Managing Risk Over Different Investment Horizons

Blog post

September 25, 2018

Given high market valuations, some investors worry that a market pullback may be at hand. We saw markets gyrate earlier this year — what if volatility returns? How investors respond to changing market conditions may depend on their time horizons.

From February 2 to April 6, the U.S. equity market experienced some large daily swings, causing anxiety among many investors.1 We list the eight days within 2018 where the absolute returns of the MSCI USA IMI exceeded 2%. All but one of these days had a negative return. In contrast, all of 2017 did not experience a single day with an absolute return above 2%.

Days in 2018 with MSCI USA IMI absolute returns above 2%

Date | MSCI USA IMI Return |

|---|---|

Date Feb 02, 2018 | MSCI USA IMI Return -2.07% |

Date Feb 05, 2018 | MSCI USA IMI Return -3.98% |

Date Feb 08, 2018 | MSCI USA IMI Return -3.65% |

Date Mar 22, 2018 | MSCI USA IMI Return -2.48% |

Date Mar 23, 2018 | MSCI USA IMI Return -2.07% |

Date Mar 26, 2018 | MSCI USA IMI Return 2.63% |

Date Apr 02, 2018 | MSCI USA IMI Return -2.24% |

Date Apr 06, 2018 | MSCI USA IMI Return -2.13% |

The drops, however, turned out to be short-lived. The market has since recovered and resumed its upward trend, and has reached an all-time high recently. However, many investors have commented that we are late in the market expansion cycle and may see stock prices decline sooner or later.2

HISTORICAL SHORT- VS. LONG-TERM RISKS

Since January 2015, the U.S. stock market has climbed fairly steadily, with some noticeable exceptions, as we can see in the exhibit below for the MSCI USA IMI. Thus, long-term investors have benefitted from staying the course.

Since 2015, the U.S. stock market has generally been moving up

Source: MSCI USA IMI, gross returns

Now, let's compare the extreme returns from February to April to the January 2015 to July 2018 period, together with the forecast volatilities for this index given by MSCI's Barra® US Total Market Trading and Stable models.

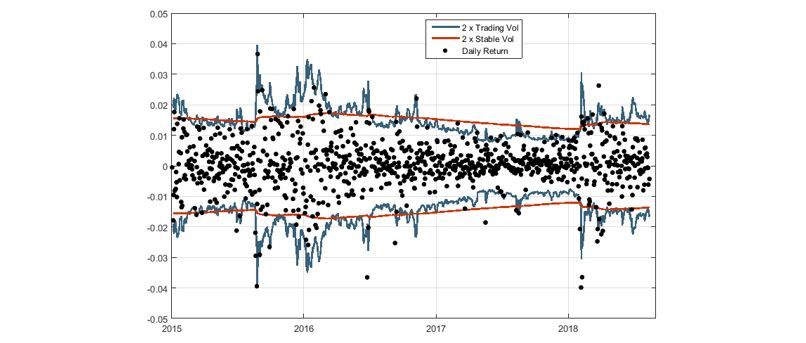

SHORT-TERM RETURNS AND VOLATILITIES

In the below exhibit, the dots represent the daily returns and the lines represent plus/minus two times the forecast volatilities given by the models – we call these lines the two-sigma lines. They allow us to visually identify outlier returns.

We have two observations:

- The Trading Model responded immediately to large returns by raising its volatility forecast from 0.56% on Feb. 1 to 1.53% on Feb. 5. In contrast, the Stable Model responded much more gradually, from 0.60% to 0.65%. This difference is understandable, because the Trading forecast is mainly based on recent returns, thus a new daily return carried a large weight. The Stable forecast, on the other hand, is formed from returns from a much wider window, thus it cannot be changed dramatically by a single return.

- The increased responsiveness of the volatility forecast helped to reduce the number of daily returns outside the two-sigma lines. In 2018, there were 12 outlier returns with respect to the Trading volatility forecast, while the Stable volatility forecast resulted in 17 outliers. This more responsive forecast exhibited superior performance when used for risk control on the daily horizon.

MSCI USA IMI daily returns and forecast volatilities

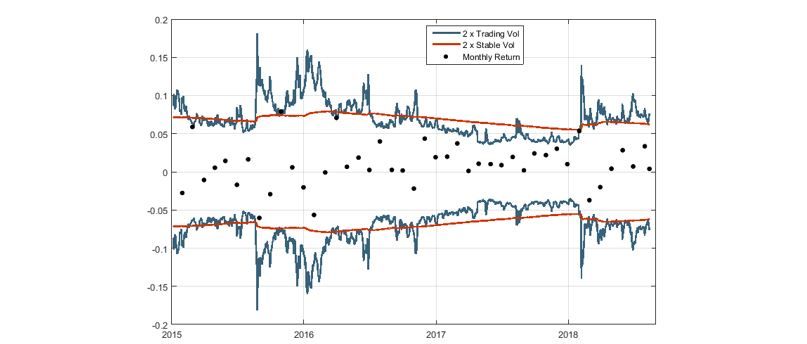

LONG-TERM RETURNS AND VOLATILITIES

We now switch to the monthly view depicted below, where the dots represent the monthly returns of the portfolio, and the two-sigma lines are scaled to the monthly horizon. There are no clear outliers relative to the two-sigma lines given by either model – the worst offenders were several dots riding on the lines. The key takeaway of this example: the long-term manager did not need to adjust the portfolio in response to short-term changes in market volatility.

MSCI USA IMI monthly returns and forecast volatilities

These two exhibits suggest that the hypothetical long-term manager would have been better able to ride out the short-term ups and downs of the market, while the manager with a short-term focus may have sought to react quickly to daily fluctuations.

Thus, a manager might want to consider whether to marry risk forecast with investment horizon. For the manager with a long horizon, the short-term moves of the market tend to even out, thus diminishing the need for the highly responsive volatility forecast that may increase transaction costs. Managers may wish to further examine whether the volatility forecast that is tuned for the monthly or even longer investment horizons is more appropriate for such a use case.

1 For example, see Carew, S. (2018). "Stock sell-off overdue, investors lick their wounds and hunt." Reuters.

2 For example, see Timmer, J. (2018). "Is it getting late for stocks?" Fidelity Viewpoints; Holmes, F., (2018). "Take the long-term view in a late-cycle market." Forbes.

Further Reading

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.