Global Real Estate: To Hedge, or Not to Hedge

Blog post

September 12, 2018

While not quite as profound as the Shakespearean original, it is still quite a tricky one for real estate investors to grapple with. Until fairly recently, it is one that has been avoided by the majority of real estate investors due to their heavy home bias. But the increasing global nature of the asset class, combined with rising currency volatility, means the question is becoming increasingly difficult to avoid.

LOCAL COUNTRY BIAS

Historically, real estate investors have had a strong home bias. MSCI surveyed a large group of institutional investors in 2013 which revealed that, on average, 83% of real estate was domestically invested.1 However, the world's largest sovereign wealth funds and pension funds are gradually eroding this home bias. More broadly, an improved understanding of the role of real estate within a multi-asset class portfolio and an increased awareness of the potential diversification benefits from international real estate exposure are helping to boost cross-border real estate investment.

GOING GLOBAL

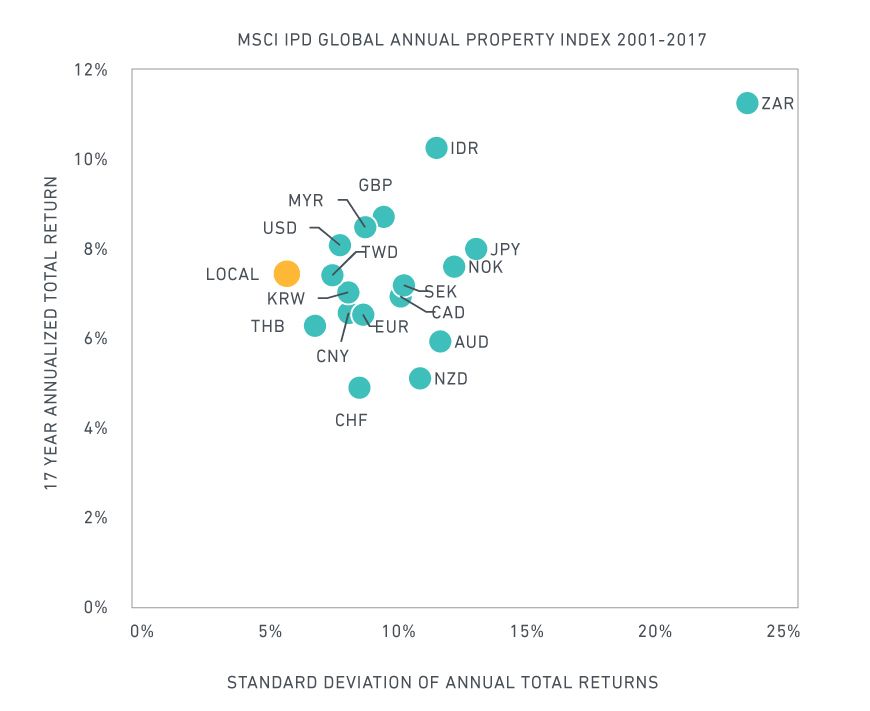

Currency movements can have a big impact on performance as the exhibit below demonstrates. Over the full 17-year history of the MSCI Global Annual Property Index, the annualized total return was 7.4% (measured in local currency terms). However, performance can look very different when measured in other currencies. For example, in South African rand, the index's annualized total return would have been 11.2% while if measured in Swiss francs, the total return would have been 4.9%.

The stability of returns can also be strongly impacted by currency movements. Therefore, investors with foreign currency exposures may wish to think carefully about how they manage such exposures.

Currency has significantly affected performance

Source: MSCI – Global Intel PLUS

BUT IS CURRENCY THE ONLY QUESTION?

Unlike Hamlet's ultimate question, currency risk management in real estate is somewhat more nuanced. Other factors such as what should be hedged or when is the right time to hedge are important considerations. A recent MSCI article published by the Pension Real Estate Association (PREA) explores some of these issues in more detail including assessing the cost and regulatory hurdles in managing currency risk.

While there are a number of potential factors to consider and many of the decisions may not be straightforward, one thing is clear: As real estate becomes increasingly global in nature, more and more investors could find that currency becomes a growing source of investment risk.

1 Based on 138 asset owners. See Hobbs, P., B. Teuben, N. Gilfedder and Z. Marossy. " The Asset Owner Real Estate Investment Process: Risk Management Insights from the MSCI/IPD survey." (2014). MSCI.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.