Managing Fixed-Income Risk in Turbulent Times

Blog post

June 7, 2017

Fixed-income markets have weathered a series of financial crises since 2008, forcing institutional investors to discard old assumptions and seek a risk management framework suited to the new, ever changing environment.

The rapid onset of crises highlighted the need to better understand credit risk without relying on credit ratings, which were slow to anticipate changing market conditions. And it was just as important to recognize the end of one crisis to see the warning signs of the next event. The early signals of the 2011 euro crisis could have been missed against the backdrop of the extreme events of 2008, but stood out against the calm that had returned in late 2009, for example.

These changes suggest a need for an updated approach to modeling fixed income. New risk factors may be needed to recognize the decoupling of old relationships, new risk exposures may be needed to signal changing market regimes, and new connections may be needed between risk and portfolio management:

- Credit: Market turbulence could require a view of risk that supplements backward-looking volatility with forward-looking indicators to recognize transitions between risk regimes.

- Rates: Quantitative easing and negative interest rates have fundamentally changed interest-rate dynamics. Rather than assume the term structure of traditional interest-rate models, investors may increasingly see a need to manage exposures to each key rate individually.

- Basis risk: Drops in dealer inventories have increased illiquidity and driven a wedge between closely related securities – such as cash bonds and credit default swaps, or on- and off-the-run Treasurys. Tools to manage basis risk are likely needed to prepare for the further breakdown of the theoretical ties between these assets during times of market stress.

- Risk management practices: Policy and regulatory changes have placed risk management front and center in the investment process.

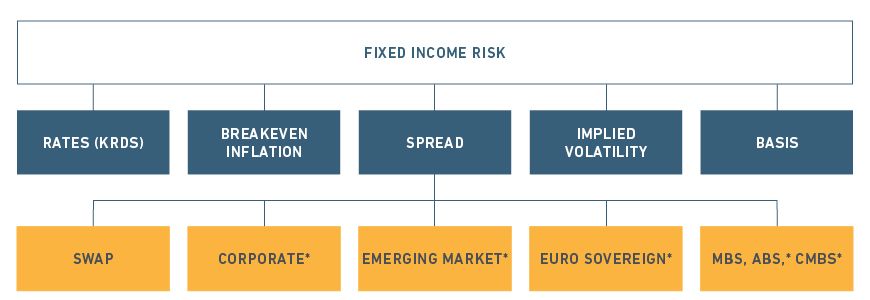

MSCI's fixed-income risk framework

Fixed-income risk is decomposed among various classes of factors. The spread factors denoted (*) use duration times spread (DTS) exposures. Currency, equity, commodity and private asset factors are also modeled but not shown here.

Further reading:

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.