Is Real-Estate Bond-Like?

Blog post

June 16, 2015

Many institutional investors have been favoring private real estate over bonds, drawn by its steady income stream and higher yields. While the short-term income may be bond-like, the long-run behavior of the asset class is much more cyclical and growth-sensitive.

In the short term, real estate's stable income flows and the lags in adjusting appraisals to the market can give the impression of bond-like behavior. But this impression is misleading, with implications both for asset allocation decisions and risk management.

Comprehensive IPD data and new analytic tools in the Barra Private Real Estate Model and the MSCI Macroeconomic Model shed light on the reality of real estate's performance. By using new desmoothing techniques to identify the relationships between valuations and macro-economic variables, MSCI research uncovers the true importance of the factors driving real estate returns.

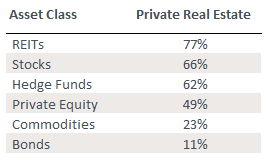

Our research shows that the long-run behavior of real estate lies between that of bonds and equity, but leans much closer to equity than many investors may realize. This behavior can be seen in the long-run correlations of real estate with other asset classes. Private Real Estate does not behave like an uncorrelated "Alternative," nor as a counter-cyclical bond. Rather, it shows a strong cyclical relationship with other risky asset classes.

Long-Run Correlations

Source: The Barra Private Real Estate Model

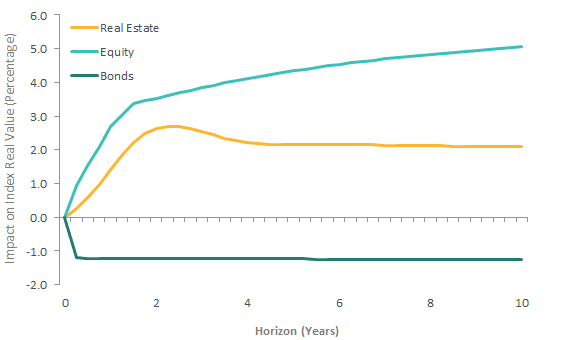

The MSCI Macroeconomic Model provides another perspective, with similar conclusions, by looking at how real estate is expected to respond to a sudden boost in economic growth. Real estate, like equity, benefits from the unlimited upside of greater cash flows associated with higher economic growth, while bonds suffer due to the negative impacts of higher discount and inflation rates. This sensitivity of real estate performance to growth makes it a significant source of systematic risk, rather than the diversification source assumed in many asset allocation decisions.

Impact of a positive 1% shock to real GDP growth, U.S.

Source: The MSCI Macroeconomic Model

Although it may not be the free lunch some would hope for, private real estate generates a liquidity premium in most markets around the world, and inefficiencies in international markets still leave large opportunities for diversification globally. In many ways, these markets are reminiscent of global public equity markets three or four decades ago.

Central bank policies have created a bond market environment in which many investors are exploring higher yields and inflation protection in other asset classes, particularly in private real estate. It is important for investors to be aware that the cyclical, growth-sensitive nature of the capital component of real estate dominates the more bond-like, short-term risks in the lease

Read the paper, "Is Real Estate Bond-Like?."

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.