GICS Changes: Risk Depends on How It’s Measured

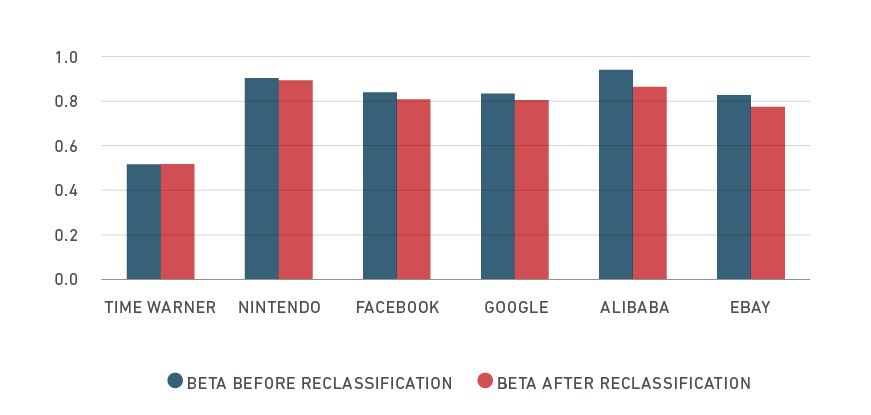

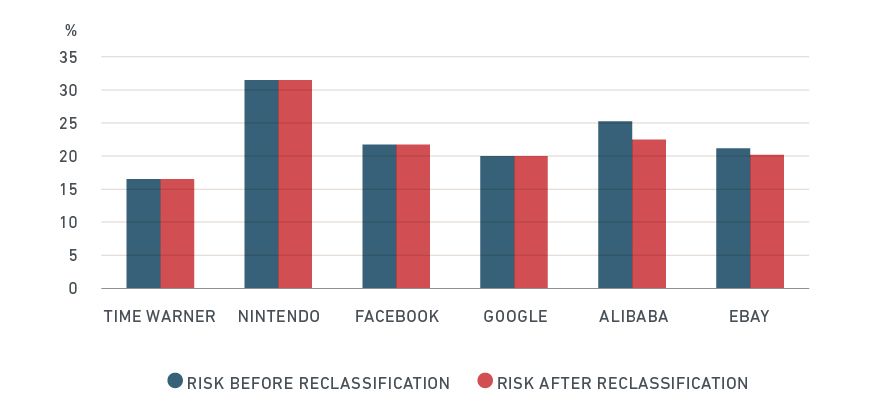

On Sept. 28, 2018 over USD 3 trillion in market capitalization will switch sectors because of changes to the Global Industry Classification Standard (GICS®)1 structure; specifically, the Telecommunications Services sector will significantly broaden and be renamed Communications Services. Our recent paper, "The New GICS Communication Services Sector," provides full details. What does this change mean for the risk profiles for six of the largest companies affected? While reclassifying a stock's sector or industry may change the way the market views that stock over the long term, financial theory says that reclassification alone should not dramatically change its short-term behavior. Our analysis suggests that industry changes occurring as a result of the GICS sector changes would have decreased predicted Beta and total risk for some of these companies.

Company Name | New GICS Sector? | Current GICS Sector | New GICS Sector | New GEMLT Industry Factor? | Current GEMLT Factor | New GEMLT Factor |

|---|---|---|---|---|---|---|

Company Name Time Warner | New GICS Sector? Yes | Current GICS Sector Consumer Discretionary | New GICS Sector Communication Services | New GEMLT Industry Factor? No | Current GEMLT Factor Media | New GEMLT Factor No change |

Company Name Nintendo | New GICS Sector? Yes | Current GICS Sector Information Technology | New GICS Sector Communication Services | New GEMLT Industry Factor? No | Current GEMLT Factor Software | New GEMLT Factor No change |

Company Name | New GICS Sector? Yes | Current GICS Sector Information Technology | New GICS Sector Communication Services | New GEMLT Industry Factor? No | Current GEMLT Factor Internet | New GEMLT Factor No change |

Company Name | New GICS Sector? Yes | Current GICS Sector Information Technology | New GICS Sector Communication Services | New GEMLT Industry Factor? No | Current GEMLT Factor Internet | New GEMLT Factor No change |

Company Name Alibaba | New GICS Sector? Yes | Current GICS Sector Information Technology | New GICS Sector Consumer Discretionary | New GEMLT Industry Factor? Yes | Current GEMLT Factor Internet | New GEMLT Factor Retailing |

Company Name eBay | New GICS Sector? Yes | Current GICS Sector Information Technology | New GICS Sector Consumer Discretionary | New GEMLT Industry Factor? Yes | Current GEMLT Factor Internet | New GEMLT Factor Retailing |

In GEMLT, risk model construction depends on industries and not on sectors.

Simulation was performed for Oct. 2, 2017

Neither individual asset volatility nor correlations between factors were importantly affected in this scenario. However, companies that are exposed to a different industry after reclassification will get a different risk contribution from the new industry. Therefore, we attributed most of the change in both risk indicators to this industry shift. As some very large companies switch GICS sectors, there will likely be implications for investors. Some will be induced by the reclassification itself while others will be caused by changes in the way the market views these securities because of a change. Based on our analysis, investors may want to consider whether sector reclassification may ultimately have an effect on the risk profiles of individual stocks in their portfolios.

1 GICS, the global industry classification standard jointly developed by MSCI and Standard & Poor's.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.