Did private capital deliver?

Blog post

January 30, 2020

- Pursuing high returns and diversification, investors made record inflows into the private markets in recent years.

- From January 2013 through December 2018, average risk-adjusted excess returns were positive for most private-capital strategies. Strategies focused on Europe and Asia generally performed the best.

- Our analysis suggests that private capital provided diversification benefits relative to public markets.

Dissecting private-capital return premia

Investors may be attracted to private capital for various reasons. Many believe it delivers a return premium over traditional asset classes. This premium may be compensation for illiquidity. It may also be a result of superior skill in selecting and overseeing private companies. In addition, it may be caused by differences in companies' profiles, such as size and age. The magnitude of the return premium has varied over time, often influenced by changes in the supply and demand of private-market investment opportunities and the private-market cycle.4 We decomposed private-capital returns into two components: one arising from sensitivities to public-market factors (e.g., market, sector and size) and a pure component capturing the return premium from private markets.

The interactive exhibit below shows the pure private return premia, net of fees, for different private-capital strategies from Jan. 1, 2013, to Dec. 31, 2018, compared with the previous 26 years (Jan. 1, 1987, to Dec. 31, 2012). Click on a bar to see how a given strategy performed over time (select multiple strategies by holding the "Alt" key when you click).

Private-capital risk-adjusted excess returns (net of fees)

Loading chart...

Please wait.

Historically, many private-capital strategies generated very strong return premia (adjusted for sensitivity to public-market returns).5 Compared to the earlier 26-year period, the average premium for private-capital strategies declined from January 2013 to December 2018. Of the 17 strategies we examined, the average premium was positive for 10.6 A majority of these outperforming strategies targeted European and Asian markets, with return premia ranging from 2% to 9% over the six-year study period. However, five U.S.-focused strategies, which accounted for three-fifths of assets under management, underperformed their respective public-market counterparts. To identify when private-capital returns changed to negative relative returns, we checked the average six-year premium for each year from 2009 to 2018. We found that return premia declined for buyouts and were stable for venture capital over 2009-2018. The premia for distressed debt increased from 2013 to 2018.

Private capital's diversification benefits

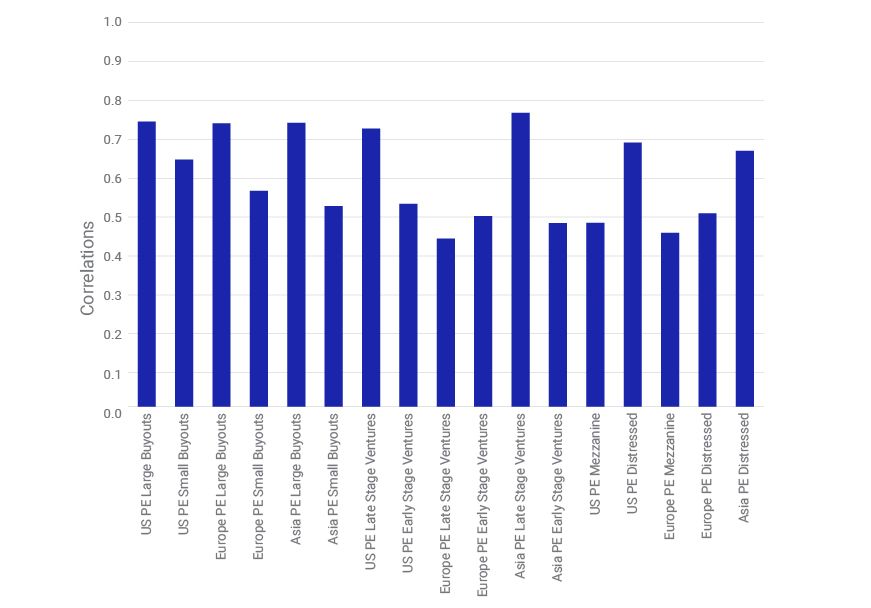

The exhibit below shows the long-run correlation of each of the 17 private-capital strategies with their corresponding public-market counterpart, based on the MSCI Private Equity Model. Unlike other methodologies that use raw returns, our model de-smooths returns, resulting in higher correlations between private and public markets.

Private capital's average correlations with public-market indexes over 2013-2018

We find that all 17 strategies still had significantly lower correlations to equivalent public-market groups. Nine had correlations below 60% and all 17 correlations were below 75%. All these correlations were substantially lower than those for the same asset class (e.g., correlations among long-only country, sector and factor portfolios in public equities). Regardless of private capital's return premia, the diversification benefits remained intact.

Understanding private capital

Private capital represents a diverse set of strategies. While return premia have varied over time, private capital continued to provide diversification benefits in our study period, supporting many asset owners' desire for uncorrelated returns. Given these variations in return premia and correlations, institutional investors may want to model these strategies to better understand their role in multi-asset-class portfolios.

The authors thank Juan Sampieri for his contribution to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1We define 17 different private-capital strategies, ranging from buyouts to distressed debt to venture capital.2“Global Private Equity Report 2019.” Bain & Co., Feb. 25, 2019.3Private-market data is available after a considerable reporting lag; data used in our analysis was through Dec. 31, 2018.4Shepard, P. and Liu, Y. 2014. “The Barra Private Equity Model (PEQ2) Research Notes.” MSCI Model Insight. (Client access only)5The public proxies aim to match region, sector and size in decreasing order of importance.6The exceptions were U.S. large and small buyouts, U.S. and Europe early-stage ventures, U.S. late-stage ventures and U.S. and Asia distressed debt.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.