Five Misconceptions About Climate-Change Risk in Real Estate

- Because of real estate's illiquidity, fixed locations, energy consumption and other characteristics, property portfolios may be particularly vulnerable to climate-change risks.

- Many real estate investors have been increasing their focus on climate-change risks in recent years, but some misconceptions still exist within the industry.

- From a belief that climate-change risk is too far down the road to matter, to overlooking transition risk. These misconceptions may make it harder for investors to understand the risks climate change poses to their portfolios.

1. Climate-change risk is too far down the road

The typical holding period for real estate assets can vary considerably, but is usually measured in years or decades.1 Climate-change risk models, on the other hand, often project out to the end of the century, so investors may be tempted to think that climate change will not pose a threat to assets they hold today, even though some assets are already experiencing the impacts of climate change. But even short-horizon investments can be affected by long-term risk — via an impact on exit value. For example, the impact of infrastructure development projects, like new transport links, can have an impact on asset values far in advance of the expected completion date, as investors price in the likely impact of the new infrastructure. The situation may be similar for climate-change risk, as markets may start to price in changes that won't be realized during the current hold period. The world economy may not have reached net-zero, and the full extent of physical risks may not have occurred by the time an asset is sold, but that doesn't mean that climate-change risks can be ignored in the short term.

2. Climate-change risk is only physical

Buildings are real assets, so physical hazards like hurricanes, floods and fires tend to be front of mind for many investors. Physical risks are only part of climate-change risk, however. An equally important consideration comes in the form of transition risk — or the risk of potential costs incurred to meet carbon-reduction requirements as part of the transition to a low-carbon economy. By some estimates, real estate accounts for up to one-third of global energy-related CO2 emissions; and so, as the global economy attempts to decarbonize, there will likely be significant cost implications for real estate investors.2 Therefore, investors may wish to consider both physical and transition risk when assessing their real estate portfolios' exposure to climate change.

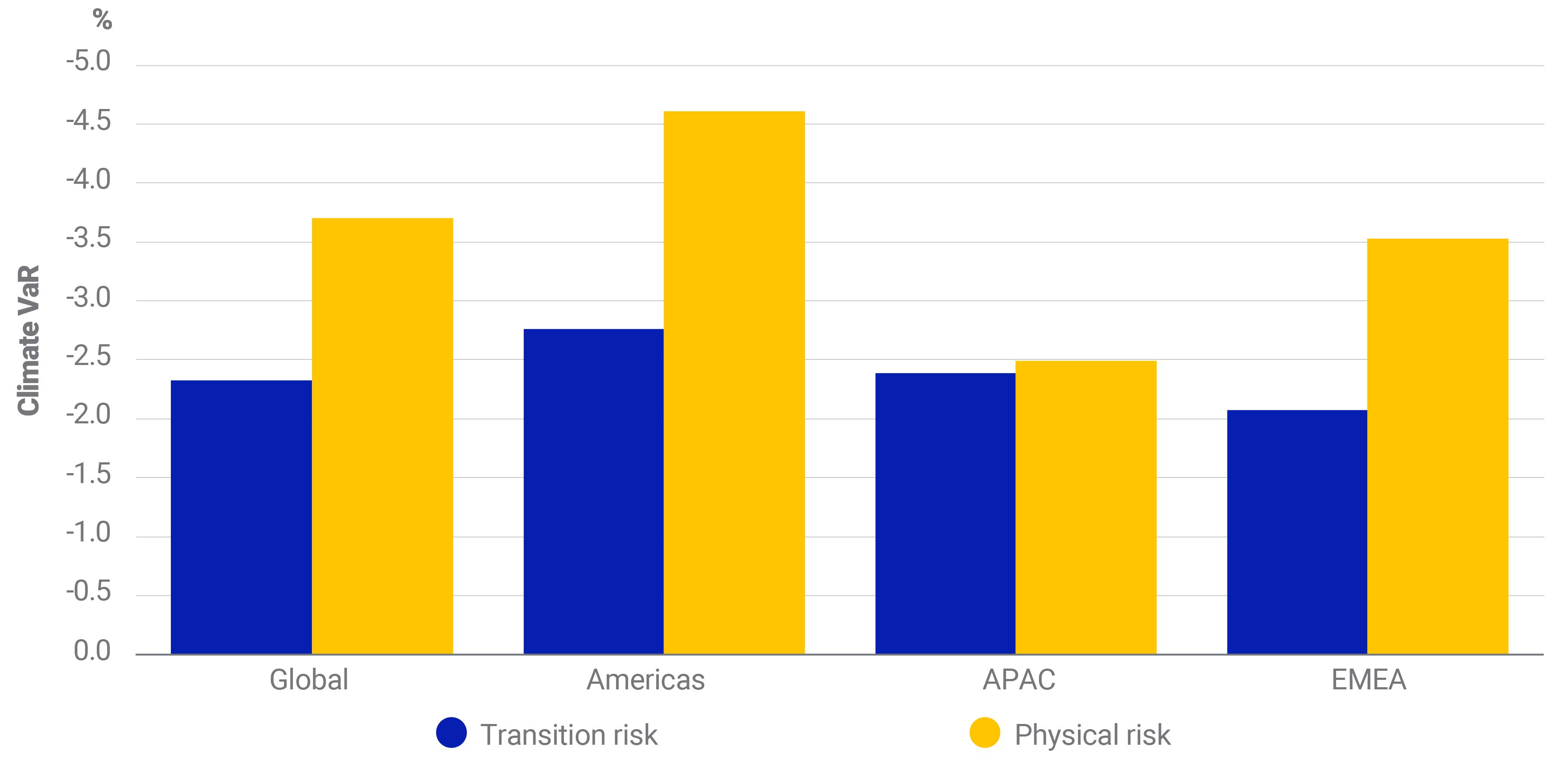

For example, under the default scenarios in the MSCI Real Estate Climate Value-at-Risk Model, properties from the MSCI Global Property Index were projected to have a physical value-at-risk of -3.7% and a transition value-at-risk of -2.3%.

Projected climate risk in MSCI Global Annual Property Index

3. Transition risk is all about tax

When thinking about transition risk, investors may initially think about regulations like New York's Local Law 97, which aims to limit emissions by setting caps and imposing penalties for exceeding those caps. But transition costs will not just be realized through taxes and penalties. Taxes may form part of the potential costs in some jurisdictions, but the costs of decarbonizing real estate could also come in several other forms. One avenue could be through capital expenditure, investing in energy-efficiency and carbon-intensity upgrades for the assets like new windows, more efficient HVAC systems or low-carbon fuel switching. These upgrades reduce the cost of lighting, heating and cooling buildings and therefore help lower the carbon footprint of the assets. Another avenue could be through carbon offsets, which may form part of investors' strategy for reducing assets' net carbon footprint. Tenancy demand could also fall as organizations set and implement net-zero goals (particularly in less efficient assets), resulting in lost rents for landlords. For most assets, investors will face a variety of transition costs — not all of them related to regulation and tax.

4. All physical hazards are climate-change risks

Buildings face numerous physical hazards that vary depending on where they are located, how they are constructed and how they are used. These include geophysical, meteorological, hydrological and climatological hazards. But not all of these hazards are linked to climate change. For a physical hazard to be a climate-change risk, it must be clear how the changing climate will affect the frequency and severity of the risk. For instance, the physical underpinnings of a hydrological hazard like coastal flooding are well understood, so climate scientists can model how projected sea-level rise will affect them. Thus, coastal flooding is a clear climate-change risk. By contrast, a geophysical hazard like earthquakes would typically not be considered a climate-change risk, as earthquakes are primarily a tectonic phenomenon and not directly linked to climate change.

Examples of physical hazards that are climate-change risks

5. Physical climate-change risks are already priced in

It can be easy to confuse physical climate risk with physical climate-change risk. All buildings are subject to some level of current physical risk, but current exposure to physical hazards does not equate to climate-change risk, because current hazard levels should be known and reflected in current asset prices. However, climate change stands to fundamentally alter global weather patterns and introduce changes that are not currently priced in given the level of uncertainty involved. Physical climate-change risk is therefore all about the difference between current and future hazard exposure.

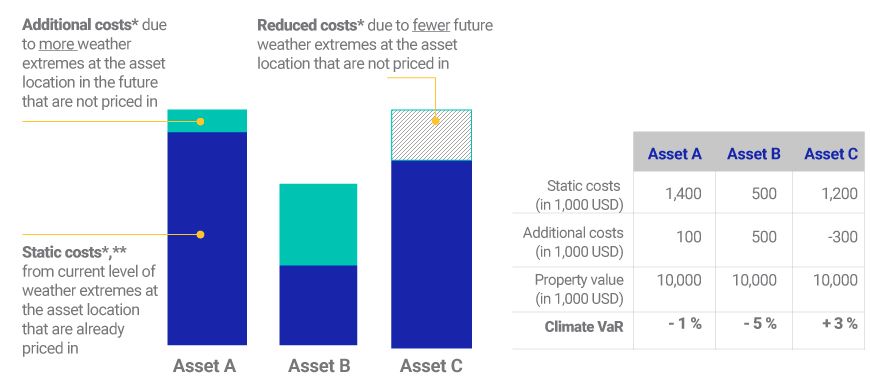

The change to hazard levels may also not be proportional to current levels. In the example below, we show three hypothetical assets that have different levels of physical risk exposure. Asset A has both a higher current and predicted future hazard exposure than Asset B. However, the projected increase for Asset B is larger, so Asset B has a higher value-at-risk percentage. Asset A, despite its overall larger exposure, has a smaller value-at-risk percentage, since this metric reflects costs not already priced in. Investors should therefore not always expect to see the highest value-at-risk percentages in assets with the highest current hazard exposures.

*Costs are discounted and aggregated between today and the year 2100. **Assuming no climate change between today and 2100. Source MSCI ESG Research LLC

In some rare instances, climate-change risk models may project a reduction in hazard exposure. For example, an asset currently subject to a higher level of fluvial-flooding risk may see a projected decrease in exposure due to changes in precipitation patterns. In cases like this, an asset can have a relatively high current and predicted future exposure to physical risk, as illustrated by Asset C, but the predicted reduction in priced-in hazard exposure means that the asset has a positive value-at-risk percentage. Investors should be careful to not interpret the positive value-at-risk as an indication that the asset is free from hazard exposure.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1The median time between purchase and sale in the MSCI Global Property Index is approximately six years, but a quarter of the assets have sold after 10 or more years.2A 2019 United Nations Environment Programme report found that buildings represent 28% of global energy-related CO2 emissions (39% when construction emissions are included).

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.