- The COVID-19 pandemic has hit China's economy badly and may lead to a rise in delinquency rates for all types of consumer loans, due to reduced borrower income, laggard collection efforts and borrowers' prioritizing cash over paying debt.

- The impact will likely vary across asset classes and securities. Residential mortgage-backed securities (RMBS) could be more resilient, while uncollateralized consumer loans could be hit the hardest.

- Whether the situation will improve depends on variables: how soon the epidemic will end and normal economic order resume; the effectiveness of government efforts in stimulating the economy; and when loan servicing will be restored.

An economy hit by an epidemic

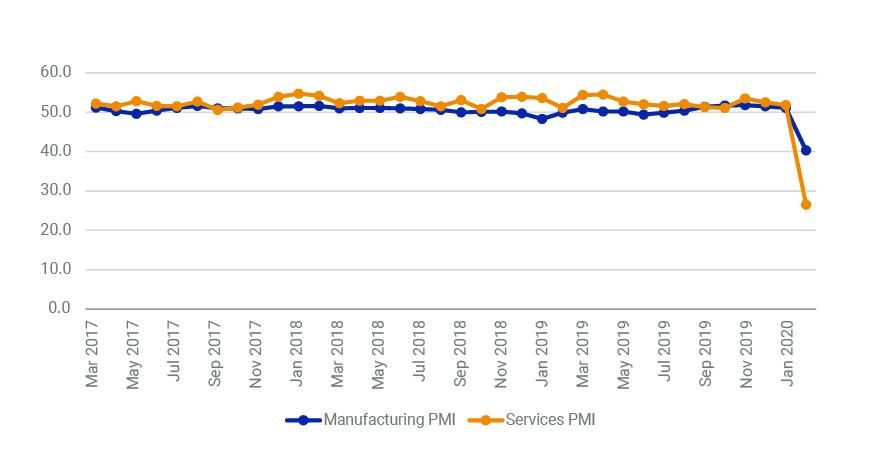

Chinese economic activity slowed considerably due to the outbreak. The Caixin-Markit purchasing managers' index (PMI) for manufacturing hit 40.3 in February 2020, its lowest level since the survey began in 2004.2 The Caixin China services PMI recorded only 26.5 in February, falling 50% from the previous month — the first time below the breakeven threshold, since the survey was launched in November 2005.

China PMI's drop-off showed outsize impact on services

Seasonally adjusted coronavirus impact on Chinese purchasing managers' index. Source: Caixin, Markit

COVID-19's potential impact on ABS

First-quarter China GDP growth may turn negative, and services firms could be impacted more severely than manufacturers, as the PMI surveys suggest. For example, the year-over-year change for box-office revenue at movie theaters during the week of spring festival dropped by 99.4%;3 meanwhile, travel during the same week dropped 63.9% compared to last year, leading to a potential loss for tourism of CNY 3 trillion.4

We used our model for Chinese ABS to analyze the potential impact on Chinese consumer ABS from three key risks:

- Reduced income. While it generally takes about 20 days after spring festival for manufacturing companies to get back to full capacity,5 the latest estimate of the full resumption is late March — almost 60 days after the holiday. Taking that assumption into account in our model, as well as the assumption that services employees' income will likely be reduced due to gaps in employment, the model suggests increased delinquency among borrowers who work in services.

- Laggard collection efforts. To make things even worse, a lot of the collection staff in the Chinese financial sector are located in Wuhan, the epicenter of the coronavirus outbreak. The list of employers includes China Minsheng Bank, China Merchants Bank, Bank of Communications and Home Credit (the largest licensed consumer finance company in China). Home Credit alone has more than 5,000 employees in Wuhan. According to our what-if analysis, disruptions in servicing the ABS could increase delinquencies.

- Borrowers' unwillingness to pay down debt. Assuming that the virus outbreak and its social impact could encourage people to hoard cash, our model suggests that such a scenario would lead to higher delinquency rates. Our model also indicates lower loan balance and lower borrower income show higher credit risk; thus credit cards and uncollateralized consumer loans will face higher delinquency increase.

Data delay clouds the picture

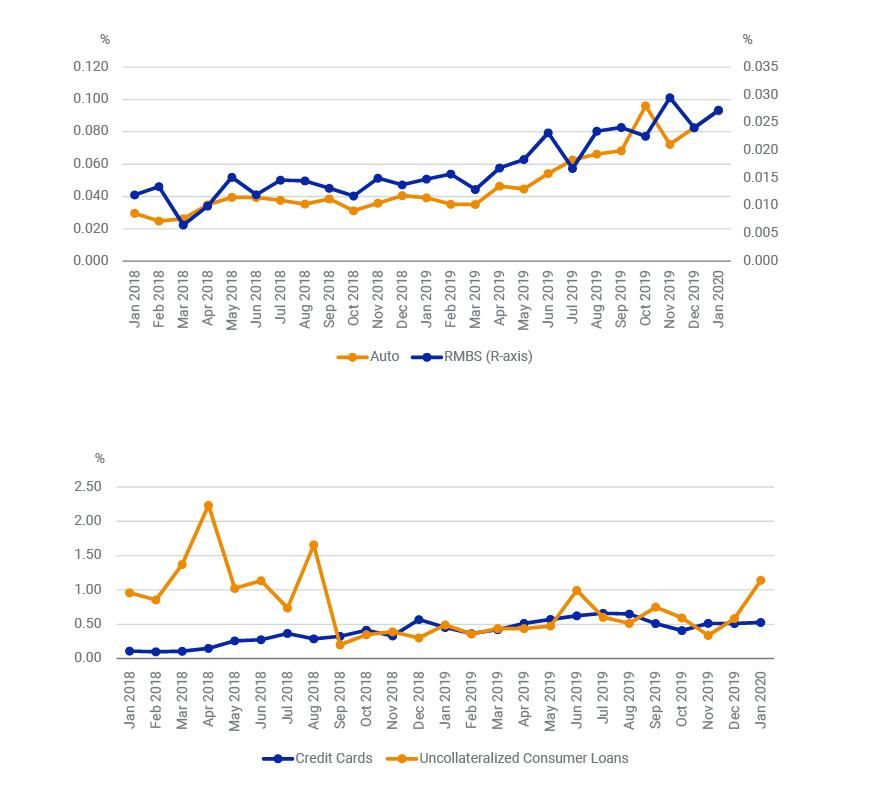

Due to the delay of available data, we won't be able to observe the impact directly, since default is generally defined as a post-90-day delinquency event. If people stopped making payments by the end of January, for example, the default amount will not be disclosed until April or May. Default rates for all major asset classes (residential mortgages, auto loans, credit cards and uncollateralized consumer loans) have risen significantly since 2018, according to data from CNABS, which reflects the latest payment behavior by ABS special-purpose vehicles (as of Feb. 7, 2020). However, the virus outbreak's impact on Chinese ABS performance will likely vary across sectors and securities.

Default rates were rising even before coronavirus outbreak

Monthly default rates of pre-2019-vintage Chinese consumer ABS. Source: CNABS, MSCI

For residential mortgages, the default event is driven not only by the borrower's ability to pay, but by the collateral value. MSCI's Chinese-ABS model estimates higher sensitivities to house prices and trends than to temporary dislocation of income for this sector.6 Given government policies supporting the real estate industry, the housing market may not experience a significant negative impact from the pandemic.7 Due to demand for residential spaces, borrowers could make their mortgages the highest priority among all debts. For these reasons, mortgages may experience only an uptick in default rates

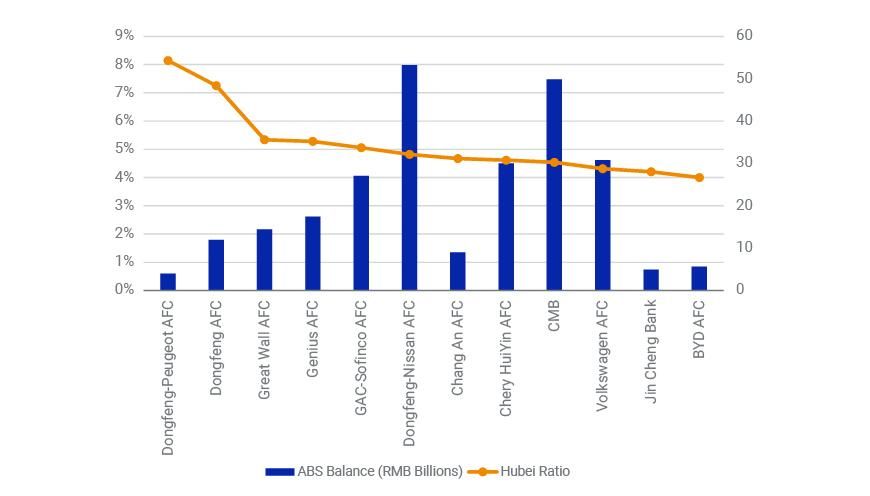

For auto-loan ABS, the coronavirus impact could be higher than for residential mortgages, due to the former's rapidly depreciating collaterals. MSCI's model for Chinese ABS estimates higher overall sensitivities to income changes and assumes they will vary across geographical areas and in how the autos in question are used. The impact on loans for non-business personal cars may be less than for business-car loans, whose income may be affected by delays in resuming work, limited passenger ridership and other factors. Issuers whose loans are concentrated in the affected geographical regions may be affected more severely. For example, Dongfeng AFC and Dongfeng-Peugeot AFC — which have significantly higher exposure in Hubei province, with loan-balance ratios of 7.1% and 8.3%, versus the industry average of 3.9% — could face higher delinquency rate rise, compared with their peers.

Auto-ABS issuers' exposure to Hubei province

Source: MSCI, CNABS

For credit cards — based on estimates from our model — the early-delinquency rate could rise if GDP drops, because the default rate of this asset class has historically been very sensitive to the overall economy. For example, in the first quarter of 2018, the GDP growth rate was 6.8% and the monthly default rate was 0.1%. Meanwhile, in the third quarter of 2019, the GDP growth rate was 6.0% and the default rate was 0.65%.8 Slow or negative economic growth could disproportionately affect the financial wellness of the population with lower or less stable income.

Issuers that targeted customers like government workers and employees at state-owned enterprises (who have relatively stable income during the quarantine period9) could experience a lower rate of delinquencies than issuers that targeted customers at the low end of the credit spectrum. Geographical exposure could also matter: China's top three credit-card companies — China Merchants Bank, Bank of Communications and China CITIC Bank — have their major operational centers in Wuhan. That exposure could reduce operational efficiency and potentially further weaken their credit-card loans' performance, our model assumes.

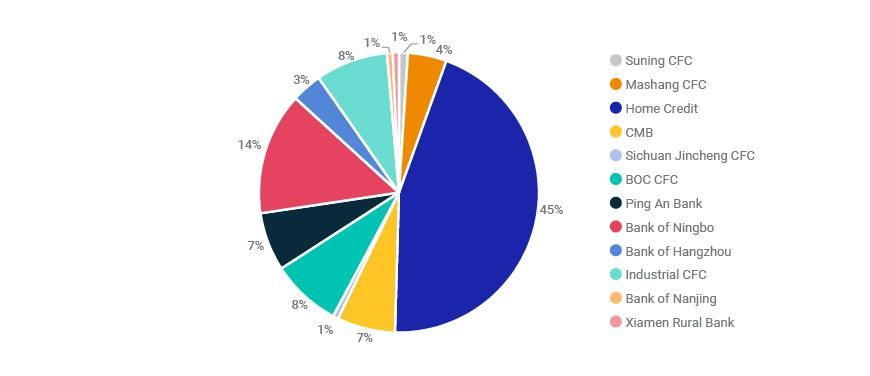

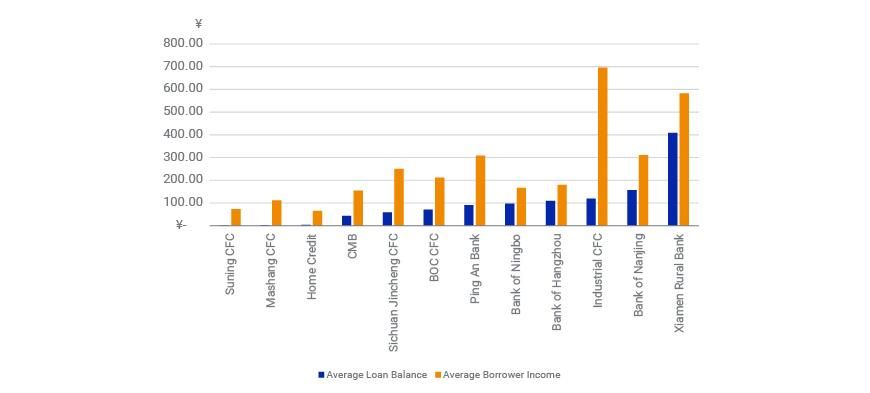

Uncollateralized consumer loans could experience the highest rise in default rates, in our analysis. Among the four asset classes we reviewed, these loans have the highest historical default rate. MSCI's Chinese-ABS model estimates they have among the highest sensitivities to short-term economic dislocations, because borrowers in this category have the weakest credit and the issuers tend to have less-effective collection abilities than banks do. In the U.S., default rates for this category often increase dramatically during a recession. We estimate similar performance for Chinese uncollateralized consumer loans, if the national or regional economy stalls due to the virus outbreak. Relative performance among customer groups could further diverge, as issuers that aggressively lent to customers with higher credit risks could be hurt worse. For example, issuers of loans with relatively small balances, lower borrower income and higher interest rates could face a larger increase in default rates.

Issuers of uncollateralized consumer loans by market share

Source: CNABS, MSCI

Uncollateralized consumer loans: Average loan balance vs. average borrower income

Figures in CNY thousands. Source: CNABS, MSCI

Overall, the COVID-19 pandemic could have a significant impact on Chinese consumer ABS — and that impact could be disproportionate among particular asset classes and types of issuers. Investors may wish to keep an eye on the issuer's lending standards and the quality of the underlying collateral.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Chen, J. 2020. “MSCI China ABS Collateral Model.” MSCI Model Insight. (Client access only.)2“The effects of the economic shock of the service industry.” March 4, 2020.3Zheng, R. “2020 Spring Festival closed with 23.57 million yuan box office.” , Feb. 2, 2020.4Zhou, J. “Tourism industry affected by epidemic.” , Feb. 11, 2020.5Yu, H. “Caixin PMI Analysis.” , March 4, 2020.6“MSCI China ABS Collateral Model.”7“Many provinces and cities have successively introduced real estate support policies.” , Feb. 19, 2020.8“Quarterly gross domestic product (GDP) growth rate in China Q4 2017-Q4 2019.” , March 2, 2020.9Yang, Y. “Real estate companies in the epidemic: Small and midsize developers cut wages and lay off employees, while big SOEs are gaining ground.” , March 10, 2020.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.