Listed and Private Real Estate: Putting the Pieces Back Together

Blog post

April 19, 2017

A property owned by a listed real estate company, such as a Real Estate Investment Trust (REIT) or a real estate management and development company, should produce returns close to those of an equivalent asset that is privately owned. In reality, however, the results differ, especially when looking at short-term performance. The challenge for real estate investors is to be able to use both listed and direct real estate in their real estate allocations and understand the performance drivers for each. Specifically, how do equity market factors, financial structures and individual properties contribute to performance?

Previous studies have used market index series, which permitted only imprecise analysis due to their varying constituents. In our new paper, reporting research undertaken in association with the European Public Real Estate Association, we compared corresponding market indexes as well as precisely matched samples from 19 European listed real estate companies with long-term returns at the asset level. This detailed dataset enables us to make an apples-to-apples comparison within and across asset, vehicle and security levels, using custom indexes or composites.

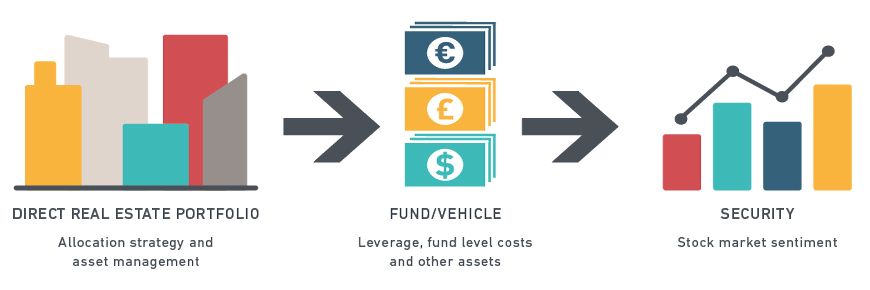

The three performance levels of real estate companies

This more granular analysis showed that asset, vehicle and security levels are not as different as they might superficially appear, suggesting that asset owners may be able to combine the three in their total real estate portfolios, provided they conduct the proper performance reconciliation and attribution analyses. We found:

1. High correlations existed across levels. Among the selected 19 companies, there were strong correlations across asset, vehicle and security levels, particularly over longer periods, suggesting that listed real estate companies may be used as components of overall real estate portfolio strategies.

2. Assets drove performance. When aggregated to a single composite, there remained a close fit between security- and asset-level results, particularly for Europe ex U.K. companies. Asset-level returns clearly were the main driver of overall equity performance in the long term. However, vehicle/financial factors also influenced returns, especially in phases of weak or strong overall equity returns. Over short time periods, stock market sentiment had a hefty impact on return volatility.

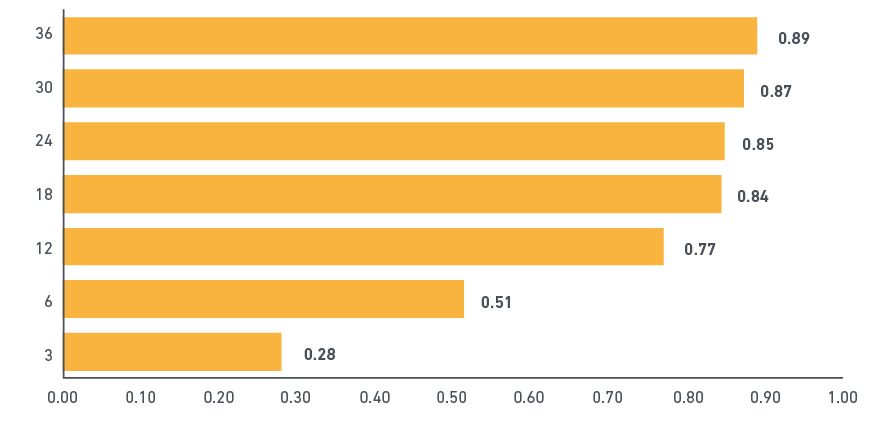

3. Index returns aligned. At the highest level of aggregation, asset, vehicle and equity headline index performance trends all appeared broadly synchronised over the longer term, at least to the extent that their overall cyclical patterns largely matched one another, but diverged in periods up to around 18 months (see below exhibit). The relationship was even stronger for U.K. companies than for their continental European counterparts.

Asset vs equity level index correlations over periods from 3-36 months

MSCI Europe ex UK IMI Core Equity RE vs IPD Europe ex UK Direct RE (quarterly returns)

The author thanks Ian Cullen for his contribution to this post.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.