Investing in Convertible Bonds When Rates Rise

Blog post

November 30, 2018

Like many investors, fixed-income managers are looking for ways to hedge against the risk that interest rates will continue to rise. Historically, convertible bonds have been used as a hedging option by many investors, due to their relatively lower duration, their potential upside from embedded equity call options and healthy issuance (especially in the technology sector). However, they are not the most straightforward of asset classes, and it may be challenging for investors to fully appreciate their exposures to different sources of risk. Is my convertible bond more like a stock or a bond? How can I identify convertible bonds offering protection from rising rates?

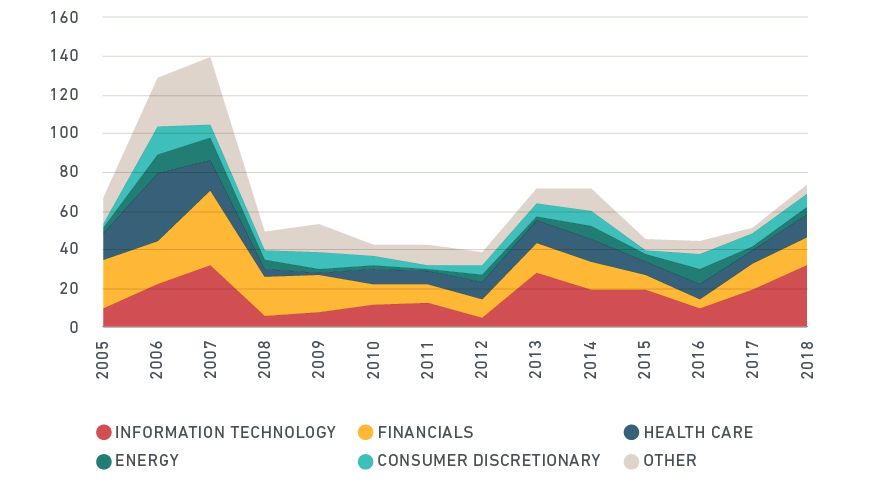

US convertible bond issuance by sector (USD billion)

Source: Reuters

DISSECTING DRIVERS OF PERFORMANCE

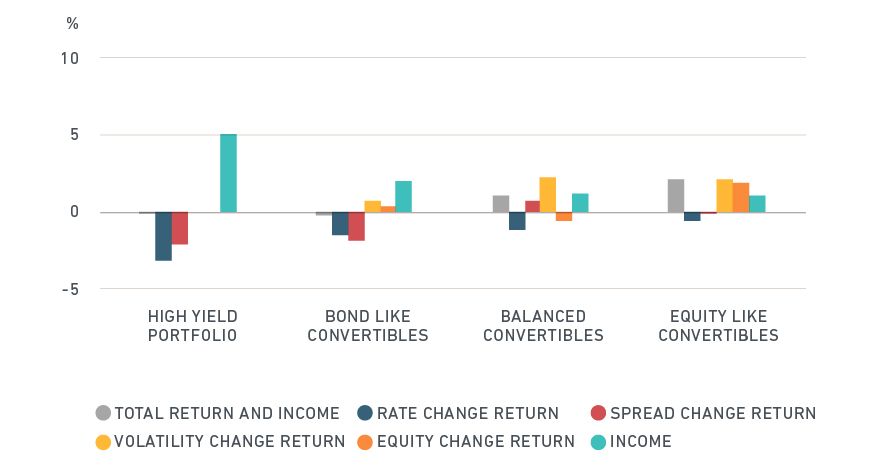

Using the MSCI Convertible Bond Pricing Model, we analyzed a representative portfolio of convertible bonds issued in the U.S.1 and divided the portfolio into three categories based on the equity exposure as of Jan. 2, 2018: bond-like convertibles, balanced convertibles and equity-like convertibles.2 These categories accounted for 15%, 25% and 60% of the portfolio, respectively. We compared these sub-portfolios to a representative U.S. high-yield bond portfolio3 to highlight the similarities and differences between their respective investment characteristics. We attributed returns to income and relevant market factors: yields, spreads, equities and volatility (see exhibit below).

Drivers of convertible bond performance

Performance Attribution (Jan. 1 – Nov. 22, 2018)

Source: MSCI, Reuters. Data from Jan. 2, 2018 to Nov. 22, 2018

For the U.S. high-yield corporate bond portfolio, all the coupon income was offset by losses due to rising yields and spreads. The bond-like convertible bonds demonstrated very similar behavior. Balanced and equity-like convertible bonds, however, benefited from equity and volatility exposure, especially volatility.

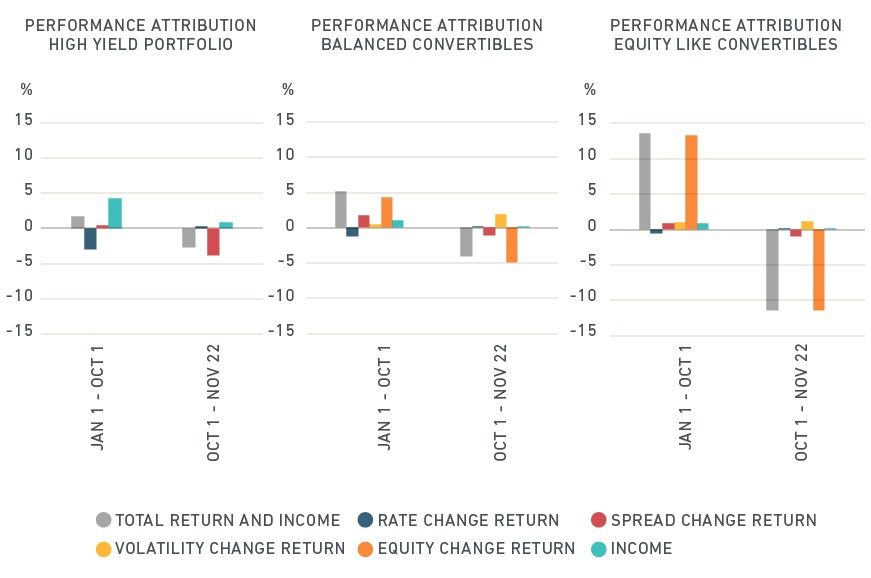

To highlight the differing characteristics of the various convertible bonds, we extended our analysis further, by dividing the Jan. 2 – Nov. 22 time-period into two distinct groups: a relatively calm period until October, where Treasury yields and equity prices increased, followed by a period when equity markets experienced increased volatility and spreads widened (Oct. 1 – Nov. 22). Equity markets are at the same point where they were at the beginning of the year for the period under review.

Some convertible bonds held up better than others

The high-yield portfolio suffered losses in the first period due to the interest-rate environment, whereas convertible bond portfolios provided exceptional returns on the back of rising equity markets. In October and November, the high-yield portfolio suffered losses dwarfing coupon income because of spread widening. Balanced convertible bonds suffered slightly higher losses during the October – November period due to equities but losses were similar in magnitude to the high-yield bond portfolio, underscoring the equity-like characteristics of high-yield bonds. Equity-like convertible bonds lost considerably more in the last two-month period, but they were still at break-even due to the exceptional returns they provided in the first half of the year.

What delivered consistent returns in our analysis was volatility. For both convertible portfolios, for both periods, the volatility contribution was positive, especially in the second, more volatile period.

OTHER RISKS TO EVALUATE WITH CONVERTIBLE BONDS

As well as the complexities of which convertible bond to opt for in a rising interest-rate environment or period of heigtened volatility, other risks may need to be taken into account. Apart from the increasing probability of defaults or the widening of spreads, convertible bonds are also exposed to the vagaries of equity markets. Historically, decreasing equity prices have always had a direct negative effect on convertible bond prices, but falling prices can also push convertible issuers under water as they can no longer redeem equities instead of paying back the principal.

Our analysis underscores the importance of understanding and assessing the exposures to various sources of risk and return when choosing between different types of convertible bonds. Using appropriate modelling tools could assist the decision-making process.

The author thanks Andy Sparks and Thomas Verbraken for their contributions to this post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1 Based on iShares ICVT ETF (constituent data from CAPCO, prices from Reuters).2 Bond-like convertible bonds are those whose delta to equities is lower than 33%, balanced convertible bonds have a delta between 33% and 66%, convertible bonds with a delta higher than 66% are considered equity-like.3 Based on iShares HYG ETF (constituent data from CAPCO, prices from Reuters).

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.