Drawing Insights from Thematic Exposures: The (Natural) Language of Growth Investing

- While artificial intelligence has generated interest recently, bespoke language models have already gained traction in characterizing firms by connecting them to longer-term, structural themes.

- Growth-oriented firms that also had exposure to themes were in the minority, but drove much of the return in the MSCI ACWI IMI Growth Index over the past several years.

- Indexed and discretionary fund managers may complement language models with traditional tools such as factor attribution to manage a portfolio's risk and performance.

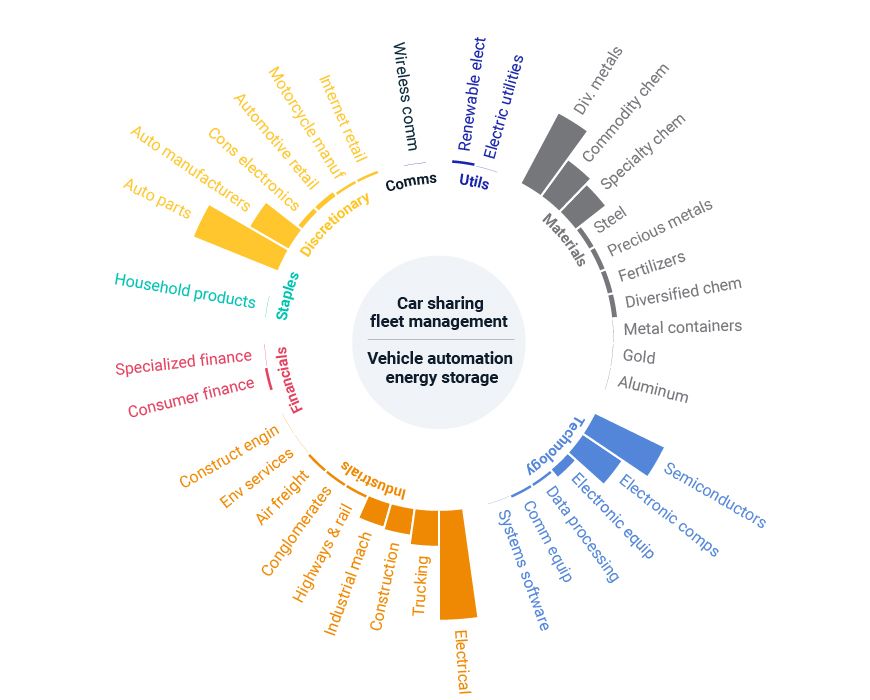

One theme but many industries

One of the challenges inherent in thematic investing is identifying the firms that have economic linkages to broader themes. That is important because themes can span many products and services, and no single sector or investing style may capture its full value chain. We found that NLP can assist by generating granular phrases that describe the theme, which can then be compared to companies' self-declared business-line information and publicly-sourced business description information.

For example, a mobility-related theme (shown below using the constituents of the MSCI ACWI IMI Future Mobility Index) seeks out firms associated with the development of energy storage, fleet management and vehicle grids, amongst other concepts. The list of concepts that describe the theme are linked to several-hundred firms, which themselves span eight GICS® sectors1 and almost 40 sub-industries, from diversified metals to data processing.

Mobility themes span eight sectors and 40 sub-industries

The bars represent the number of stocks in each sub-industry in the MSCI ACWI IMI Future Mobility Index. As of Dec. 31, 2022.

The weight of words

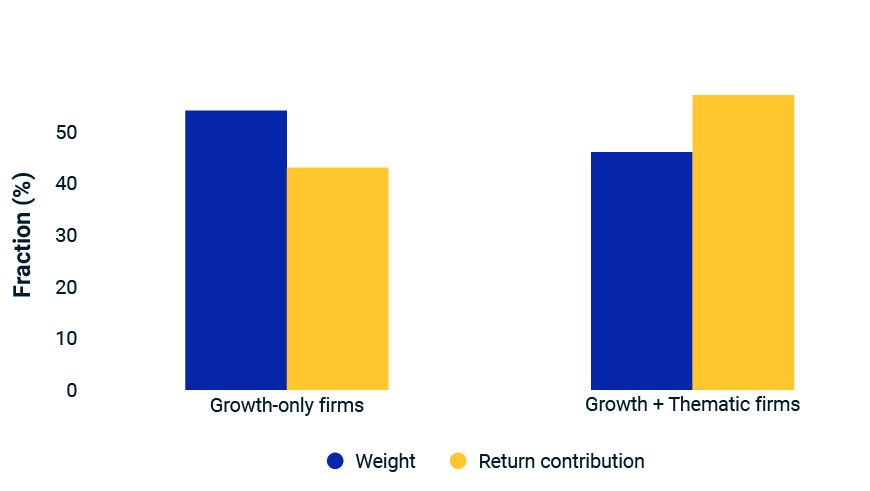

Given that NLP can assist in linking firms to themes, we then set out to test if themes can provide insight into the success of the growth stocks over the past decade. Specifically, we wanted to know what type of growth-oriented firms drove the style's success.

At first glance, growth and thematic stocks might appear very similar to one another. However, as we previously highlighted, the two can have notable distinctions between each another. We extend that analysis (shown below) by comparing growth-only firms (those with a history of growing earnings but little exposure to longer-term megatrends) to growth firms that also had a significant thematic exposure.2

Growth and thematic firms made up less than 50% of the MSCI ACWI IMI Growth Index

Weights are the average and return is the contribution from each category from Jan. 2017 to Dec. 2022, which is the maximum period for the simulated Leaders approach.

On a historical basis, we found that the growth-only firms accounted for about 60% of the weight in the MSCI ACWI IMI Growth Index, but only 40% of the index's total return. The 'growth and thematic' firms, however, carried more than their weight, as they accounted for 40% and 60% of the weight and return, respectively. In other words, investors significantly rewarded those firms that were not only able to steadily grow their top and bottom lines, but also take advantage of transformative trends (as shown below). That held true despite the sharp sell-off in growth stocks in 2022.

Growth and thematic firms outperformed growth-only firms

Returns are gross in USD. From Jan. 2017 to Dec. 2022.

The drivers of outperformance

Next, we examined what the drivers of outperformance were in the Growth and Thematic group of firms. To help isolate if and how the thematic risks paid off, we combined traditional attribution with factor attribution. The overweight to high-exposure firms accounted for the bulk of the outperformance, shown in yellow below. A handful of companies in the software and services, semiconductor and the life sciences industries had an outsize effect. Whether the platform dominance3 of those firms continues will be a vital question for investors going forward.

Factor risk in high exposure firms presents an opportunity for refinement

The left plot shows fraction of active return vs. the MSCI ACWI IMI Growth Index from Jan. 2017 to Dec. 2022. The right plot shows contribution from selected factor groups within the high-exposure firms.

Factor attribution revealed an important nuance within the high-exposure firms, shown on the right above. Many of these firms were the largest and had the highest growth, which was impactful but was more than offset by the tendency of these same firms to be high beta and have low investment quality. That presents the opportunity to integrate factor risk controls into thematic portfolios, either through rules-based or discretionary means.

NLP's future in investment management is coming fast, but the future is already upon us for certain applications. Language models may help in connecting company operations to longer-term structural themes, which can influence stock selection. These models assist in calculating thematic exposures, which can help in creating distinctive portfolios, and in understanding the drivers of a portfolio's risk and return.

Further Reading

1Sectors and industries are based on the Global Industry Classification Standard (GICS®), the global industry classification standard jointly developed by MSCI and S&P Global Market Intelligence.2We use the ‘Leaders’ approach, which captures several themes (such as mobility) in a single portfolio. Stocks that exist only in the MSCI ACWI IMI Growth Index make up the ‘growth-only’ group. Stocks that exist in both the MSCI ACWI IMI Growth Index and the simulated Leaders approach make up the ‘growth and thematic’ group.3SpringerLink, “Multisided Markets and Platform Dominance,” May 17, 2020.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.