Dissecting the Stock Market Sell-Off

Blog post

February 6, 2018

Feb 6, 2018

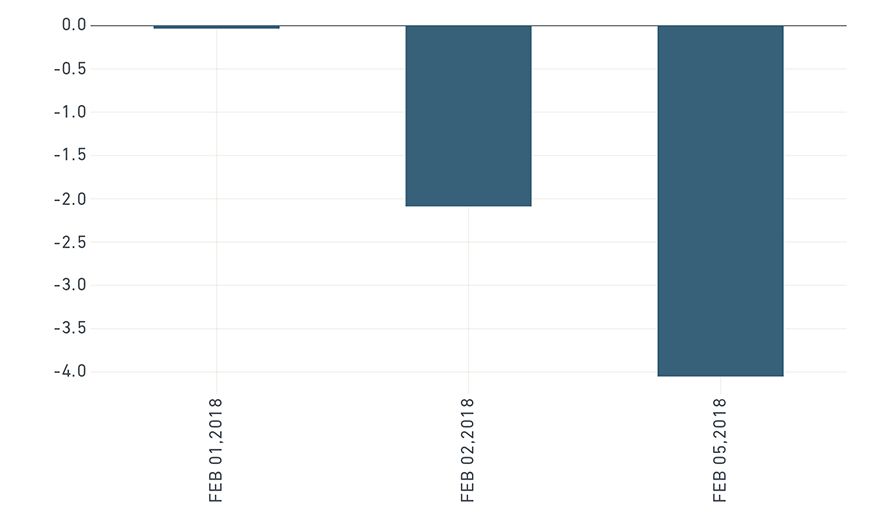

Growing fears about rising inflation and interest rates sparked a decline across equity markets in the last few days. The MSCI USA Index fell 2% on Friday and a further 4% on Monday. Has the sell-off been indiscriminate? Or has it affected certain sectors and factors more than others? In this blog post, we dissect the recent decline and compare it with previous extreme market conditions.

Growing fears about rising inflation and interest rates sparked a decline across equity markets in the last few days. The MSCI USA Index fell 2% on Friday and a further 4% on Monday. Has the sell-off been indiscriminate? Or has it affected certain sectors and factors more than others? In this blog post, we dissect the recent decline and compare it with previous extreme market conditions.

MSCI USA Index returns over the past 3 days

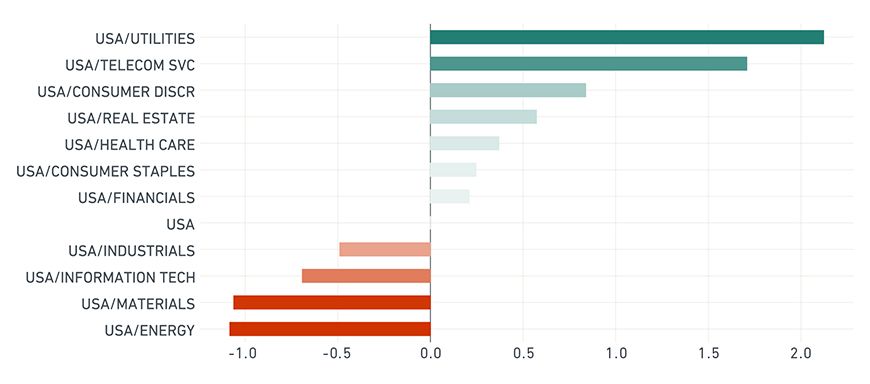

The sell-off was not indiscriminate. Although all sectors registered negative absolute performance, we saw clear evidence of flight to safety. Using sector indexes as market proxies, we see that defensive sectors such as utilities and telecom outperformed while cyclical sectors such as energy, materials and information technology fell more than the market.

Utilities and telecom outperform while other sectors are hard hit

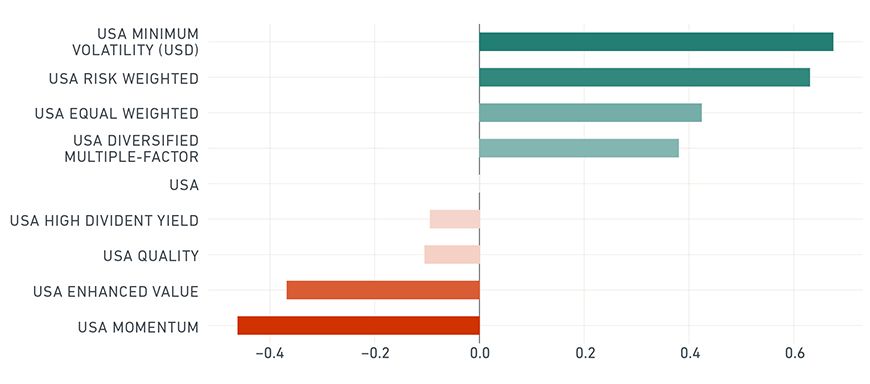

We observed similar patterns of performance across equity factor indexes. Low volatility indexes outperformed while value and momentum indexes fell sharply and underperformed the broad equity market. One unusual feature of this sell-off is that large-cap stocks dropped more sharply than mid- and small-cap companies, resulting in outperformance for the MSCI USA Equal Weighted Index. The MSCI USA Diversified Multiple Factor Index, a proxy for fundamental strategies that favor stocks with low size, value and quality characteristics, fared relatively well during the sell-off.

Minimum volatility outperformed while value and momentum declined

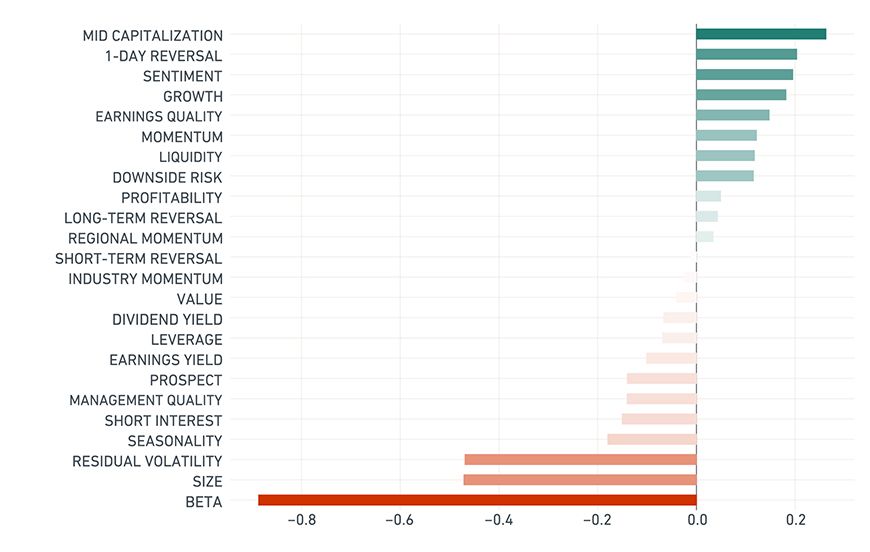

Next we turn to factor returns from the MSCI Barra U.S. Total Market Equity Trading Model (USFAST). In the three days leading up to Feb. 5, 2018, the beta, residual volatility and size factors had sharp negative excess returns while the mid cap factor showed modest improvement in this period. All other factor returns were relatively muted during this time.

Factor performance during the recent market turbulence

Source: USFAST equity model

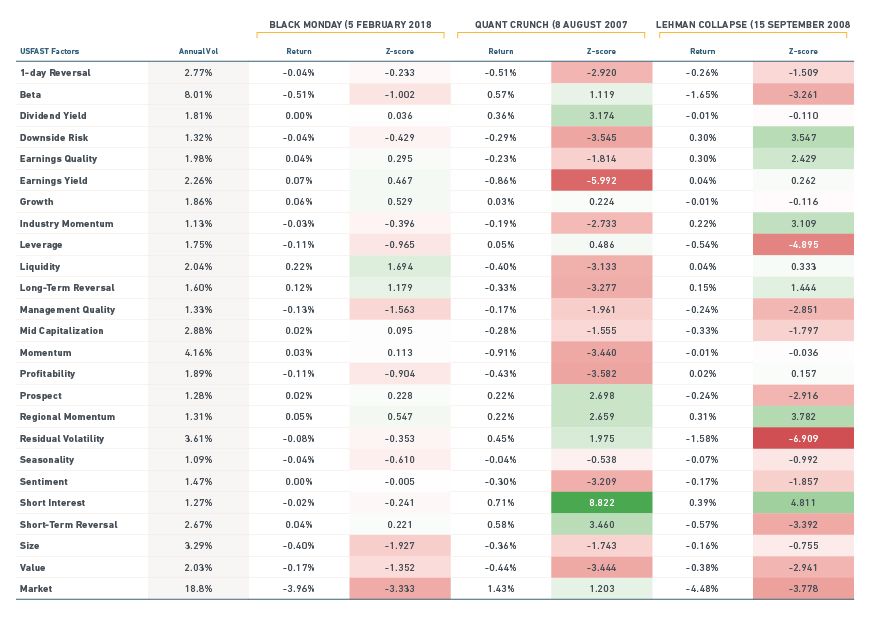

To put factor performance in a historical context, we focus on one-day returns and calculate z-scores by dividing with daily factor return volatility, calculated over the period June 30, 1995 to Feb. 5, 2018, the longest period for which we have daily factor return data. Then we compare standardized daily factor returns from Feb. 5, 2018 (Black Monday) against two previous instances of extreme market conditions: the Quant Crunch on Aug. 8, 2007 and the collapse of Lehman Brothers on Sept. 15, 2008.

Comparing extreme market events

Source: USFAST equity model

On Black Monday, the U.S. market factor (bottom line) was the only factor that experienced an extreme drawdown of more than three standard deviations while all style factors were within two standard deviations. The worst-hit style factors were size, value, beta and management quality, with drawdowns between one and two standard deviations. The short interest factor had muted negative return that day, suggesting that covering of short positions did not play an important role.

Factor returns during the Quant Crunch reveal a different profile. The market factor was actually up by just over one standard deviation that day. On the other hand, traditional risk premia factors favored by quantitative strategies suffered sharp drawdowns as leveraged equity hedge funds aggressively unwound positions in stocks with high exposure to these factors. In particular, value, earnings yield, momentum and profitability were all down by more than three standard deviations. The short interest factor had a nine (!) standard deviation positive move that day, as a result of aggressive unwinding of short positions and short covering by leveraged quantitative equity funds.

When Lehman Brothers declared bankruptcy on Sept. 15, 2008, the U.S. market factor had a 3.8 standard deviation drawdown, similar in magnitude to Black Monday. Beta and residual volatility factors also registered sharp negative returns that day. Also, the leverage factor fell by five standard deviations, underscoring the severe impact of the credit crunch on highly leveraged companies.

On Feb. 5, 2018 the U.S. market experienced its 12th worst drawdown over the last nine years. The relative performance of sectors and factors in the U.S. equity market suggests that investors preferred safer assets. However, style factor returns were within two standard deviations and factor performance was much less volatile than in previous recent extreme markets conditions. Thus, while Black Monday was a significant event, we have seen much more severe drawdowns and intra-market rotation in the past decade.

The author thanks Roman Kouzmenko for his contributions to this blog post.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.