Managing MBS risk in a rising rate environment (Part 1)

Blog post

September 17, 2018

This blog is the first of two blogs published by Yihai Yu discussing the risk implications for MBS investors in the context of the prevailing interest rate environment.

Bond investors lost $1 trillion during "the great bond massacre"1 of 1994, which was triggered by the Federal Reserve's aggressive tightening of interest rates. Many U.S. mortgage-backed securities (MBS) investors and broker-dealers misjudged the risk that fixed-rate prime mortgage borrowers would defer prepayments due to market conditions. This risk — known as "extension risk" — means that borrowers may hold onto mortgages longer than previously expected.

While the current MBS sell-off has not experienced the same rapid pace as in 1994, the majority of the agency MBS universe effectively cannot be refinanced,2 as mortgage rates have risen to 4.6% from 3.5% in October 2017. In this environment, it may be worthwhile for investors to assess their current MBS risk exposure.

WHAT IF RATES CONTINUE TO CLIMB?

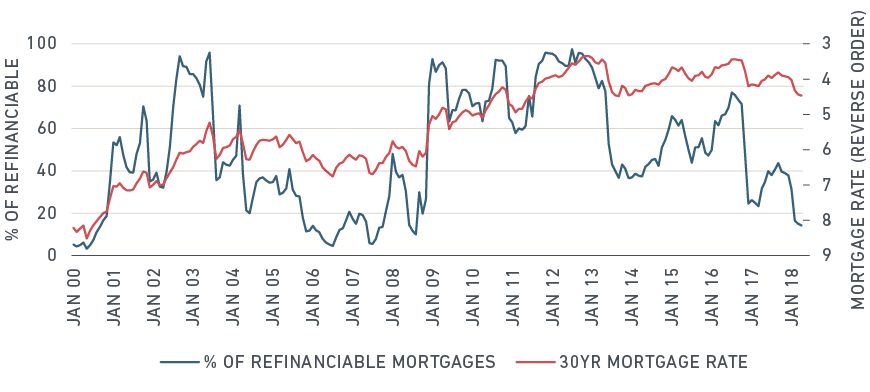

This is the first MBS environment where most homeowners lack tangible refinance incentives since the 2008 global financial crisis (see exhibit below). If mortgage rates increase further, decreasing prepayment speeds (the rate of prepayment of mortgage loans) could significantly extend MBS durations.

Fewer homeowners have an incentive to prepay their mortgages

Source: Fannie Mae, Freddie Mac, MSCI

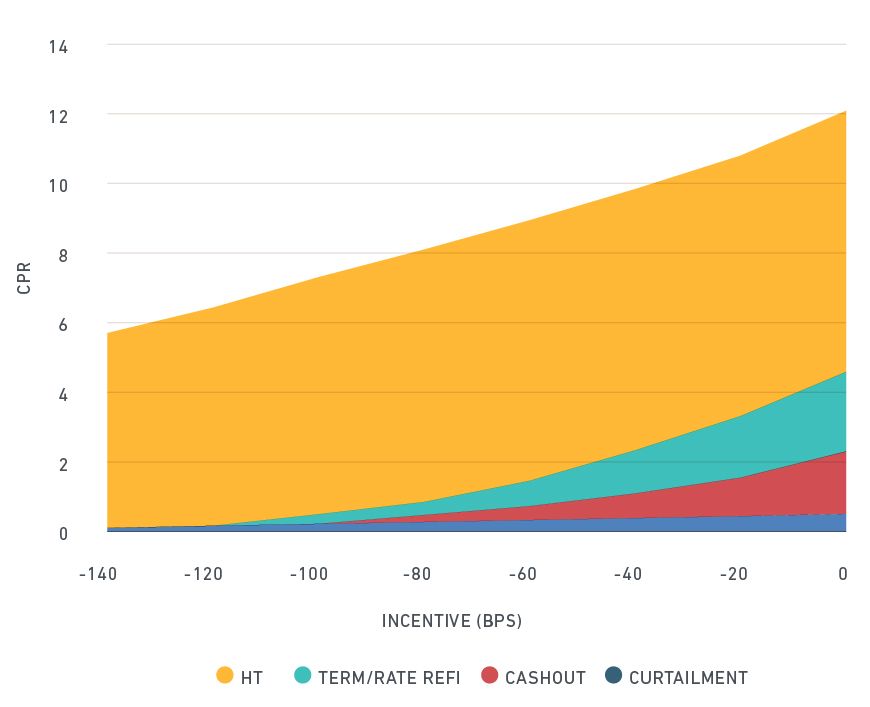

The following exhibit shows the composition of the current base prepayment speeds across different rate incentives, based on the new MSCI prepayment model.3 Overall, the total base prepayment speed, in units of Conditional Prepayment Rate (CPR), is projected to drop from 12 CPR (at-the-money) to 6.4 CPR (120 bps out-of-the-money). According to the model, cash-outs (allowing borrowers to convert home equity into cash) and rate/term refinance may decline quickly as rates rise, while housing turnover may stay relatively stable for mild rate rises and may start to slow down when the disincentive becomes significant. Curtailment is a relatively small and stable component, showing a moderate lock-in effect.

Prepayment speed may drop as rates rise

Source: MSCI Agency Prepayment Model

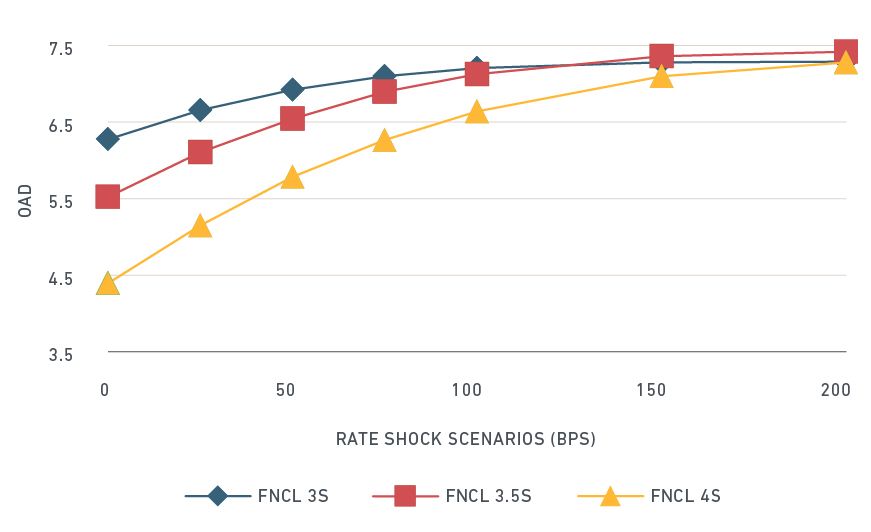

In a MBS sell-off, the risk of duration extension is most pronounced in the first 25 bps rise in interest rates, especially for securities whose coupon is close to market rates, as the very rate-sensitive components of the base speeds (cash-out, rate/term refinance) retreat. As the sell-off deepens, our model shows that duration may continue to extend, although at a slower pace, due to the gradual flattening of the overall lock-in effect. Under an extreme rising rates scenario, the prepayment variation effect may diminish, leading to the convergence of the durations.

Risk of duration extension is most pronounced when rates first rise

Source: MSCI Agency Prepayment Model. FNCL refers to Fannie Mae 30-year TBA

In short, the risk of rising interest has potentially dramatic implications for all investors. MBS investors, however, may need to be aware of the risk of the duration of their securities extending as homeowners slow down mortgage prepayments. Modeling these risks may help investors better understand these risks.

Further Reading

Managing MBS risk in a rising rate environment (Part 2)

MSCI Agency Fixed Rate Base Prepayment Model (Available on the client site only - login required)

As credit risk rises, beware of selection bias in CLOs

Getting Ahead of the curve: How Taper 2.0 May affect Bond returns

Subscribe todayto have insights delivered to your inbox.

1 Ehrbar, A. (Republished 2013). “The great bond massacre.” Fortune.2 The prevailing rate needs to be roughly 40 basis points (bp) lower than existing mortgage’s rate for the homeowner to gain a tangible economic benefit.3 Yu, Y. (2018). “MSCI Agency Fixed Rate Base Prepayment Model.” MSCI Model Insight (client access only)

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.