Factor Investing Goes Multi-Asset Class

Factor investing has brought disruptive change to the asset management industry. The effects were first felt in equities, where rules-based factor strategies ate into the domain of the stock picker, and created low-cost opportunities for the asset owner. But the disruption has not ended. Factor investing is now going multi-asset class: to factor-based asset allocation and systematic strategy factors that push beyond equity selection.

Factor-based asset allocation

One new form of factor investing is factor-based asset allocation. Rather than make allocation decisions among asset classes, many large institutions have begun to look through to the underlying drivers of returns: factors which cut across asset classes, and within them. For example, instead of allocating to fixed income as an asset class, bonds are viewed as providing different exposures to rates, credit and inflation, with very different behavior from each. Similarly, both public and private equity give exposure to a generalized equity factor. The latter is also exposed to a "pure private" illiquidity premium, but its returns often have more in common with public equity than with other alternatives such as hedge funds or real estate.

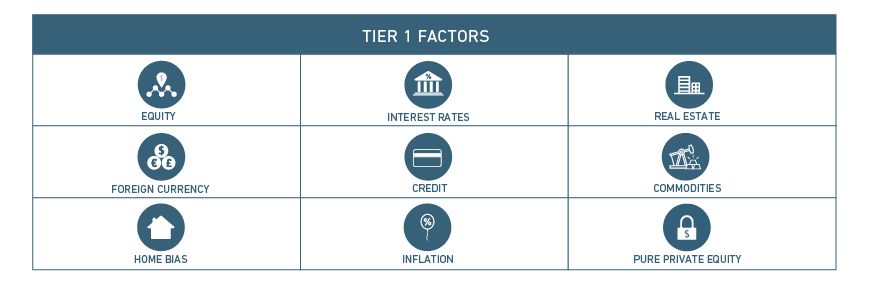

Since asset class weights can be loosely tied to the underlying exposures driving returns, factor-based asset allocation directly uses these exposures as the basis of the allocation decisions. Asset classes are relegated to the role of investment vehicles chosen to efficiently implement the desired factor exposures, much as individual stocks can be seen as conduits for equity factor exposures. At the highest level, the most important factors driving a broad, multi-asset class portfolio are the "Tier 1" factors, as described in our soon-to-be-released paper, "The MSCI Multi-Asset Class Factor Model."

Multi-asset class systematic strategies

A second form of multi-asset class factor investing is pushing systematic strategy factors beyond equity selection. Initially, factors such as value and momentum recognized that some investors' stock-picking patterns could be captured with systematic, rules-based strategies. Rather than reflecting skill – and compensated with corresponding management fees – returns to these strategies can be captured with efficient, indexed vehicles. Just as importantly, the prevalence of these strategies makes them sources of concentration, and important risk factors.

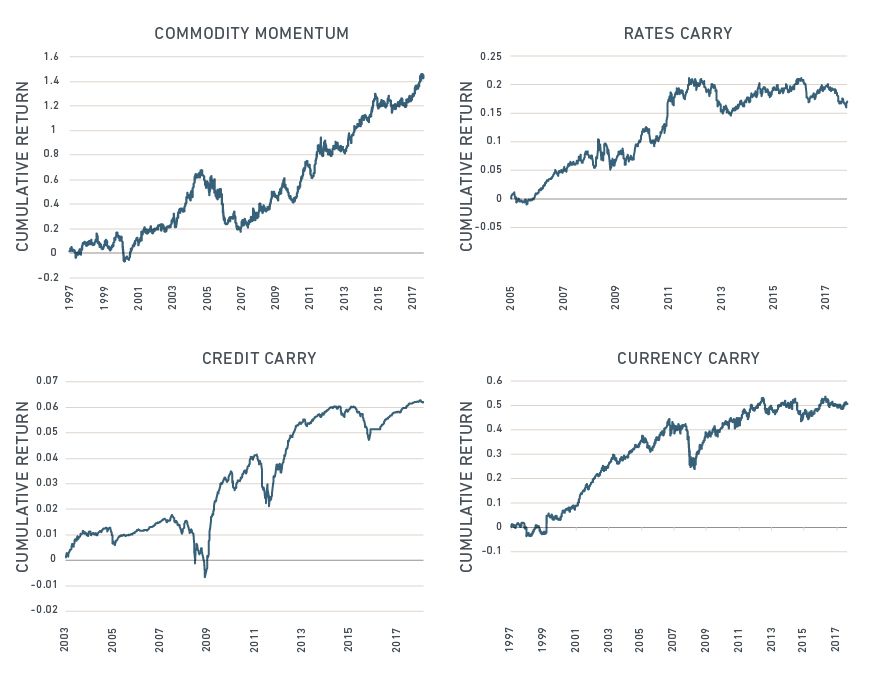

More recently, many investors have recognized the role of systematic strategies in a wide range of asset classes, and many strategies that originated in equities have counterparts in other asset classes. The mechanical definitions differ significantly across asset classes – value draws on balance sheet ratios for equities, and purchasing power parity for currencies, for example – but the economic rationale for the factors is often the same. Value strategies aim to capture mispriced assets reverting to fundamental value, and momentum reflects investors' trend-following behavior and initial under-reaction to new information. Examples of such strategies can be seen in the following exhibit.

Performance of selected systematic strategy factors

Source: The MSCI Multi-Asset Class Factor Model

No one view is correct, and different investment problems call for different lenses. In some cases, a yen exposure is best understood as part of a currency carry strategy. In other cases, yen exposure is simply that: a directional bet on the yen.

To make sense of this landscape, MSCI is introducing a suite of models for factor investing, with multiple tiers of factors to capture the global drivers of risk and return across all asset classes, and an aggregation framework to zoom in and out between views. Together, these provide a new framework to understand a multi-asset class factor world.

The move to factor investing in equities has been felt across the investment industry. Active managers, hedge funds and indexed funds have all been affected one way or another. Other asset classes are likely to follow.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.