Emerging market country allocation matters

Blog post

November 6, 2019

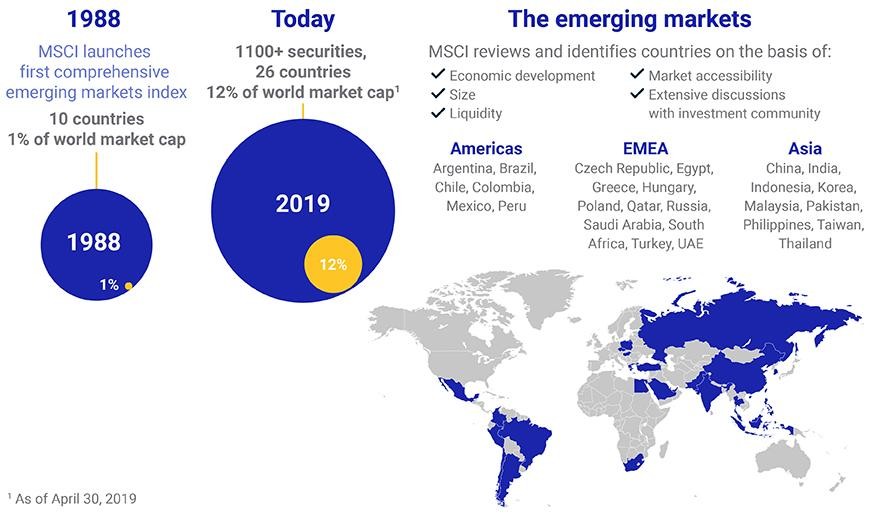

- Over the past three decades, emerging markets (EM) have grown to 12% of global equities (as reflected by the MSCI ACWI Index) from less than 1%.

- Emerging markets' headline performance can hide a wide dispersion of country outcomes. The performance of EM stocks tended to be more affected by their underlying country than by their sector or style exposure.

- Understanding how EM countries react differently to macroeconomic factors, such as the U.S.-China trade war and the price of oil, may matter for investors with strong views.

The evolution of emerging markets

How one approaches EM equities may depend on one's level of conviction and whether one employs a top-down or bottom-up approach. For example, an investor with a low level of conviction on individual countries or stocks might use an approach that aims to replicate a market-cap-based index, such as the MSCI ACWI Index and MSCI Emerging Markets Index. At the other extreme, an investor with strong bottom-up views might seek an active EM manager.

However, an investor with strong convictions might consider an approach allowing tilts toward or away from specific themes. One way to do this would be through active allocation to single-country index-based funds. We explore topics investors might consider with such an approach.

Measuring the opportunities

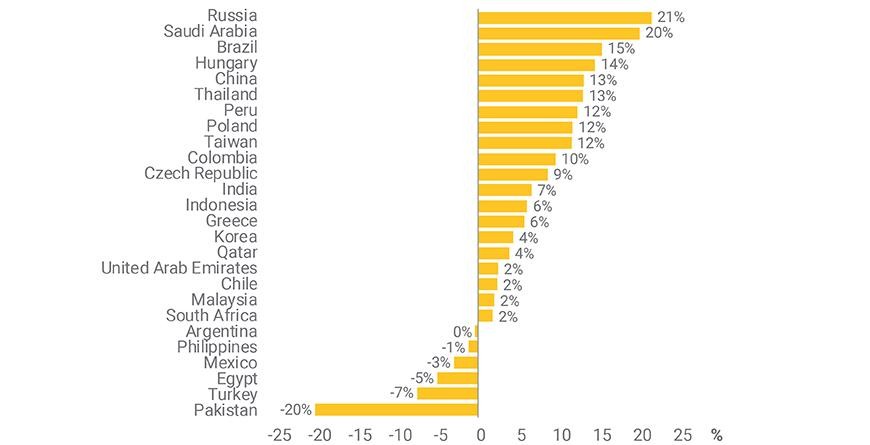

In emerging markets, the spread of returns between countries has tended to be wide, especially over short-term time horizons. For example, over the three years ended July 31, 2019, the difference in returns between the best- and worst-performing EM country was 40% — more than twice the range in developed markets.

A wide dispersion in EM country equity performance

Three-year performance in USD, annualized through July 31, 2019.

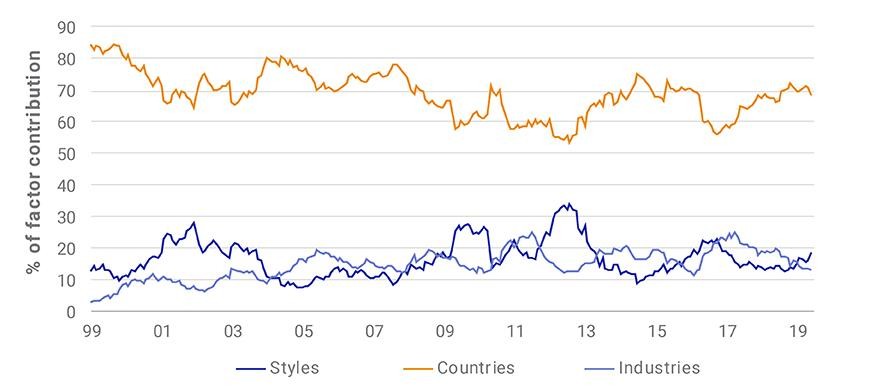

This wide dispersion in performance is supported when looking at the cross-sectional volatility (CSV)2 of the emerging-market stock universe across three systematic factor categories: countries, sectors and styles. In developed markets, the three factor categories all had similar contributions to stock-return dispersions. However, in emerging markets, the contributions to CSVs were distinguished with countries representing over 60% of the systematic factors, while both sectors and styles were below 20% for the majority of time over our sample period of 20 years. In other words, leaving aside the idiosyncratic component, the performance of EM stocks tended to be more affected by their underlying country than by their sector or style exposure.

Country factors had larger influence over EM returns

The MSCI Emerging Market Index cross-sectional volatility by factor groups from Dec. 31, 1998, to March 29, 2019.

EM countries reacted differently to macroeconomic factors

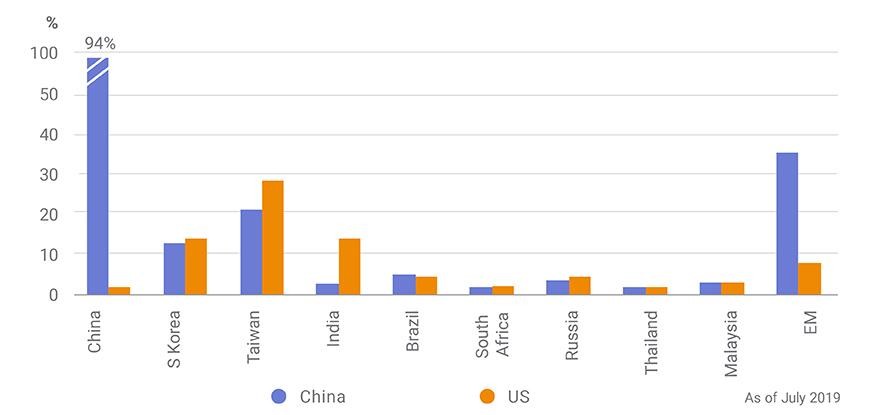

Given the large role of country exposure, we examined the potential effect of macroeconomic events, such as the current U.S.-China trade war. Specifically, we sought to understand the supply-chain impact and from where revenues were sourced by country and sectors.3

Looking at the exhibit below, we see the Chinese equity market is almost exclusively a domestically oriented one – with over 90% exposure to the internal market. Looking at the other large EM countries, South Korea and Taiwan are the two countries most exposed to both China and the U.S.

Economic exposure to China and the US

Measuring the sensitivity of EM countries to currencies

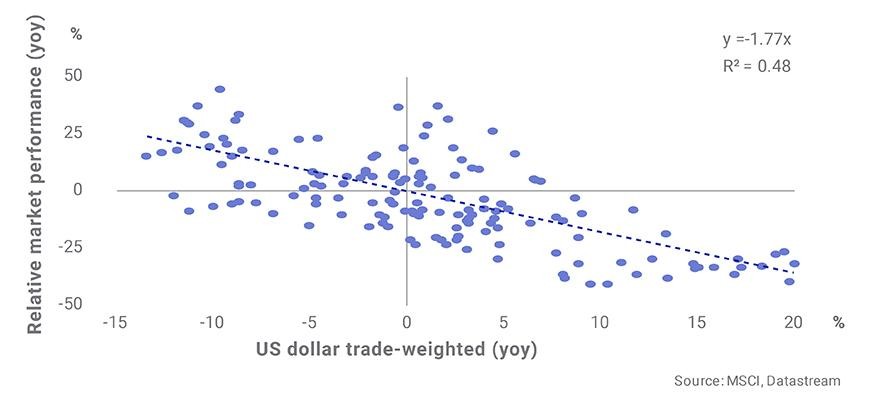

The U.S.-China trade war may also have an impact on EM currencies, whether directly if a country embarks on currency depreciation or indirectly if the trade war triggers an economic slowdown, which might change the valuation of a country's currency. In particular, the weakness or strength of the U.S. dollar historically had implications for countries such as Taiwan, Russia and Brazil.

Looking at one-year rolling periods from 2006 to 2019,4 an equal-weighted mix of the Russian and Brazilian equity markets, as represented by the MSCI Russia Index and MSCI Brazil Index, tended to underperform versus Taiwan when the trade-weighted U.S. dollar strengthened against major currencies and vice versa (see exhibit below). With an R-squared5 of 0.48, the relation was strong over those 13 years, and the coefficient of the regression suggests that for every 10% the U.S. dollar trade weighted strengthened, Taiwan outperformed a mix of the Russian and Brazilian equity markets by over 17% on average.

US dollar impacted Brazil, Russia and Taiwan stock markets differently

One-year rolling periods in USD from 2006 to 2019

The sensitivity of EM countries to oil prices

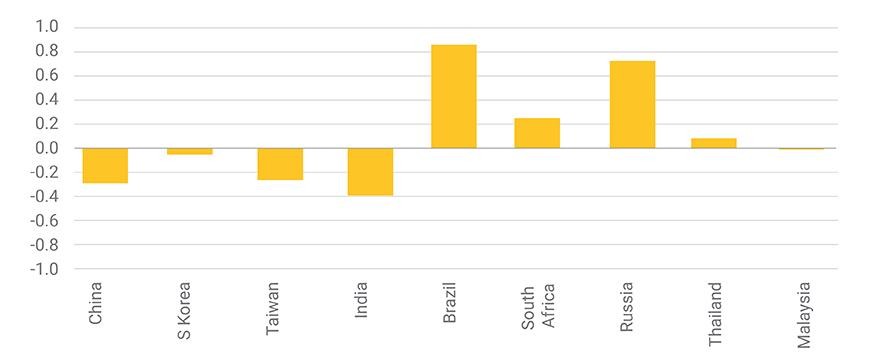

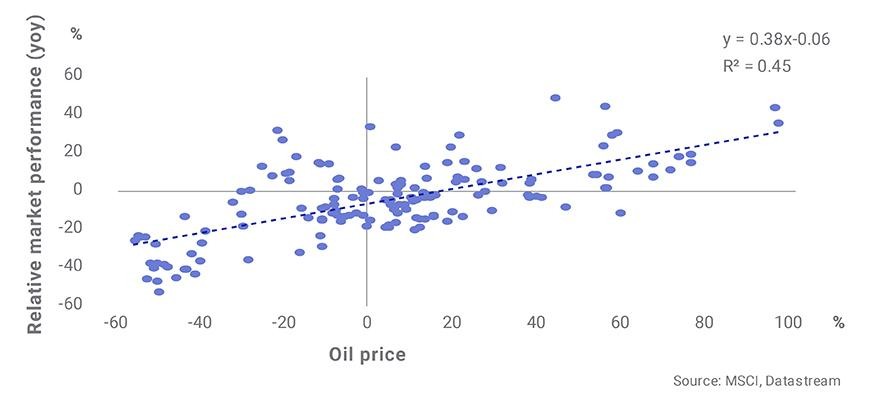

The price of oil is often another determinant macroeconomic variable, especially for large EM commodity producers. Based on MSCI's Barra Emerging Markets Model, EM countries have different exposures to oil, depending on whether they are a producer, such as Russia and Brazil, or importer, such as China, India and Taiwan. Historically, producers outperformed importers when oil prices rose (see exhibit below).

Oil price and emerging markets

Missing the trees for the forest?

In short, investors with strong convictions face a number of considerations when investing in emerging markets. Equity performance across EM countries were less correlated than DM countries. Additionally, many EM equity markets showed wide dispersions of reaction to certain macroeconomic variables such as economic exposure, currencies and commodities, which can be affected by major global events. Approaches based on single-country indexes may allow investors to express their views on specific themes.

The author thanks Fotios Kassianidis for his contribution to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1From Dec. 31, 1987, to Sept. 30, 2019.2Defined as the standard deviation of returns across stocks in a given universe.3The economic exposure of a company to a target region or country is the proportion of its revenues coming from that region. As a general principle, MSCI estimates economic exposure from the geographic segment distribution of revenues by final markets/destination as reported by a company and the GDP weight of the countries and regions within a specific geographic segment. See the MSCI economic exposure data methodology.4Time series of the US dollar trade weighted index available from Datastream.5R-squared is a statistical measure of how close the data is to the fitted regression line.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.