Global Real Estate: The Conundrum of High Prices and Wide Yields Spreads

Blog post

July 15, 2015

Historically, the majority of global real estate returns have come from income, which has made up more than 80% of the total return over the past decade. In 2014, however, growth in asset values represented 43% of the total return — more than double its long-term average contribution. This trend was driven largely by the weight of capital flowing to real estate and by yield compression. All the same, as of December 2014, income return remains above 5%, despite having fallen in each of the last four years, and is significantly higher than the yields available for global equities and bonds.

For many institutional investors, high pricing is a concern across markets, and this represents a growing risk for real estate investors. At a global level, recent income yields and spreads with bond yields point to real estate being more aggressively priced than at any time since just before the global financial crisis. The difference this time is the persistence of wide spreads due to unusually low interest rates.

A critical question is how real estate yields will respond if and when interest rates start to rise. This response will depend on a complex set of factors including the level and speed of rate increases and the reasons behind them, combined with the performance of real estate fundamentals. The difficulty of gauging current pricing and prospects for real estate markets represents a major challenge for investors and portfolio managers.

For many institutional investors, high pricing is a concern across markets, and this represents a growing risk for real estate investors. At a global level, recent income yields and spreads with bond yields point to real estate being more aggressively priced than at any time since just before the global financial crisis. The difference this time is the persistence of wide spreads due to unusually low interest rates.

A critical question is how real estate yields will respond if and when interest rates start to rise. This response will depend on a complex set of factors including the level and speed of rate increases and the reasons behind them, combined with the performance of real estate fundamentals. The difficulty of gauging current pricing and prospects for real estate markets represents a major challenge for investors and portfolio managers.

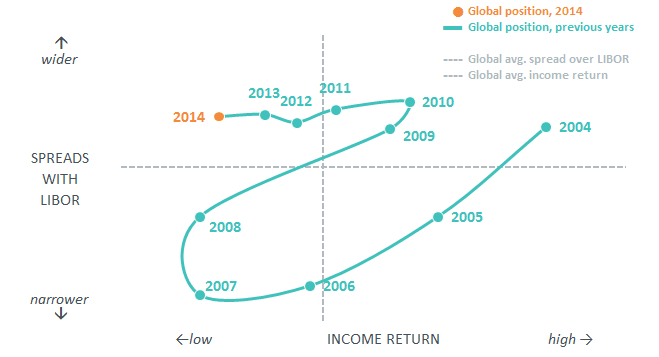

Yield spread vs income return at a global level

Source: MSCI

Global real estate income returns are now back close to pre-crisis lows, but markets continue to be supported by wide spreads with interest rates.

Read the complete report, "Real Estate Market Insights – Global."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.