Credit in the COVID Crisis: Contagion, Valuation, Default

Blog post

May 6, 2020

- Diverging market measures after the onset of the COVID-19 crisis pointed to uncertainty in creditworthiness and default risks — particularly in the investment-grade market — which might be exacerbated by demand for liquidity.

- Today's wide bond spreads might be a sign of many different risks, including liquidity, risk premia and economic prospects — or some combination thereof.

- Elevated levels of correlation in credit markets could signal contagion risk, or the potential that price shocks and defaults in one sector may be significantly more likely to cause shocks in other credit sectors.

What Did Different Markets Tell Us About Default Risk?

After the onset of the COVID-19 crisis, U.S. investment-grade and high-yield bond prices first dropped significantly — and then rallied,1 after the Federal Reserve pledged to support the U.S. corporate-bond market.2

To understand the impact of the COVID-19 crisis on the broader credit market, we analyzed market-implied default probabilities for a basket of investment-grade and high-yield bonds.3 We modeled one-year default probabilities from bond spreads and compared them to default probabilities from the credit-default swaps (CDS) protecting against the default of the same issuer, as well as to default probabilities from CreditGrades, an MSCI model of equity-based distance to default.4

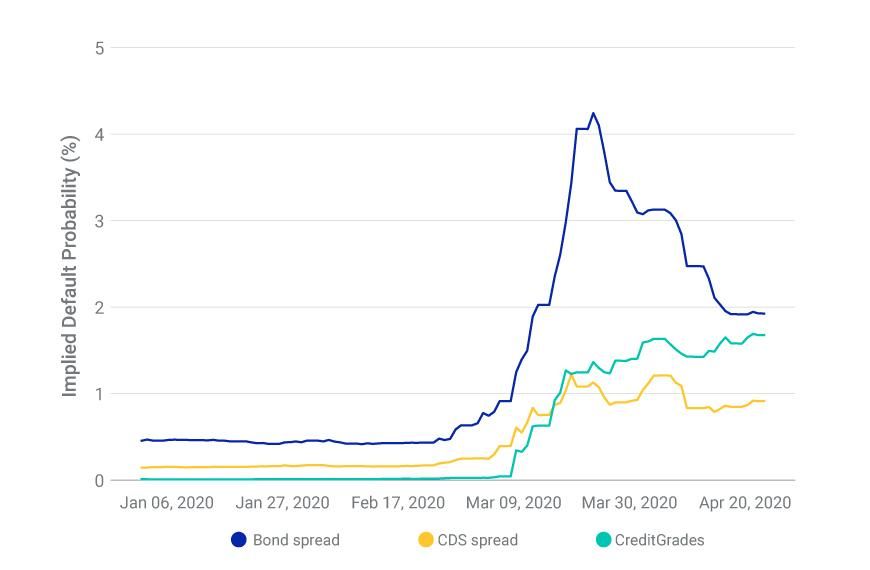

Implied Default Probabilities and Uncertainty Rose in Investment-Grade Bonds

Source: IHS Markit, S&P Compustat, MSCI

The onset of the crisis was marked by a sharp increase in the average implied default probabilities of the investment-grade bond basket. Indeed, spreads increased in credit markets,5 as equity prices dropped significantly. The dramatic spread widening in bonds may have been exacerbated by selling pressure6 from investors rushing for cash and thus hurting liquidity conditions,7 leading to bond-implied default probabilities increasing more than those derived from CDS or CreditGrades. Interestingly, these deviations may have implied arbitrage opportunities to some investors who buy bonds and default protection; they also suggest market fragmentation that has hindered that sort of activity.

With the announcement of emergency lending programs and asset purchases by the Federal Reserve on March 23, default probabilities implied by the bond and CDS markets declined significantly, in the former much more dramatically than the latter. The closing of the gap between bond valuations and the other two market-implied measures signaled the market's view of improving credit conditions and easing liquidity pressure.

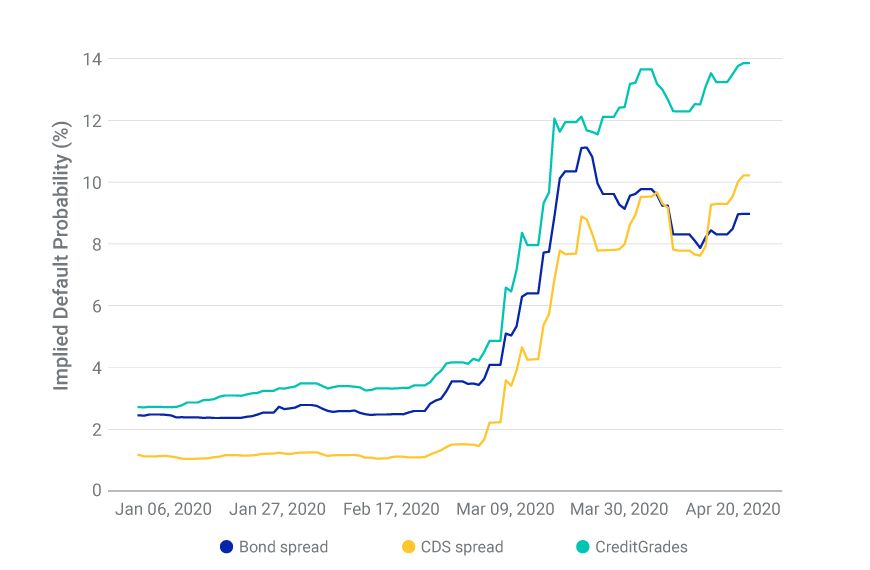

Implied Default Probabilities Rose Consistently in High-Yield Bonds

Source: IHS Markit, S&P Compustat, MSCI

The exhibit above plots the same measures for the high-yield market and gives us a very different picture. In the high-yield case, the three market measures of default risk moved more in sync until the trough of the selloff, not showing significant signs of relative liquidity-risk mismatch. This observation is in line with the more gradual sell-off in the high-yield market, compared to investment-grade bonds.8 Since the Fed's announcement, however, bond-implied default probabilities decreased to levels even slightly lower than those derived from the CDS market.

The divergence in measures of default risk and slippage in hedging relationships likely reflected uncertainty brought on by the crisis. But investors may want to consider that such periods of apparent uncertainty in creditworthiness might primarily reflect liquidity risk.

How Can We Assess Value During This Crisis?

As noted above, the sell-off at the onset of the COVID-19 crisis gave way to a rally. But credit spreads have not returned to pre-crisis levels. Investors face the challenge of determining whether today's prices are a sign of elevated liquidity and risk premia, a prelude to a vastly altered economic landscape or some combination thereof. A key question for investors is distinguishing how much elevated risk aversion and expected future defaults may be contributing to the current level of spreads.

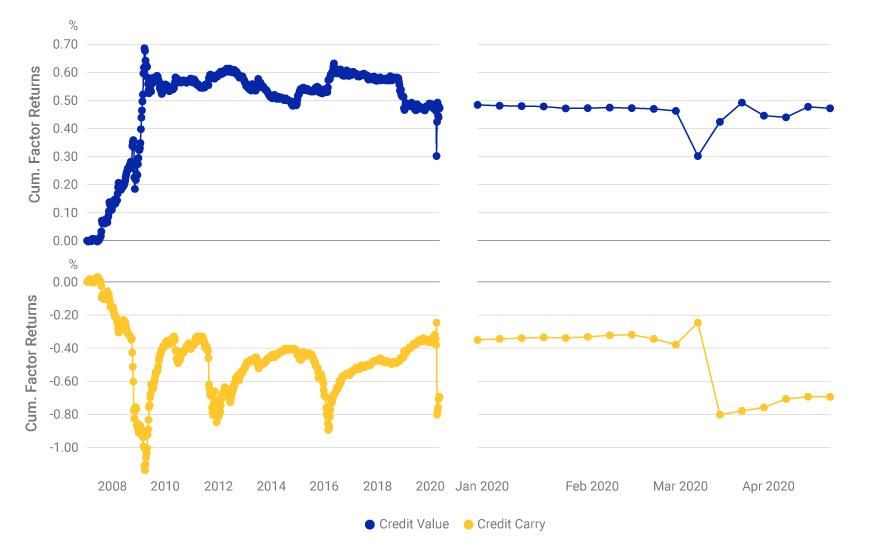

The cumulative factor returns in the exhibit below represent the spread return (excluding interest accruals) for two different investment styles since 2008.9 "Credit value" tilts toward market segments in which, on average, issuers' option-adjusted spreads (OAS) are high compared to an equity-based distance-to-default measure — and tilts away from the converse. "Credit carry" tilts toward high-OAS sectors within the investment-grade universe and away from the low-OAS sectors. It does the same in high-yield bonds. The former is a factor that generally has profited from the mean reversion of asymmetric riskiness across sectors, while the latter's returns have generally tracked the credit cycle — i.e., the broad patterns of credit-spread widening and tightening that track sectoral or marketwide episodes of distress.

Historical Spread Returns by Systematic Strategy Factor

Note that the figure understates the historical profitability of these strategies, as the cumulative factor returns don't incorporate income returns. Source: MSCI Tier 3 Multi-Asset Class Factor Model

Most of the sectoral dislocations in the credit value factor have been erased in the recent spread tightening. This is in contrast to the global financial crisis, as this tightening happened in a matter of weeks rather than months. Perhaps counterintuitively, given the recent bankruptcy filing by J.Crew,10 credit value has positive tilts toward all developed-market consumer-discretionary sectors. More broadly, the recent rally has brought sector spreads back in line with fundamentals-based measures of default risk. However, a similar rebound in credit carry has not materialized, as high-spread sectors haven't appreciated relative to low-spread sectors.

If the sector rotations are complete, as credit value's rally suggests, then what remains is determining where we are in the credit cycle. If we've reached the nadir of the crisis, then relatively high-OAS sectors may mean-revert and appreciate more rapidly than their more expensive counterparts.

Did Contagion Risk Spread to Credit Markets?

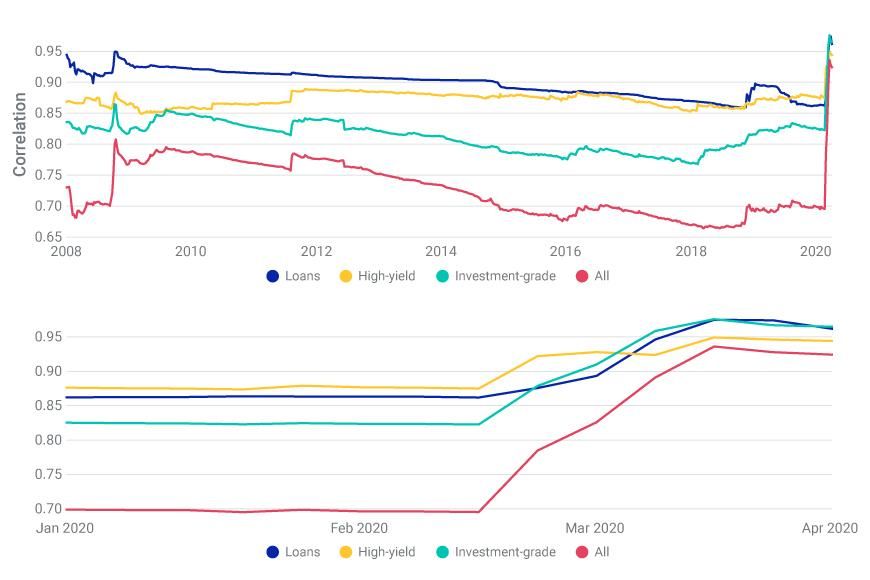

Correlation is not causation, though it may be our best measure of contagion risk, or the risk that shocks in one portion of the credit markets can be transmitted to others and thereby generate correlated defaults. Extreme correlations may signal that markets are primed for asset-class or sectoral contagion.

The MSCI Multi-Asset Class (MAC) Factor Model illustrates that credit correlation rose to elevated levels in the months since the initial outbreak. Below we plot the weekly history of the average correlation among spread factors in a given credit market (investment grade, high yield and leveraged loans). These factors capture the common element of spread return among bond issuers in the same sector or sub-sector.11 Sectors and credit tiers moved in lockstep after the onset of the COVID-19 crisis, and sector correlations reached their highest levels of the past 12 years, according to the MAC model. In other words, shocks in previously less correlated sectors (e.g., technology and energy) may now be more likely to spill over from one to the other.

Correlations Rose in the Fixed-Income Factor Model

Source: MSCI Multi-Asset Class Factor Model

Corporate-credit securitizations also showed rising correlations over the past several months. The figure below plots implied correlations12 for issuers in the North American investment-grade and high-yield CDS indexes from prices of the equity tranche of synthetic collateralized debt obligations (SCDOs).13 The picture tracks what we see above through the factor lens, implying the potential for contagion in the credit markets.

Implied Issuer Correlations Rose Simultaneously with the Factors

Source: IHS Markit

What are some of the potential impacts of elevated correlations on the financial system? We've recently documented how elevated correlations in the leveraged-loan market may lead to losses on collateralized loan obligations. Further, higher correlation among issuers may increase risk in cash credit portfolios due to weaker diversification. In addition, the risks to central counterparties — a topic of recent concern for the industry14 — might also increase as the prospect of correlated defaults may pose a larger threat to margin reserves than idiosyncratic defaults.

Conclusion

The market rally since late March has inspired commentary comparing it with the rallies of late 2008 and early 2009.15 The first was ephemeral and the second a genuine inflection point in the credit cycle. Amid the backdrop of a global pandemic and unprecedented monetary and fiscal policies, investors trying to find credit-cycle coordinates may have their work cut out for them.

The authors thank Gabor Almasi, Manuel Rueda, Benedek Skublics and Chenlu Zhou for their contributions to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The iBoxx $ Liquid High Yield Index dropped 21.7% from March 6 to March 23, bouncing back to -10.5% on April 27. The iBoxx $ Liquid Investment Grade Index fell by 18.9% from Feb 20 to March 20 and ended at -4.04% on April 27.2“Federal Reserve announces extensive new measures to support the economy.” Federal Reserve, March 23, 2020.3The basket contained representative bonds from CDX North American High Yield and CDX North American Investment Grade Index constituents for which we have issuer-level discount curves, equity-level information and debt-to-share data — leaving us with 100 investment-grade and 61 high-yield issuers. Clients of MSCI's RiskMetrics® RiskManager® can access security-level information at https://ssa.msci.com/.4CreditGrades is a structural (Merton-type) model that uses equity and balance-sheet information to derive default probabilities for a given issuer. Structural models view equity as a call option on the assets of the firm; declining equity prices prompt worsening of credit.5I.e., bond prices fell and default-protection prices increased.6There was a record (USD 35.6 billion) outflow from investment-grade funds during the week of March 18. In the same week, high-yield funds lost only USD 2.9 billion, though that outflow followed three weeks with unusually large withdrawals. Scaggs, A. “Investors Are Fleeing Corporate- and Municipal-Bond Funds in Record Numbers.” , March 19, 2020.7“MSCI Liquidity Risk Monitor Special Report.” April 28, 2020.8“Investors Are Fleeing Corporate- and Municipal-Bond Funds in Record Numbers.” .9For details on the methodology, see the section and appendix on systematic strategy factors in our insight on the MAC model: Shepard, P., DeMond, A., Xiao, L., Zhou, C., and Ahlport, J. 2020. “The MSCI Multi-Asset Class Factor Model.” MSCI Model Insight.10Biswas, S. and Mou, M. “J.Crew Tumbles Into Bankruptcy in the Wake of Coronavirus.” , May 4, 2020.11Shepard, P. and Zhou, C. 2017. “The MSCI Fixed Income Factor Model.”12These implied correlations (across issuers and thereby sectors) for CDS indexes are computed using a Gaussian copula model calibrated to prices of the equity tranche of synthetic CDOs.13Equity tranches are first in line for bearing loss in the event of collateral defaults, and their payoff structure compensates for correlated rather than idiosyncratic defaults.14Berardi, P., et al. “A Path Forward for CCP Resilience, Recovery, and Resolution.” March 10, 2020.15Mackintosh, J. “Stock Market Surge Isn’t as Crazy as It Seems.” , April 30, 2020.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.