Did hedging tail risk pay off?

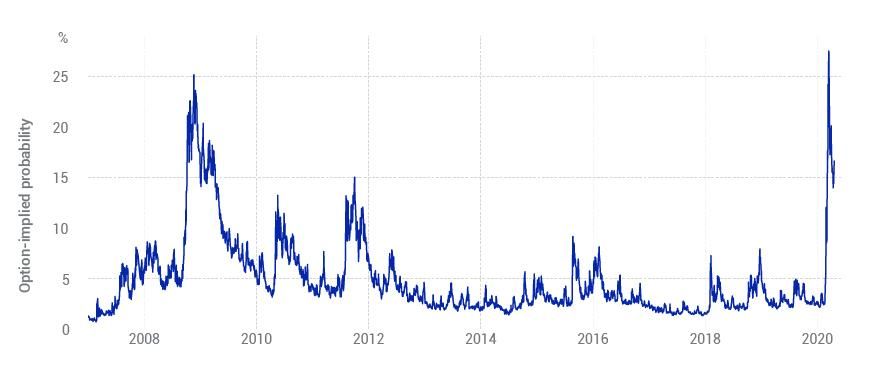

- Recent events have reminded market participants of the risk of large market drawdowns, with some investors considering strategies for hedging tail risk to protect against further losses.

- The prices of put options imply a one-in-six chance of a further 20% decline in the U.S. equity market over the next three months — roughly five times higher than at the beginning of 2020.

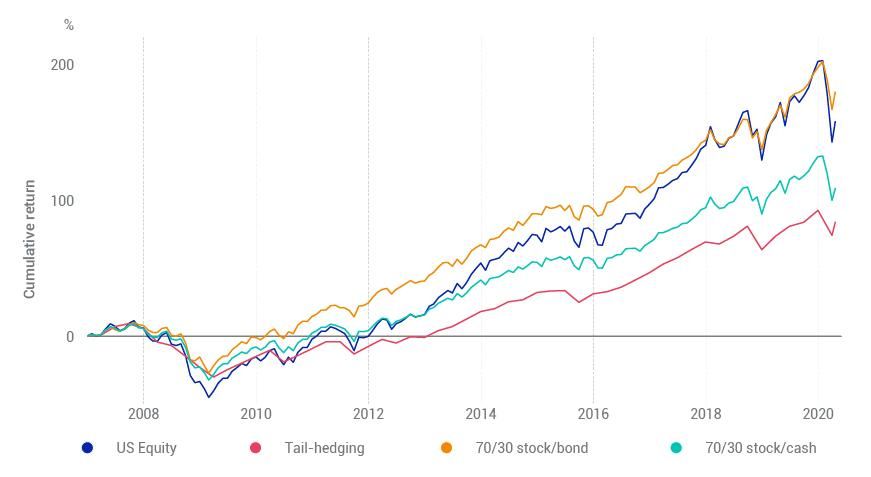

- The cost of implementing a tail-hedging strategy is correspondingly high. Unless very well-timed before crises, our hypothetical tail-hedging strategies have lagged simulated portfolios that simply reduced exposure to risky assets.

Strategy | Average Return | Maximum Drawdown | YTD Return | Sharpe Ratio |

|---|---|---|---|---|

Strategy MSCI USA Index | Average Return 8.3% | Maximum Drawdown 50.6% | YTD Return -14.7% | Sharpe Ratio 0.48 |

Strategy 70/30 equity/bond | Average Return 8.2% | Maximum Drawdown 33.9% | YTD Return -6.2% | Sharpe Ratio 0.72 |

Strategy 70/30 equity/cash | Average Return 6.1% | Maximum Drawdown 38.0% | YTD Return -10.2% | Sharpe Ratio 0.48 |

Strategy Equity + Collar (10% downside) | Average Return 5.1% | Maximum Drawdown 36.0% | YTD Return -4.6% | Sharpe Ratio 0.4 |

Strategy Equity + Collar (15% downside) | Average Return 5.9% | Maximum Drawdown 40.6% | YTD Return -9.5% | Sharpe Ratio 0.37 |

Strategy Equity + Collar (20% downside) | Average Return 6.9% | Maximum Drawdown 44.1% | YTD Return -14.8% | Sharpe Ratio 0.39 |

Strategy Equity + Puts (10% downside) | Average Return 5.4% | Maximum Drawdown 43.4% | YTD Return -9.3% | Sharpe Ratio 0.34 |

Strategy Equity + Puts (15% downside) | Average Return 5.8% | Maximum Drawdown 45.1% | YTD Return -13.0% | Sharpe Ratio 0.33 |

Strategy Equity + Puts (20% downside) | Average Return 6.3% | Maximum Drawdown 46.7% | YTD Return -17.2% | Sharpe Ratio 0.34 |

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.