Leveraged loans: Risks, rewards and investor protections

Blog post

January 11, 2018

"In rising financial markets, the world is forever new. The bull or optimist has no eyes for past or present, but only for the future…" –James Buchan, The Guardian

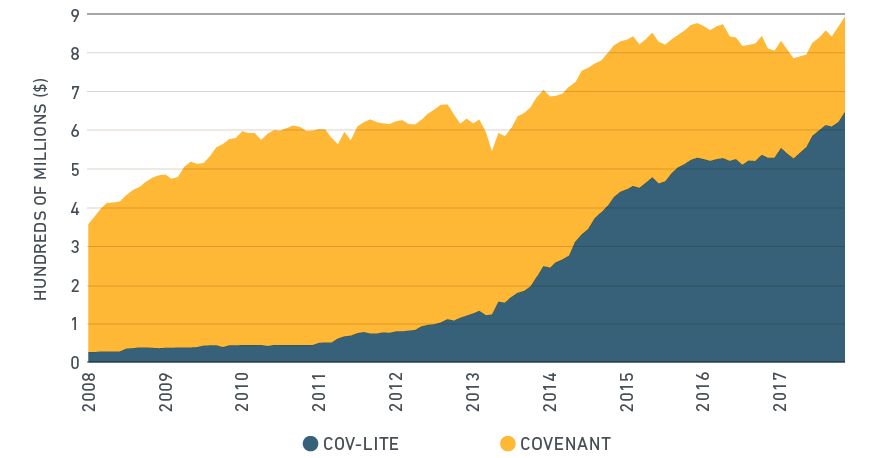

As central banks continue to keep interest rates at historic lows, many institutional investors have turned to leveraged loans1 for their attractive yields. These floating-rate instruments also may provide a valuable hedge as interest rates rise. While the leveraged loan market has now surpassed $1 trillion,2 protection for investors is declining as companies have increasingly issued so-called "covenant-lite" loans. With prices high and spreads low for these loans, is the market adequately compensating investors for the risks they are taking? Investors need to closely examine the trade-offs embedded in the current market environment.

Loan investors have traditionally required borrowers to meet strict numerical targets on financial health, known as covenants. For example, a covenant could limit the issuer's leverage to some multiple of its free cash flow. Failure to abide by a covenant may require an issuer to compensate investors, for instance by providing additional collateral, higher coupons or one-time fees. By requiring issuers to maintain these covenants, investors can directly affect issuers' default probabilities. But as investor appetite for leveraged loans (also known as syndicated bank loans) has increased, many issuers have turned to less restrictive covenant-lite (cov-lite) loans, which offer investors less downside protection.

Covenant vs. cov-lite index constituents over time

Source: IHS Markit

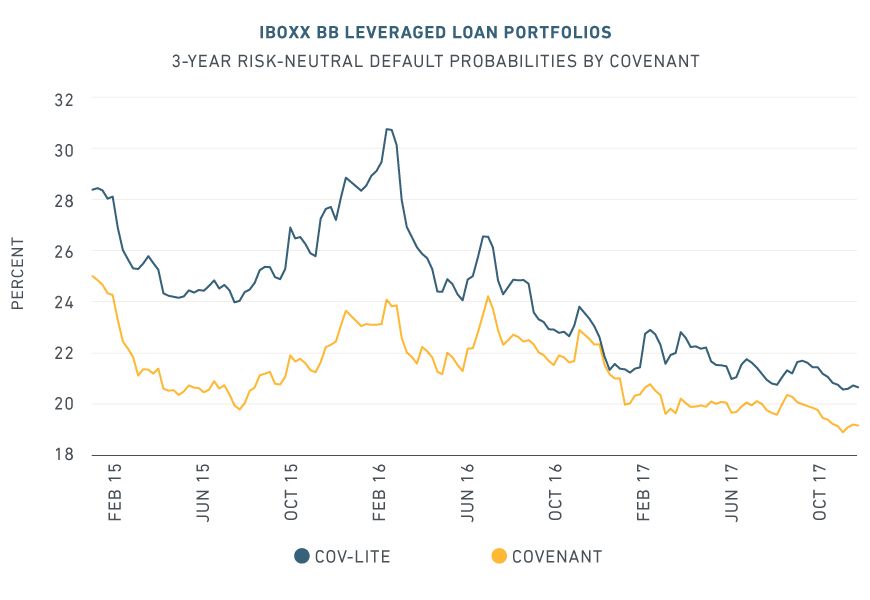

Based on the MSCI Syndicated Loan Model (powered by loan data from IHS Markit), we can compare default risks for cov-lite and covenant loans and draw insights on how the changing nature of the loan market may affect investors. The exhibit below illustrates the different reaction of covenant and cov-lite assets during periods of market turbulence. We created sample portfolios using the BB segment of the IBOXX Leveraged Loan Index, with similar size, sector and covenant strength dimensions. While the entire loan market was affected by the energy crisis of late 2015 and early 2016, the cov-lite sample portfolio's (risk-neutral3) probability of default rose much more dramatically than its covenanted counterpart. The figure shows that even though covenants were not a risk factor in normal times, potential losses have been more severe for cov-lite loans during adverse financial conditions.

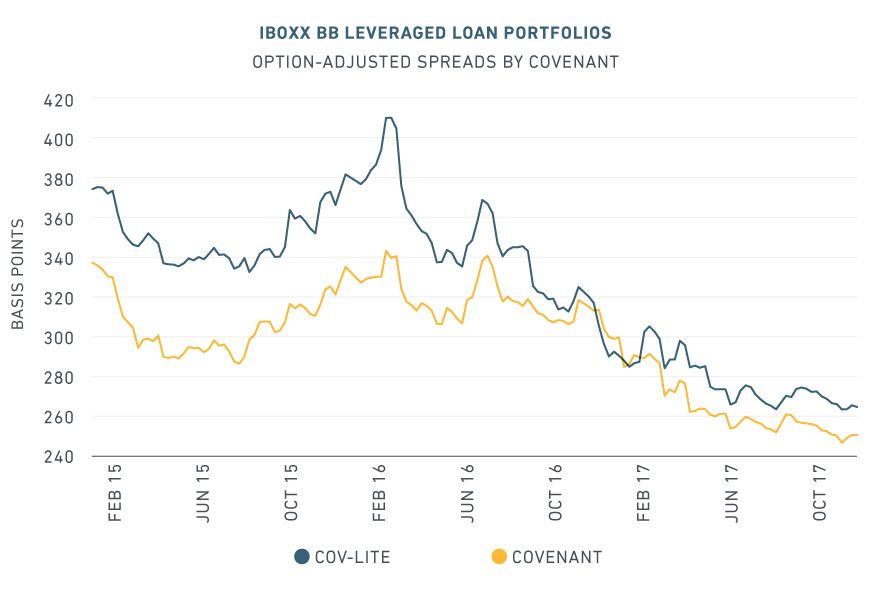

Default risks and compensation for BB leveraged loan portfolios

Source: IHS Markit. Analytics are aggregated by market value and spread duration. OAS is adjusted for both prepayment and default

The right panel above shows the extra compensation investors have received for holding cov-lite rather than covenant loans. The spread widened rapidly during the energy crisis and then steadily declined once it had passed. There are, of course, many reasons why leveraged loans have experienced impressive growth and returns since the financial crisis. But given their current valuations, investors must weigh the benefits of cov-lite loans against the compensation they are receiving for their more mercurial risks.

1 We can broadly define leveraged loans as syndicated commercial loans priced at a spread to LIBOR of at least 125 basis points.

Further reading:

The search for yield: Leveraged loans vs. high-yield bonds as interest rates rise

Leveraged Loans (Client access only)

Subscribe todayto have insights delivered to your inbox.

2 As of August 2017. Source: IHS Markit3 Risk-neutral probabilities are derived from the model, and do not reflect historical probabilities.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.