Improving Stock Selection in the Age of Big Data

Blog post

November 20, 2017

In the age of big data, fundamental stock pickers face a major challenge. Stock selection typically depends on establishing research conviction in the operating models of companies, such as identifying inexpensive businesses that demonstrate sustainable competitive advantage, disciplined capital management and strong corporate governance. The stock picker's edge may rely on analyzing information and top-notch research skills.

Yet this task is becoming progressively harder due to the rising quantity of available information. Some estimates suggest that about 4,000 brokerage reports are produced daily, comprising 36,000 pages in 53 languages.¹ How can the most valuable information from these sources be identified and summarized?

MSCI researched how fundamental company characteristics, such as value, quality and momentum, have affected expected equity return and risk since the 1970s. Understanding the impact of return drivers on portfolio assets can help fundamental managers assess whether a good company identified through proprietary research is also likely to be a good investment.

Important drivers of returns identified by MSCI²

Each category of return drivers is supported by a number of fundamental or technical measures. Some will be very familiar to fundamental managers: the metrics in the quality category are related to resilient business models, conservative accounting practices and assessing whether management acts in shareholders' best interests. On the other hand, the ability to account for the estimated impact of factors such as analyst sentiment or downside risk may be new to many managers.

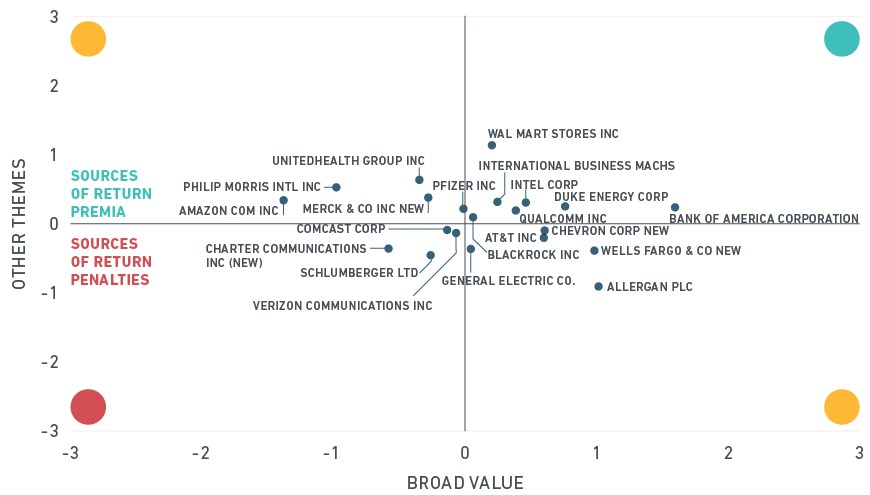

We summarize the estimated influence of these themes on stock returns with a simple chart, illustrated below for a value manager:

What makes for a good value stock?

Analysis date is Sept. 30, 2017

The horizontal axis shows the expected return contribution from value, summing up effects from book to price, earnings yield and reversal.³ It is constructed so that all assets with scores above zero on this axis are expected to have a stronger contribution to their return coming from valuations than the average stock in the benchmark. In this example, companies on the right hand side of the chart would be viewed as value stocks.

The vertical axis shows the expected contribution to the stock's return coming from systematic drivers not related to valuations. Assets in the top half of the chart (those scoring above zero on the vertical axis) are expected to have "tailwinds" supporting their returns. For example, these stocks could have higher dividend yields or better earnings quality. Conversely, assets in the bottom half of the chart are exposed to systematic effects that have historically been associated with underperformance.

The upper right quadrant, therefore, screens the portfolio for value stocks that are exposed to other systematic effects historically associated with better performance. Stocks in the bottom right quadrant are value stocks, but their exposure to potential "headwinds" from other systematic drivers may lead the manager to assess his conviction in these assets more closely. Stocks in the bottom left quadrant may require the strongest scrutiny by the portfolio manager: These assets may not be value stocks and they are exposed to systematic drivers historically associated with underperformance.

The chart offers a simple way to summarize the effects of systematic drivers of return for a universe of stocks. It is fully customizable — in the example above, we could have replaced value with any other investment style. It offers a visual comparison between multiple companies on one page, allowing managers using classic stock-picking approaches to examine their portfolios, watch lists or universes. We believe that it can enhance the key aspects of the fundamental investment process, such as screening, idea generation and the monitoring of portfolio positions through time.

¹ Blackrock. (2015). "Finding Big Alpha in Big Data."

² This exhibit does not show a complete list of measures that MSCI uses in its models.

³ The expected return contributions are calculated using a model-based approach. First, we estimate the historical return premium associated with each fundamental or market characteristic. We then adjust this historical premium for the current risk environment, using volatility forecasts from Barra models. A stock has greater or lesser sensitivity to each characteristic depending on its fundamentals (for example, reported dividend yield or analyst forecasts of earnings to price) or market behavior (for example, price momentum). The expected return contributions are then shown as scores.

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.