Digging deeper into pan-European property funds’ performance

Blog post

November 26, 2019

- In recent years, investors have increased exposure to international property, and pan-regional investment vehicles have grown in popularity — particularly in Europe. Despite these funds' similar aims, they can vary significantly in the exposures they seek to achieve them.

- While attributes like leverage, fees and currency exposure have played an important role in determining returns, underlying asset-level performance has historically been the main driver of pan-European funds' risk and return.

- Comparing a fund's return versus a specific peer-group benchmark can provide a useful like-for-like view of relative performance, but adding asset-level return attribution can offer investors a more detailed understanding.

The growth of pan-regional property funds

Many institutional investors' real estate portfolios have historically had significant home bias, and many pooled property funds have had nationally focused mandates and strategies. Over recent years, however, this home bias has eroded, as many real estate investors have moved beyond their domestic borders in search of broad, geographic diversification. Asset managers have met this demand by developing pan-regional property funds.

In North America, there is large overlap between property funds' national and regional exposure, due to the dominance of the U.S. economy and its real estate markets. The U.S. market for core, open-end funds has been in existence for decades. Although such funds have tended to focus on providing diversified U.S. exposure, the large number and variety of major cities have provided a wide range of strategic options for managers of these vehicles — and hence a reasonable level of diversity in these funds' exposures, on an historical basis.

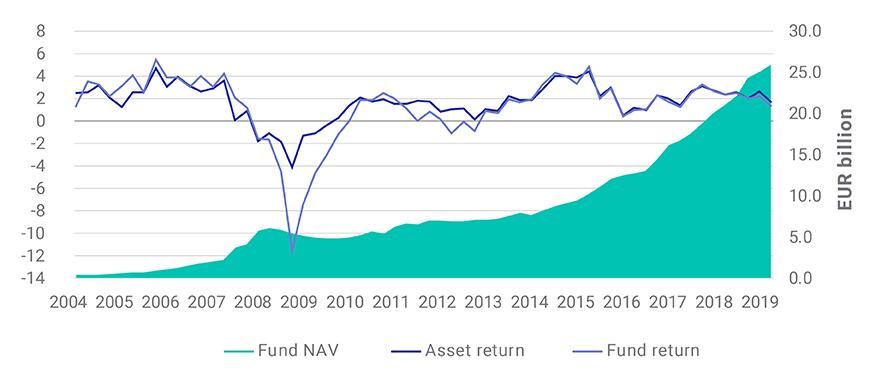

Property funds that diversify across borders have become a significant part of the European market in recent years, as the growth in these funds' net asset value (NAV) illustrated below shows. Much of Europe has diversity in real estate markets that mirrors that of the U.S. But the European market often comes with the added complexities of varying legal and tax regimes, currencies and property-market norms, such as lease structures that can lead to different property-market performance dynamics. Even with this added complexity, individual assets have tended to be the main drivers of performance, as demonstrated by comparing asset- and fund-level returns of the MSCI Pan-European Property Fund Index (PEPFI).

15 years of NAV growth in the MSCI Pan-European Property Fund Index

Mandates in detail

Many pan-European real estate funds share the same broad investment objectives (e.g., open-end, diversified European property exposure). But the nuances of the specific mandates or stated strategies can vary, leading to important differences in exposures and hence performance. For instance, does the fund invest across the whole of Europe or only continental Europe (excluding the U.K.)? Does it avoid currency risk by investing only in euro-denominated markets? Such differences are usually agreed upfront between managers and may have partially determined historical performances.

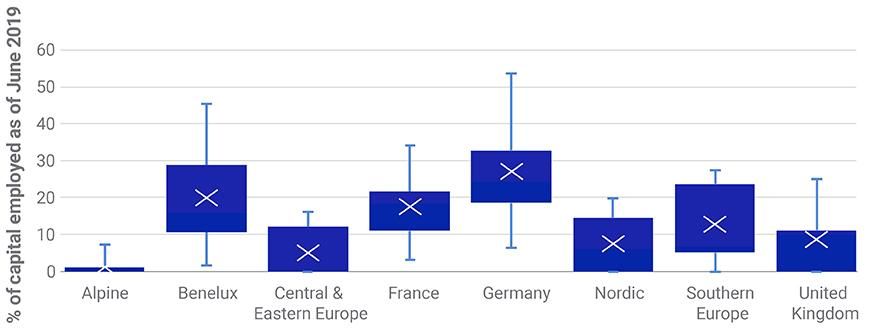

Even when comparing funds with highly similar mandates, the strategies employed by managers, the point-in-time exposures and execution have varied. This has been especially true for funds in their early-growth stages. These funds may have relatively few assets and fairly concentrated exposures to markets and sectors. The chart below, for example, compares the average regional exposures across PEPFI's component funds, while also illustrating the wide range of regional exposures across funds. All funds provided open-end, geographically diversified European property exposure, but evidently employed different strategies to achieve it.

Pan-European funds vary in their geographical exposures

Rigorous and focused inclusion criteria for benchmarks (like PEPFI) have been designed to maintain the relevance of a peer group with similar strategic aims. Combining the rigor and focus of the peer group with detailed asset-level attribution analysis may provide asset managers and their asset-owner clients with a more finely detailed assessment of their portfolios' relative performance.

Asset-level drivers of performance

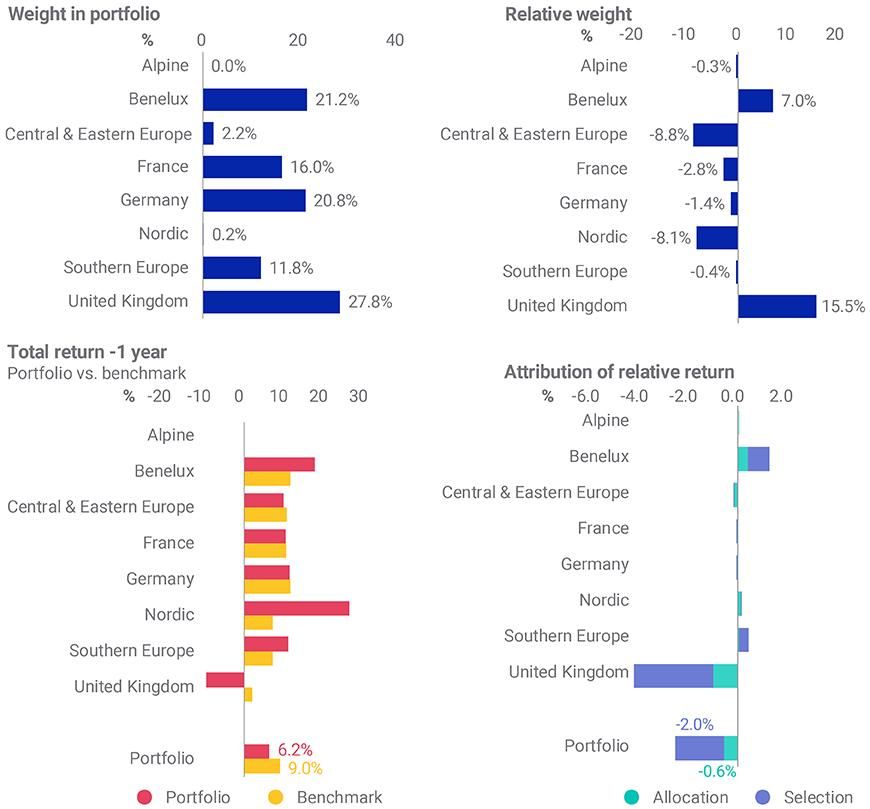

In the chart below, we show an aspect of asset-level attribution analysis for a hypothetical PEPFI portfolio: We constructed this simulated portfolio by randomly sampling assets from PEPFI contributors' funds, subject to the inclusion criteria of the index, and closely aligning the size of the simulated portfolio to the peer group's average.

Underperformance was driven by weak assets in a weak market

The specifics of the underperformance

The simulated portfolio's assets underperformed those of PEPFI by 280 basis points in the 12 months up to September 2019.1 But why? The portfolio's largest regional exposures were in the Benelux countries, Germany and the U.K. In each of these regions, it held more than the average PEPFI fund. The yellow bars show the peer group's average performance in each region. Comparing them across the third panel highlights the U.K. market's poor performance versus the other regions, while the converse was true for Benelux. The large market exposure to the underperforming U.K. dragged down relative performance, as shown by the turquoise allocation bars in the final panel. The more significant drag to performance, however, was the relatively poor performance of the portfolio's U.K. assets relative to those the peer group held in the U.K., as indicated by the pale-blue bars. The underperformance was partly due to the overweight allocation to the U.K. — but more significantly due to the performance of those U.K. assets versus the rest of the peer group's U.K. assets.

Rigorous and focused inclusion rules are important to maintain the relevance of the peer group, so the headline performance comparison is meaningful. This is particularly relevant for pan-regional investing across Europe, where the peer group is a relatively small part of the broader investment landscape. The application of detailed asset-level attribution analysis provides important insight into the drivers of performance relative to the benchmark.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1We considered asset-level performance only and excluded fund-level impacts such as leverage and fees.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.