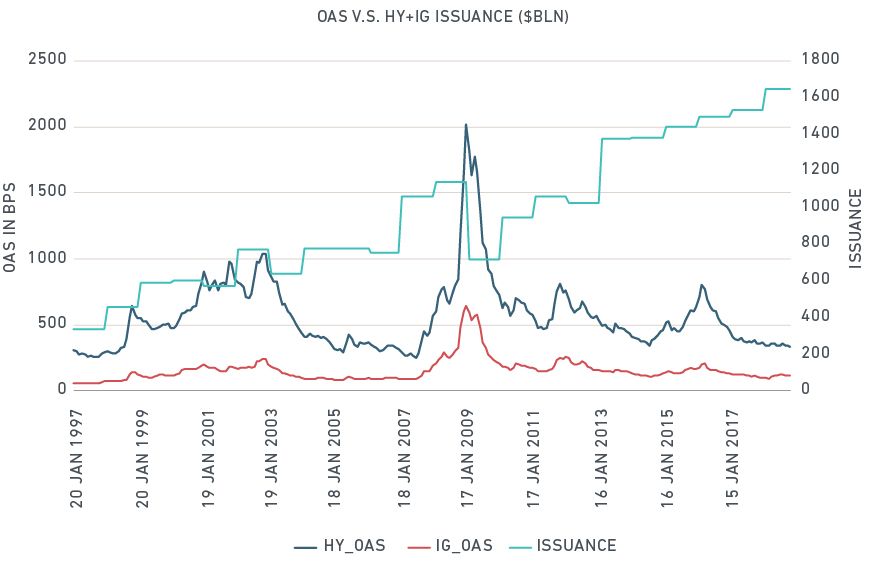

The impact of credit expansion on business cycles has been studied extensively in academia and by the U.S. Federal Reserve.1 The exhibit below shows issuance of investment grade (IG) and HY corporate bonds as of September 2018 is at historically high levels and their option-adjusted spreads (OAS) are close to historically tight levels. However, potential spread widening is only one factor that has previously driven credit investment returns. Coupon returns and collateral performance have also been key drivers. We analyze historical total returns of IG and HY and their relative performance over total returns of the US Treasury index.

HISTORICALLY HIGH ISSUANCE, HISTORICALLY TIGHT OAS

Source: SIFMA, ICE BofAML, used with permission

WHAT HISTORY SHOWS

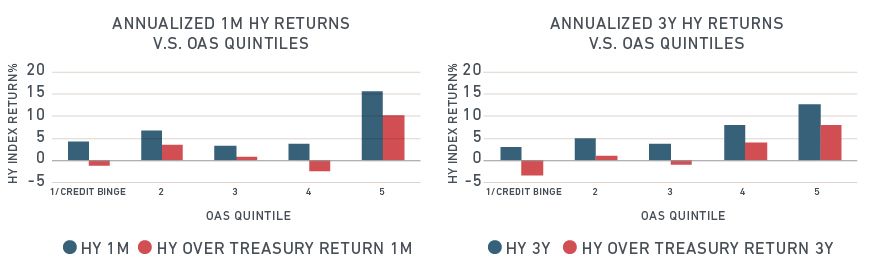

For our analysis, we looked at short- and long-term credit returns for IG and HY following a credit bull run. We compared 1-month and 3-year annualized total returns of IG and HY indices and their relative returns compared with the Treasury index, based on the monthly average of the OAS levels prior to the investment period. Our analysis is based on more than 21 years of data, from 1997 to September 2018.

The 3-year HY returns below illustrate the historical perils of investing in the HY sector after a credit binge (group 1/credit binge, which is the top quintile of monthly HY OAS levels). The absolute returns were generally lower and the average annualized returns for this group underperformed U.S. Treasurys by 327 basis points (bps) historically. This performance is distinctive from group 2 and 3 where HY OAS were also tighter than historical average levels. The patterns are less clear for 1-month returns. Often credit returns have exhibited a momentum effect as good returns attracted additional investments which drove further performance gains.

High yield market following a credit binge

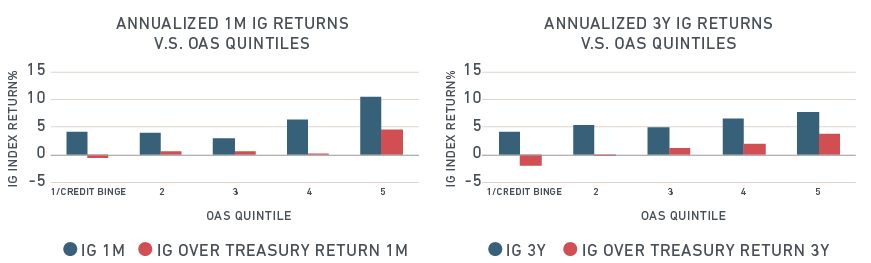

The exhibit below shows similar underperformance of the IG sector after a credit market bull run, albeit at a much less differentiating level. For group 1/credit binge (the top quintile of the monthly IG OAS levels), the subsequent 3-year underperformance against the U.S. Treasury index was approximately 181 bps annualized.

US investment grade market following a credit binge

Based on our analysis, historically tight OAS levels have often led to weaker absolute returns and weaker relative returns against U.S. Treasurys in the long term, particularly for HY. Given this history, long-term credit investors may wish to review their asset allocation strategies.

1 For example, "Overheating in credit markets: origins, measurement, and policy responses" Federal Reserve Symposium, Governor Jeremy C. Stein, February 07, 2013

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.