How Brexit May Impact your Portfolio

Blog post

March 21, 2016

Co-authors: Jahiz Barlas, Vice President, Multi Asset Class Research, Raghu Suryanarayanan, Head of Macroeconomic Risk and Asset Allocation Research and Carlo Acerbi, Risk Research

Britain's leaving the European Union would send the U.K. and Europe into the unknown with possibly major consequences for multi-asset class portfolios.

With a referendum set for June 23, opponents of a Brexit say it would usher in a decade of uncertainty in which the pound melts down, trade tumbles, and U.K.-based firms decamp to Europe. Proponents of Brexit say the U.K. does not have to choose between sovereignty and trade, and that Britain can negotiate its own trade deals and better control its borders by severing ties.

To help institutional investors evaluate the impact of a Brexit on their portfolios, MSCI has modeled two scenarios. The first envisions a moderate impact with limited spillover to the rest of the EU and the global economy. The second foresees more disruption.

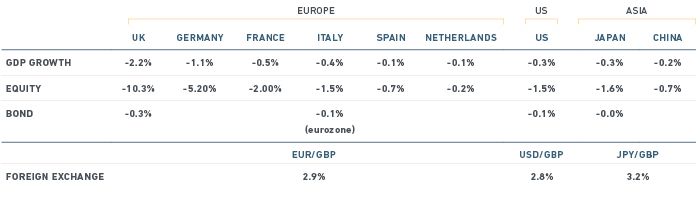

Brexit with limited spillover The first scenario assumes that a Brexit would slow the growth of U.K. real GDP by 2.2% over the year that follows the vote.* According to MSCI's Macroeconomic Risk Model, which links factors such as GDP and inflation to portfolio returns and risk, the slowdown would produce a corresponding decline of 10% in U.K. equities and a contraction of 30 basis points (bps) in the yield on 10-year U.K. government bonds. In addition, the British pound could fall about 2.8% relative to the U.S. dollar.

Brexit with limited spillover The first scenario assumes that a Brexit would slow the growth of U.K. real GDP by 2.2% over the year that follows the vote.* According to MSCI's Macroeconomic Risk Model, which links factors such as GDP and inflation to portfolio returns and risk, the slowdown would produce a corresponding decline of 10% in U.K. equities and a contraction of 30 basis points (bps) in the yield on 10-year U.K. government bonds. In addition, the British pound could fall about 2.8% relative to the U.S. dollar.

The impact on the rest of the world would turn mostly on trade with the U.K. Not surprisingly, the eurozone stands to slow the most. The U.S. would remain relatively unaffected, with a drop of 0.3% in GDP and an incremental slide of about 1.5% in equity markets over the same period. The effect on Japan and China would be even more attenuated.

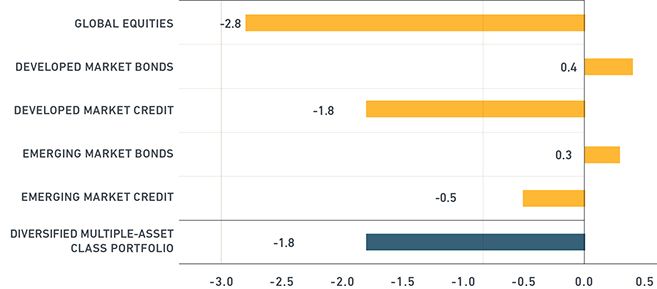

A moderate spillover would lead to similarly muted effects on major indexes, with an incremental fall of 2.8% in global stocks and modest losses in corporate and emerging-market debt. A global, diversified multi-asset class portfolio of equities, bonds, and credit would experience a modest loss of 1.8%.

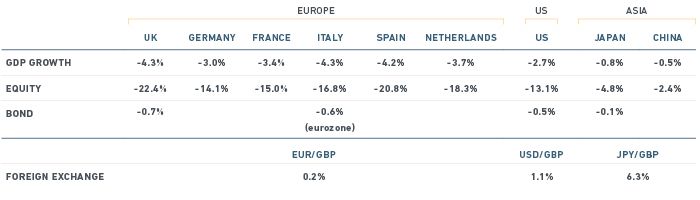

Brexit with contagion The second scenario envisions that a Brexit would shatter the eurozone and drag down growth across the world. U.K. economic growth would slow by 4.3% annually over the year that ensues.** The slowdown would produce a falloff of 22% over the same period in U.K. equities, according to MSCI's Macroeconomic Risk model. Yields on 10-year U.K. bonds would slip 0.65%. The British pound could depreciate as much as 6.3% relative to the Japanese yen.

Brexit would shred growth across the EU, including by 4.2% in Spain, 3.7% in the Netherlands, and 4.3% in Italy. MSCI's Macroeconomic Risk Model suggests that equities markets across the continent would tumble as well, including by 21% in Spain, 18.3% in the Netherlands and 17% in Italy.

The break-up of the world's largest trading bloc would ripple across the global economy. Growth in U.S. real GDP would fall 2.7% over the three years that follow a vote, with a corresponding decline of 13.1% in U.S. equities and a contraction of 0.53% on the yields in U.S. corporate bonds.

Japan would slow 0.8% on an annualized basis, with a decline in equities of roughly 5%. The effect would be more attenuated in China, where Brexit could slow growth by 0.5% and cause equities to fall 2.4%.

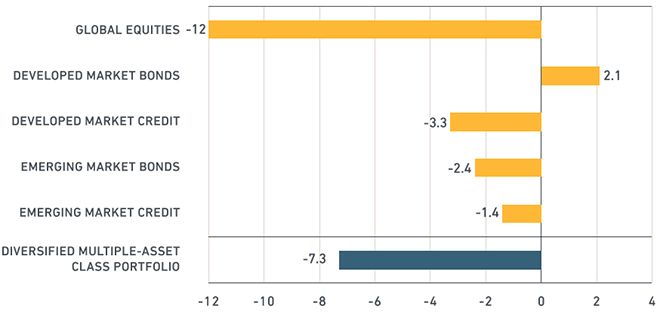

Looking across asset classes, the contagion scenario for Brexit would lead to incremental losses of 12% in global equities and losses in corporate and emerging-market debt. Government bonds would gain 2.1%. A global, diversified multi-asset class portfolio could suffer a loss of 7.3%.

To view the effects of both scenarios for a Brexit on equities, sovereign debt and high-yield bonds by country and sector, as well as for information on how to use MSCI's RiskManager to model the effect of a Brexit on your portfolio, read more.

What's next That's up to Britons. Arguments for and against a Brexit seem likely to be honed between now and when voters head to the polls. Would you like to know how to implement this Stress Test using RiskManager? Read our implementation guide. * Assumptions based on findings by Gianmarco Ottoviano, João Paulo Pessoa, Thomas Sampson and John Van Reenan as described in "The Costs and Benefits of Leaving the EU," Centre for Economic Performance, May 13, 2014 ** Assumptions for the impact of a eurozone breakup are based on findings by Mark Cliffe, Maarten Leen and Peter Vanden Houte that are described in "Quantifying the Unthinkable," ING, July 7, 2010.

What's next That's up to Britons. Arguments for and against a Brexit seem likely to be honed between now and when voters head to the polls. Would you like to know how to implement this Stress Test using RiskManager? Read our implementation guide. * Assumptions based on findings by Gianmarco Ottoviano, João Paulo Pessoa, Thomas Sampson and John Van Reenan as described in "The Costs and Benefits of Leaving the EU," Centre for Economic Performance, May 13, 2014 ** Assumptions for the impact of a eurozone breakup are based on findings by Mark Cliffe, Maarten Leen and Peter Vanden Houte that are described in "Quantifying the Unthinkable," ING, July 7, 2010.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.