Fed policy, the credit cycle and real estate

Blog post

May 28, 2019

Amid the uncertainty over Federal Reserve policy, investors in commercial real estate (CRE) are confronting asset-allocation challenges and growing concerns about CRE valuation and debt levels, after an extended period of easy credit.1

In the late stages of past credit cycles, lagging net operating income (NOI) took time to return to a neutral level relative to the risk-free return. If rates rose too fast or higher than the neutral level, it risked slowing down the economy, potentially impairing CRE. The Fed's current, more dovish policy and tone may give necessary breathing room for CRE — to allow NOI growth to catch up with the rate rise so far and adjust to the new credit environment. Even if commercial real estate is overvalued, slow asset deflation, capitalized over a longer period, could help for a smoother transition.

Is CRE value a concern?

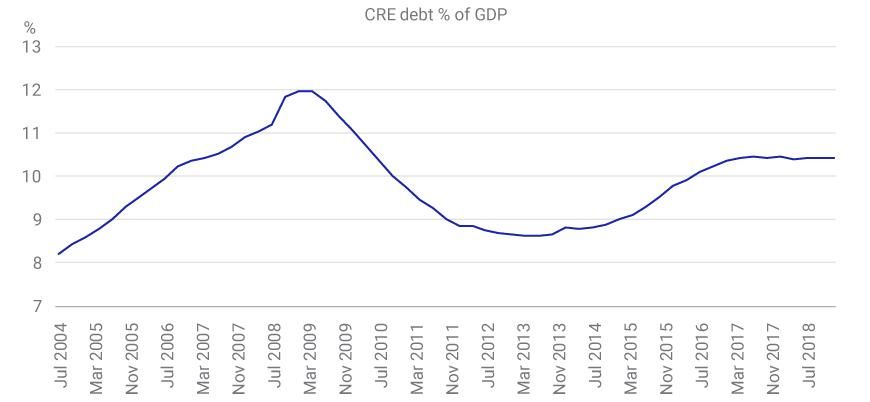

Total CRE debt issuance outpaced GDP growth over the past four years, further buoying asset prices. Concerns about asset overvaluation are compounded by fears that property income may not keep up with debt-service costs — particularly for loans on properties with long-term leases and locked-in terms. Rising CRE delinquency could also negatively impact commercial mortgage-backed securities (CMBS) backed by those loans, especially junior tranches.

Commercial real estate debt … a rising concern?

CRE debt is measured as the total value of outstanding CRE loans issued by U.S. commercial banks. Source: Federal Reserve Board

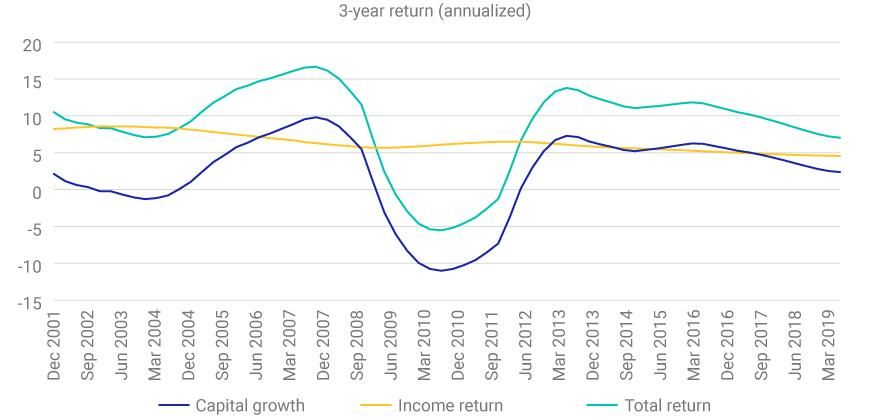

Separating the components of CRE returns

Total real estate return can be decomposed into capital growth and income. The exhibit below shows the strong cyclical pattern of total return, which was driven largely by the capital-growth component. Also, the subprime-mortgage-led credit boom and bust dominated CRE's total-return data from 2005 to 2011.

Real estate's total return has been cyclical

Source: MSCI Global Intel

Calculating the CRE risk premium

In the years since the global financial crisis, the extremely low-yield environment has forced many funds to seek alternative investments to meet their liabilities. During this period, CRE has shown extraordinary growth. If the Fed pushes bond yields higher by enacting more aggressive balance-sheet reduction/normalization and hiking the overnight rate, yield seekers might reduce their risk taking.

We decomposed the CRE NOI yield into the risk-free return (i.e., the 10-year Treasury's yield) and the spread for risk premium (including the expectation for excess NOI growth) as a risk metric. To gain a more meaningful view of these historical CRE risk premiums, we first made two adjustments that allow us to better compare the risk-free nominal Treasury yield and the rate of return of real estate investments:

- The real, not the nominal, rate: We assume a 5% cap rate (initially, USD 5 of NOI and a property price of USD 100, ignoring annual operating costs for simplicity for the denominator). If the NOI of the property keeps up with inflation (e.g., a rate of 2%), the NOI of the same property would increase to USD 5.10 the following year in our model. The property price then appreciates to $102 with the same 5% cap rate. Consequently, the property owner would have achieved a 5% real return (over inflation). Therefore, comparing the cap rate/NOI yield to the real rate — e.g., the real 10-year Treasury rate — may simplify the analysis without the inflation complication.2

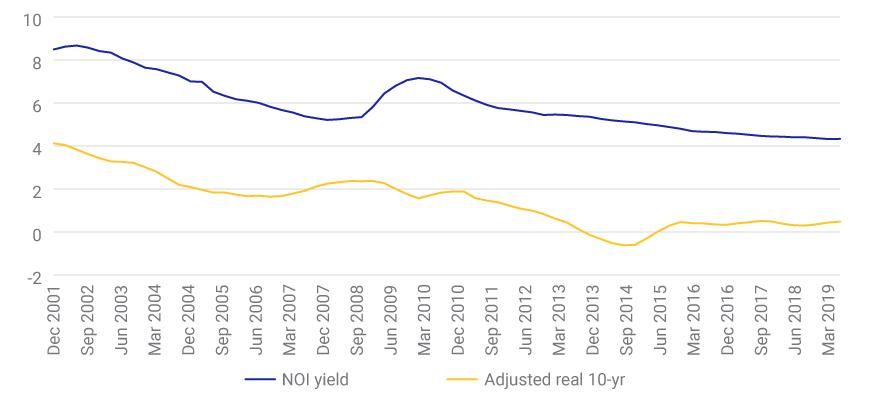

- Lagging and moving averages: Real estate income is usually fixed for the duration of a lease. As demonstrated by cross-section regression, we can adjust the lagging and moving averages (over the previous four quarters) to account for the asynchronous nature between the bond yield and the rate of return on real estate investment. NOI yield pretty closely followed the general downward trend of the adjusted real 10-year Treasury rate over the past 20 years.

NOI yield has closely followed the adjusted real rate of the 10-year Treasury

Source: MSCI Global Intel

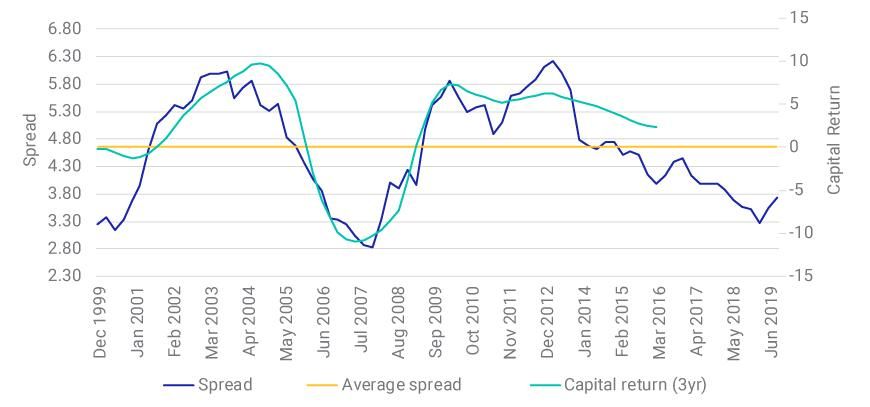

The exhibit below shows the overlay of the spread and the three-year capital return. The capital return for each calendar date represents the return for the subsequent three years. Historically, a tighter spread indicated weaker capital return for CRE — which in turn led to concerns about CRE valuation. Meanwhile, the current, more patient and dovish Fed could accommodate a smoother transition. We note that for a longer-term CRE investment horizon with less leverage, investors have historically been better able to ride through the credit cycle.

A tighter spread has led to weaker real estate capital return

Source: MSCI Global Intel

Asset allocation and cyclical uncertainty

The Fed's policy changes could have significant implications for commercial real estate. In the late stage of the current credit cycle, changes in rates and the Fed's balance sheet historically have affected valuations, and properties those with high debt-service costs. On the debt side, commercial MBS also have suffered during such periods. In a period beset with trade tensions and diverging central bank monetary-policy, risks may be around the corner.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Buhayar, N. “Bankers Are Worried About Sky-High Commercial Real Estate Prices.”Bloomberg, Oct. 11, 2018.2For instance, the NOI yield was much lower than the nominal treasury yield in 1970s and 1980s, which is not intuitive. Very recently, half of the 50-basis-point rate rally in the last two months of 2018 is actually attributed to breakeven inflation change.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.