Latin American Equity Markets: The Lay of the Land

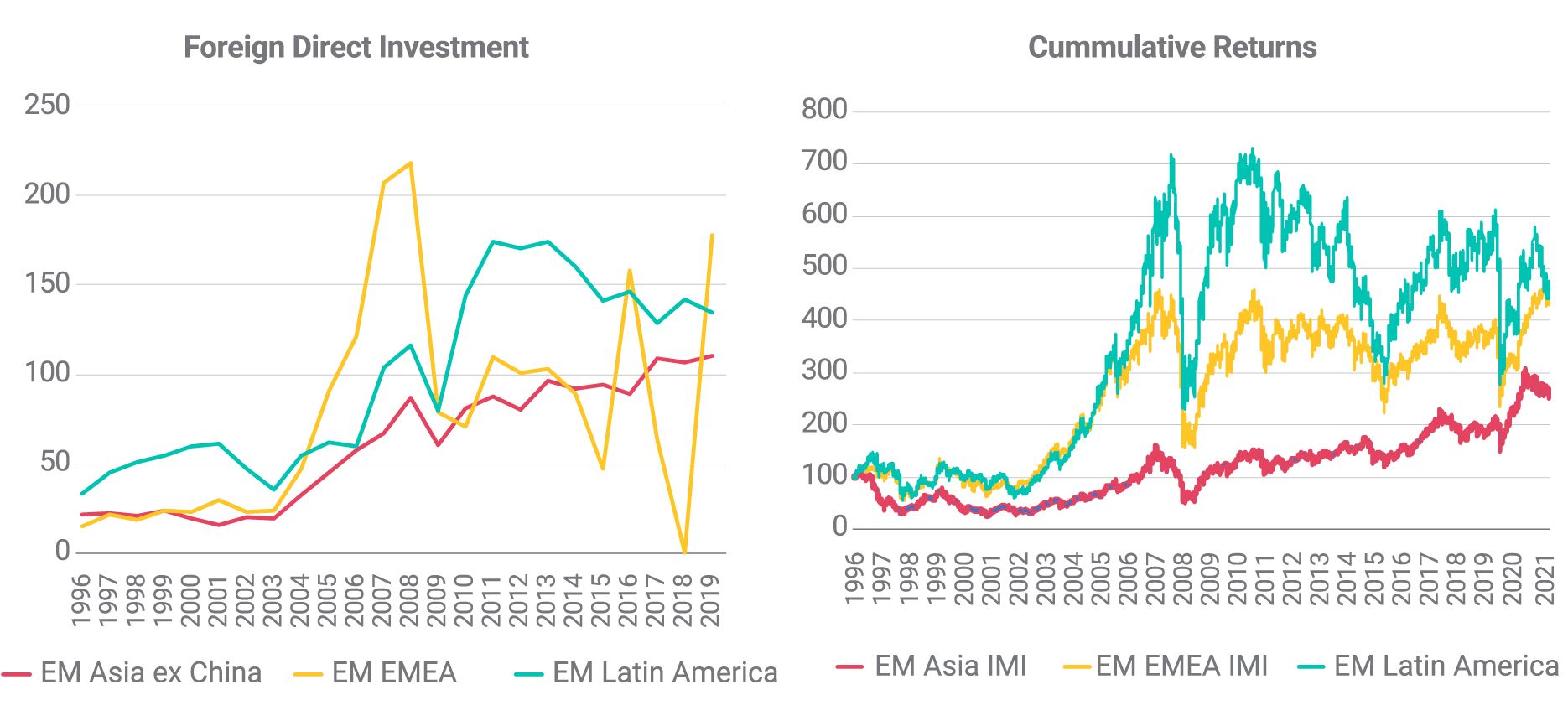

- Over the past 20 years, Latin America attracted more foreign direct investment than other emerging markets such as EMEA and Asia ex China. This has helped expand the middle class and nearly halve poverty over that period.

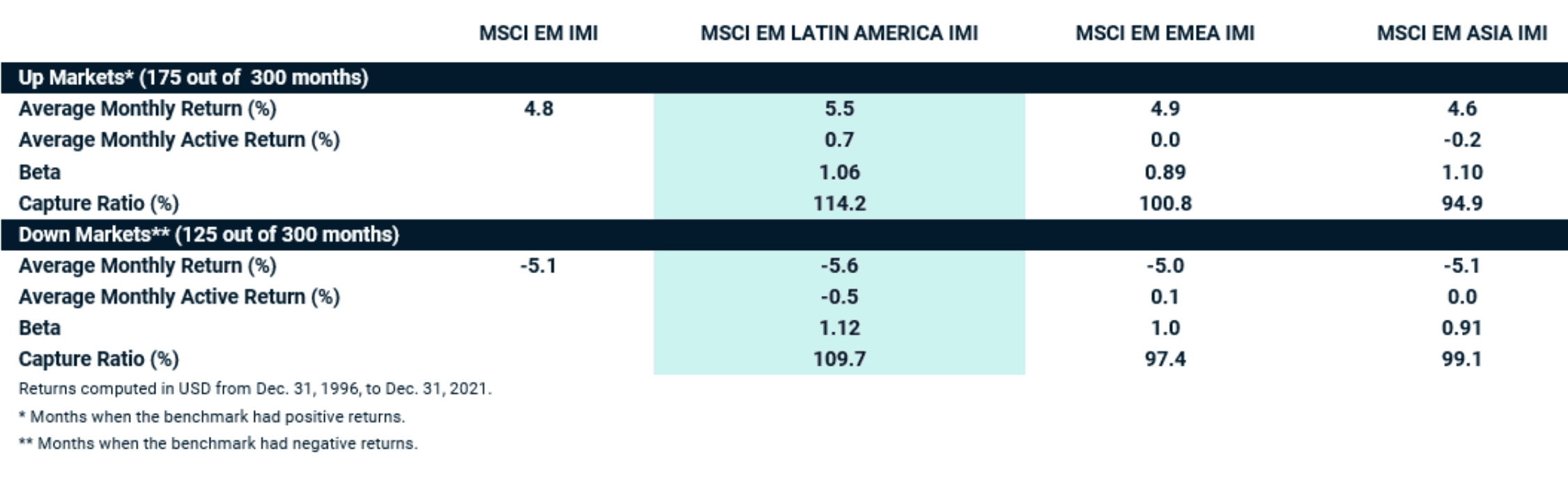

- While Latin America has been more volatile than other emerging markets, the region has, on average, outperformed other EMs during growth periods and recovered faster following economic distress.

- The region has the highest exposure to the efficient-energy theme and the highest average percentage of ESG leaders among emerging-market regions.

Latin American stock markets have recovered strongly as the world started to overcome some of the COVID-19 pandemic's challenges. We take a closer look at the region and its unique profile, including: the influence of foreign direct investment; market performance; exposure to sectors and thematic investments; and companies' ESG and climate risks and opportunities and corporate-ownership structures — relative to other emerging markets (EM).

International investors have helped fuel growth

Over the past 20 years, Latin America has steadily become a favored destination in terms of foreign direct investment, compared to other emerging-market regions such as EM EMEA and EM Asia ex China. Foreign direct investment has been a catalyst to development, income and employment growth in the region over the period, though pandemic-driven closures and a slowdown in activity have had a negative impact on the most recent measurements. From a stock-market perspective, the MSCI EM Latin America Investable Market Index (IMI), which covers large-, mid- and small-cap stocks, showed the highest average annualized returns among emerging markets during this period.

The region also has seen improvements in access to technology, education and literacy and become more integrated in global trade. Over the last two decades, the middle class has expanded and the number of people living in poverty in the region has fallen by nearly half. In addition to these structural changes, there is a cyclical story linked to the recovery of the commodity cycle and its potentially positive impact on local economic growth.

Foreign direct investment and performance across EM regions

Foreign direct investment from 1996 to 2020 in USD billions. Source: World Bank

Markets have been volatile but recovered rapidly

Latin American markets have historically been more resilient during periods of financial distress, such as the 2008 global financial crisis. While it took around 11 months for emerging-market regions in Asia and Europe, the Middle East and Africa to recover from that sudden market drawdown, Latin America recovered in just six months.1 A similar situation occurred during the early stages of the COVID-19 pandemic, when Latin America showed a higher drawdown than other EM regions, but had a steeper recovery, even if it lost some steam recently.

On the other hand, Latin America's performance has been more volatile than that of other EM regions, in absolute and relative terms. Its beta has been, on average, greater than 1 for the last 20 years, which means it has tended to move down — and up — at greater levels than the broader market. During the last 20 years, the MSCI EM Latin America Investable Market Index (IMI) has, on average, outperformed other EM regions during "up" markets, which has helped its overall performance over that period, as shown in the exhibit below.

Latin America vs. other emerging markets

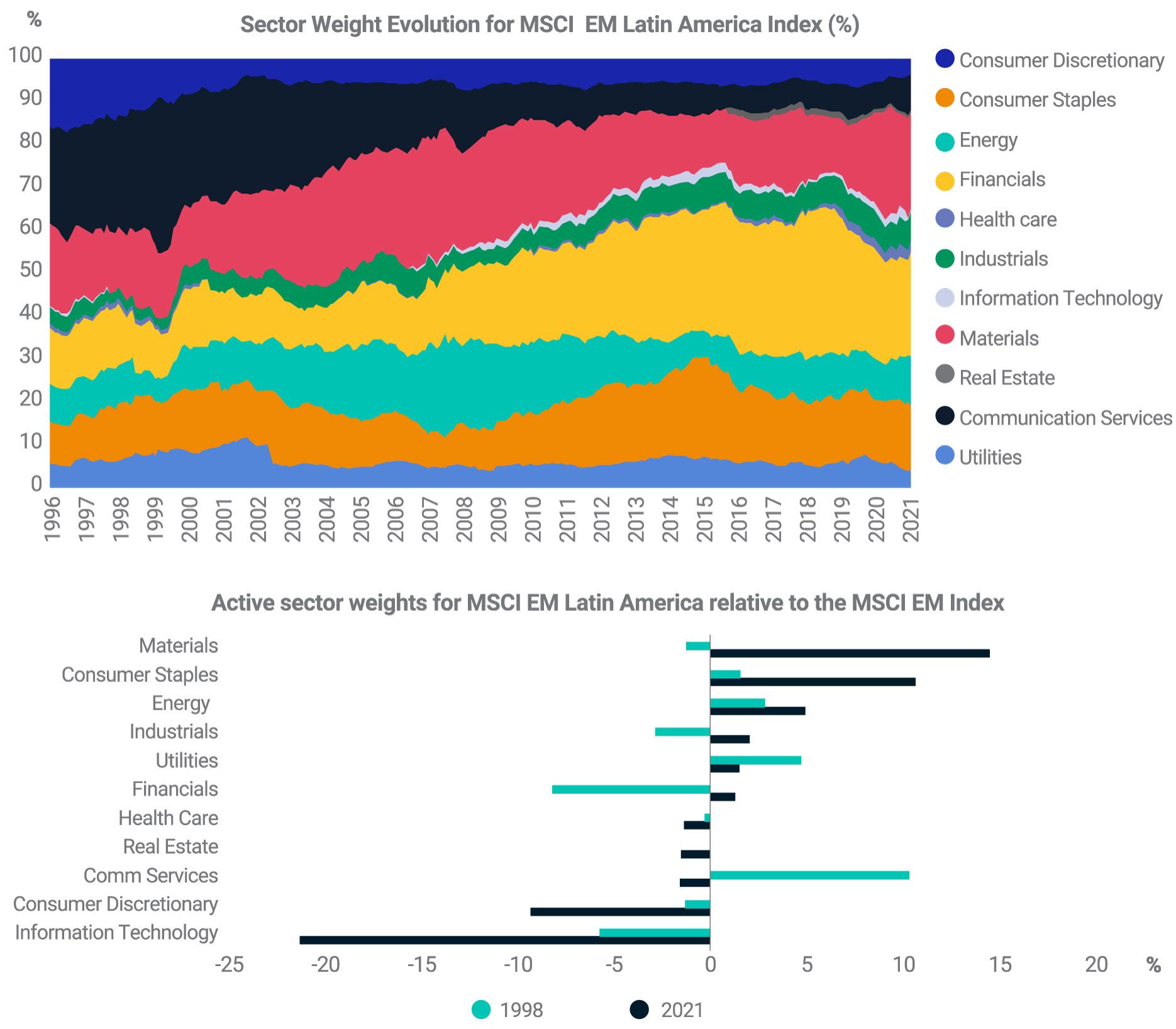

Sectors remained a driving force

Latin America's economic drivers have significantly changed over the past two decades, as we can see clearly by looking at the sector composition of the region's stock market: Materials, financials and consumer staples, the three top-performing sectors since December 1998, have grown in prominence over the last 20 years, largely at the expense of communication services, as the exhibit below shows.

The proportion of sectors also varied in the region, compared to the other EMs. Latin America's economies had greater representation in materials, consumer staples and industrials, and less in information technology (IT), consumer discretionary and real estate. In the overall MSCI Emerging Markets Index, the largest sectors were IT (driven by EM Asian companies), financials (driven by EM EMEA companies) and consumer discretionary (driven by EM Asian companies), exhibiting a procyclical profile.

EM Latin America sector weights

Thematic, ESG and climate lenses can provide clarity

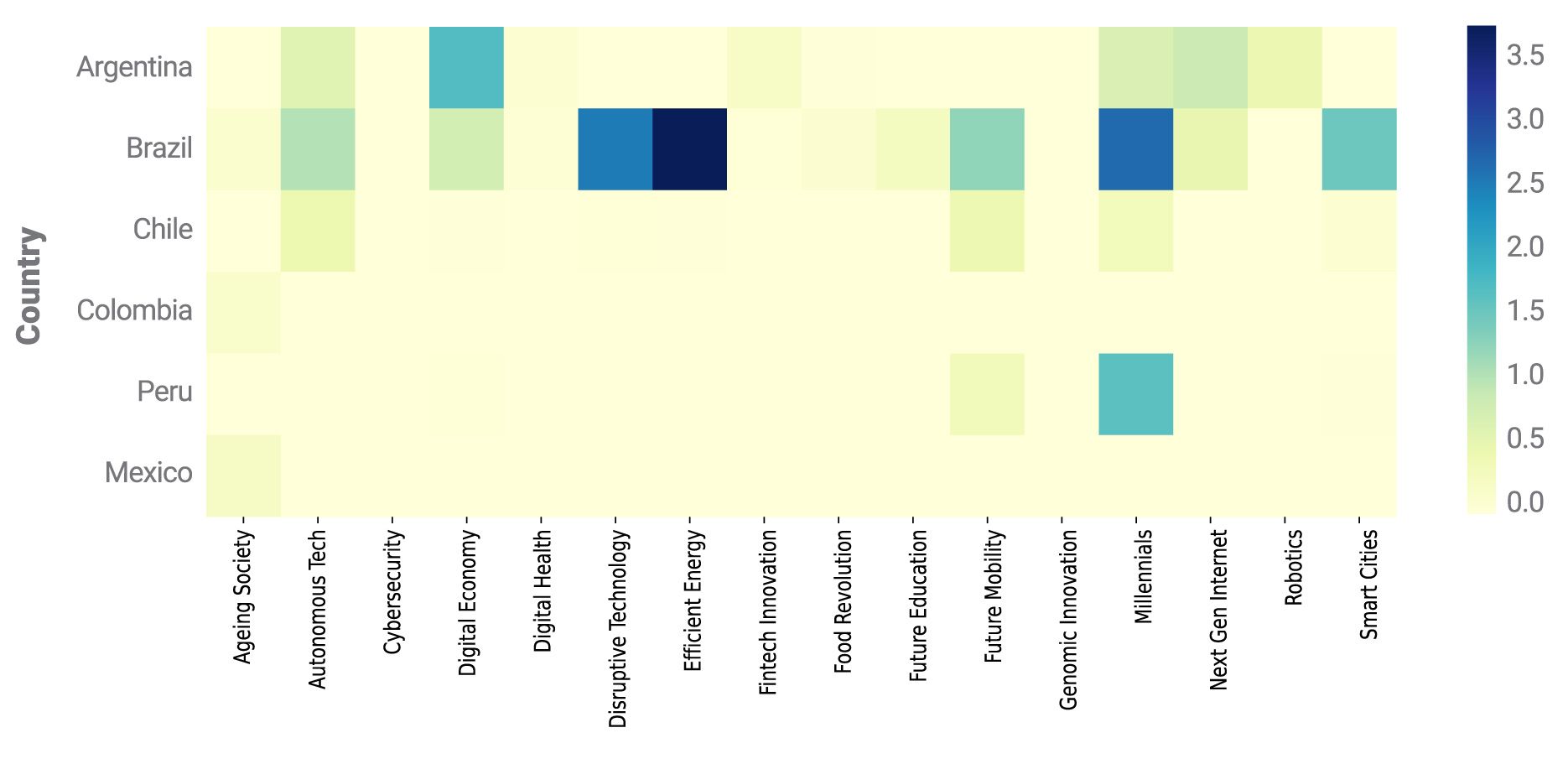

The MSCI EM Latin America IMI had the greatest exposure to the efficient-energy theme among EM regions, as of Nov. 30, 2021.2 High exposure to this theme is linked to the development of renewable energy and the circular economy, which may be of interest when considering exposure to companies with low-carbon-solutions technology.

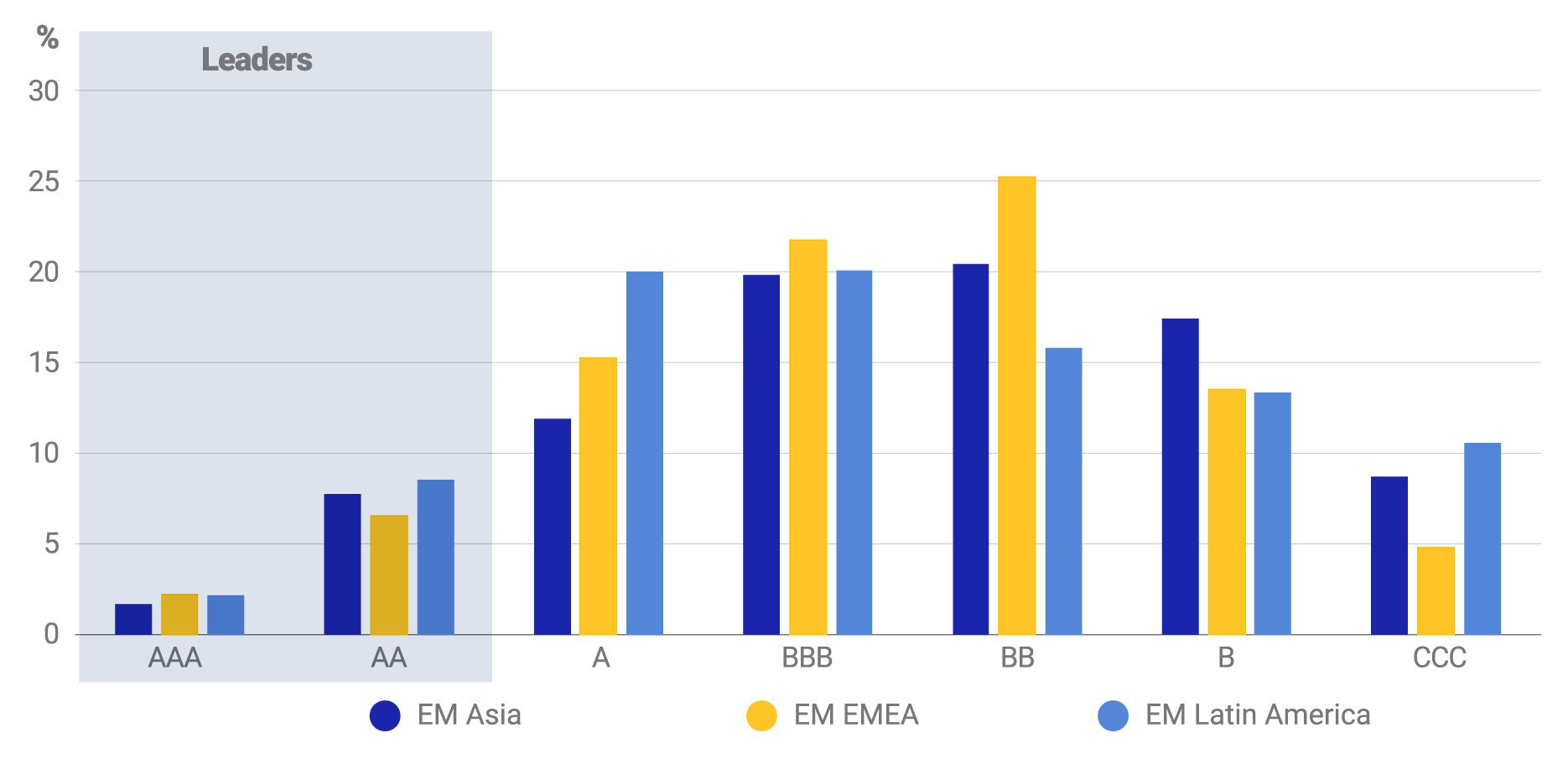

Among EM regions, Latin America has also shown a differentiated ESG profile. Historically, it has been the region with the highest average percentage of ESG leaders3 (11%) and the lowest percentage of companies with negatively trending ESG scores. Additionally, Latin America had the lowest carbon intensity for EM, as measured by tons of CO2 emissions and CO2 equivalent emissions, per USD 1 million in sales.

Thematic exposure of EM Latin America IMI

Thematic exposure of the MSCI EM Latin America IMI, as of Nov. 30, 2021.

Average MSCI ESG Ratings distribution for EM regions

Data from January 2010 to November 2021

Who owns LATAM, and how do they own it?

Better understanding a firm's ownership structure4can help investors assess how loud their voices will be when the firm's strategy and direction are being decided. Latin America has a different concentration of ownership groups compared with other emerging markets, especially considering the influence of controlled state-owned enterprises (SOEs) in other regions. Additionally, among MSCI ESG Rating leaders, Latin America has the highest weight by market cap in "Other Controlled" companies (11%).5 Prior research has shown that a lower proportion of SOEs may lead to improved governance, as companies have tended to exercise greater independence from government intervention.6

Ownership groups among EM regions

Investing in Latin America

According to data provider CB Insights, "over USD 20 billion of venture capital went into 952 deals in Latin America in 2021, nearly four times as much as in 2019. The region is catching up from a low base, and quickly: investment since 2015 has grown over ten-fold, speedier than in Asia, Europe or the United States." 7 Understanding the region, and how it has differed from other emerging markets, can help investors make more informed decisions.

1 The volatility of the MSCI EM Latin America IMI has been diverging from the rest of the MSCI EM IMI regions since 2014 (considering a 48 month-rolling window).>

Thematic investing is a top-down investment approach which seeks to capitalize on potential opportunities created by major trends that are structural and transformative in nature, rather than short-term shifts. Thematic-relevance scores derive from how much of a company's revenue comes from products or services related to a particular theme. The scores are an alternative to ESG, sector and factor metrics and allow investors to understand the economic linkage to long-term structural thematic trends and analyze the market beyond country or regional exposures.

MSCI ESG Ratings provides research, analysis, and ratings of how well companies manage environmental, social and governance risks and opportunities. MSCI ESG Ratings provides an overall company ESG rating — a seven point scale from "AAA" to "CCC." In addition, the product provides scores and percentiles indicating how well a company manages each key issue relative to industry peers.

To help investors assess that potential impact, MSCI ESG Research LLC developed an ownership-group classification framework. This classification rests on two dimensions. 1. Owner classification, or which group, if any, has effective control (largest percentage of voting rights)? It covers three categories: controlling (>=30% of voting rights), principal (=<10 – 30% voting rights) and widely held (no shareholder has more than 10% of voting rights). 2. Owner type, or who is the dominant owner (founder, family, state and other)? The two dimensions combined describe the ownership structure and level of control for each group. For example, if a company is classified as controlled by a state-owned enterprise, the state holds at least 30% of the voting rights, while if a company is classified as "SOE principal," the state holds between 10% and 30% of the voting rights.

"Other Controlled" companies include a wide range of controlling investor groups, but exclude founder firms, family firms and SOEs. For Latin America within this group, some companies are from the steel industry (19%), diversified banks (18%), hypermarkets and super centers (17%) and brewers (11%).

Wang, Yan, and Xu, Xiaonian. "Ownership Structure, Corporate Governance, and Corporate Performance: The Case of Chinese Stock Companies." World Bank Group, May 1997.

"The pandemic has accelerated Latin America's startup boom." The Economist, Jan. 15, 2022.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.