Manhattan Office Redevelopment: Still Stuck on Pricing

- There is talk in the market about converting offices to apartments, but sales for the purpose of redevelopment are still minimal.

- The prices of offices remain too high relative to apartment prices to spur conversions.

- Conversions will depend on regulatory relief or current office owners taking a loss.

Do property owners have enough incentive to redevelop offices?

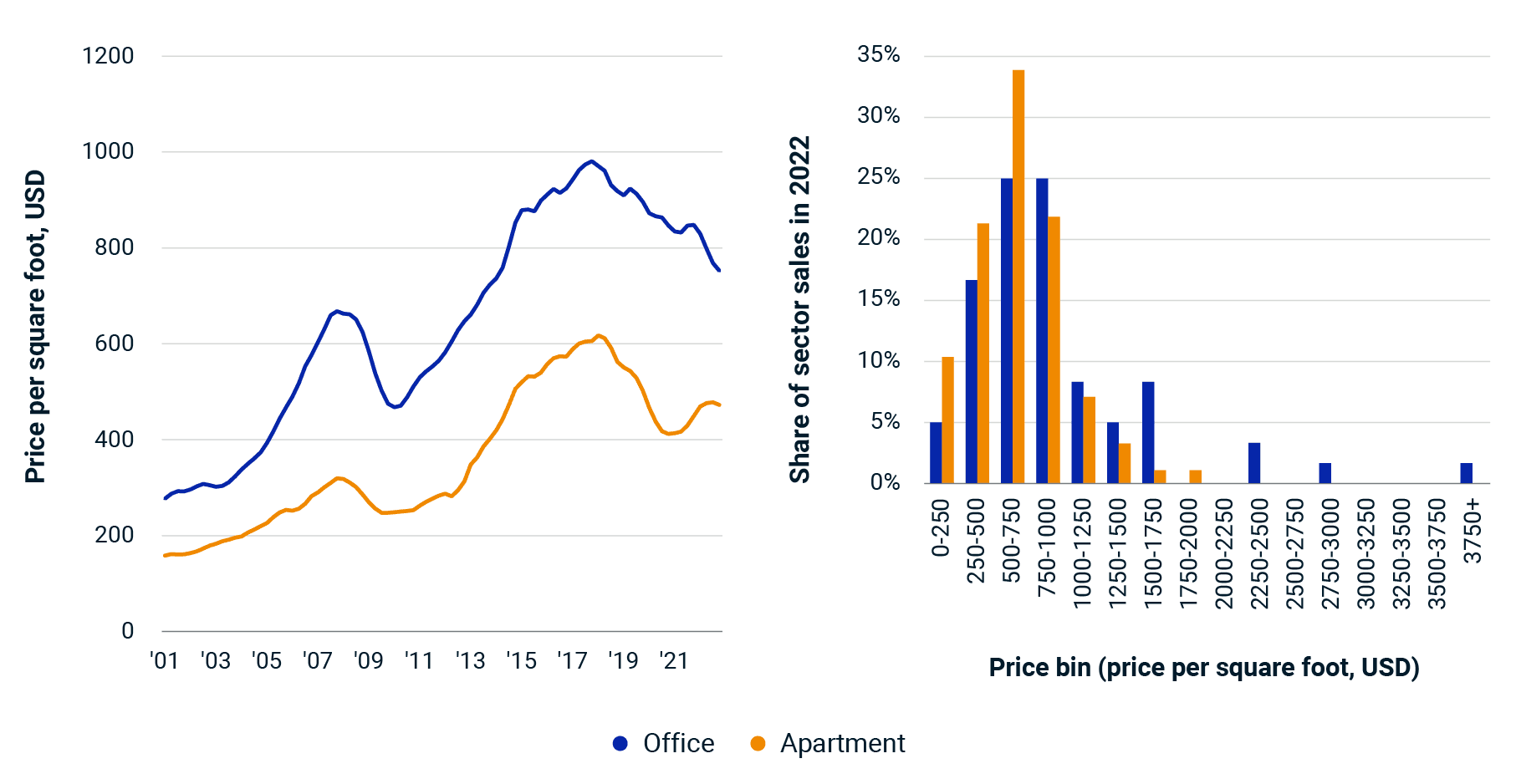

Uncertainty reigns around conversions, but the asset pricing is something we can measure and there is some movement there, providing hope for those who wish to see the city redeveloped. Pricing of Manhattan offices, as shown by the RCA Hedonic Series, has fallen a cumulative 23.3% since the high-water mark in 2017, when a flood of Chinese capital drove expectations for the market higher. Relative to midyear 2019, before the pandemic hit, prices were down 18.5% by year-end 2022. Is that kind of a drop enough to incentivize a developer to undertake the risks of converting a building?

Looking at the equivalent hedonic-price series for apartments and converting the figure to a price-per-square-foot basis, we can clearly still see a wide gap at the market level. Offices were priced 59% higher on a per-square-foot basis for the entire market at the end of 2022. Taking the average office building and investing capital to make it the average apartment building is clearly a money-losing proposition.

Office laggards most likely to convert to apartments

Still, it is not the entire market that will be converted, only the laggards. There is no one price for any piece of real estate. Some buildings will receive a higher price because of characteristics like age and secure tenancies. Others will lag due to those same characteristics. Looking at the distribution of sale prices in the Manhattan office and apartment markets in 2022, there is a wide, non-normal, distribution of sales.

Prices of Manhattan apartment and office buildings don't signal conversions

Source: RCA Hedonic Series

Even at the left-hand tail, the cheaper end of the spectrum, the apartment market is still not priced as aggressively as the office market. For all sales in 2022, 32% of the apartment sales in Manhattan were priced at USD 500 per square foot or less. Only 22% of the office market sold in this price range. For the lowest bracket — assets sold for USD 250 per square foot or lower — 10% of apartment sales were in this range, versus only 5% of office sales.

Looking through sales and refinancings of newly developed apartment buildings in 2022, one might get a sense of what a developer hopes to gain on the sale of an asset. Again, there is variation across the geography of Manhattan, with one project in East Harlem refinancing in May of 2022 at USD 895 per square foot and one in Lower Manhattan in the Financial District sold at USD 1,514 per square foot. But for Manhattan as a whole, the average for apartment assets built over the last five years was roughly USD 1,166 per square foot. With office sales, 23% of the market was priced above USD 1,166 per square foot or greater in 2022. There is not room for profit in redeveloping any of these assets, except perhaps for some smaller buildings, if one can tear a property down and build more density.

What about the other 77% of the office market with sale prices below USD 1,166 per square foot, though? How many of these would be financially viable for conversion? Sadly, there are few consistent measures of replacement costs available.

We do know, however, that New York City is among the top 10 areas of the U.S. with respect to the difficulty of building new housing due to regulatory delays.2 Combine this regulatory burden with the fact that regulation adds 40.6% to the cost of developing new housing,3 plus a modest return-on-cost expectation for the developer, and it is hard to see anything but that far left tail of the office price distribution being suitable for redevelopment in the current market.

A big wave of conversions may be coming, but it will only happen through a significant move in regulatory barriers to construction or from current owners selling buildings at a significant loss.

The author thanks Haley Crimmins and Alexis Maltin for their contributions to this post.

Further Reading

Pricing Barriers Challenge Manhattan Office Repurposing (client access only)

Is Inflation Here to Stay?

Subscribe todayto have insights delivered to your inbox.

1“Mayor Adams Unveils Recommendations to Convert Underused Offices into Homes.” New York City Mayor’s Office, Jan. 9, 2023.2“U.S. Barriers to Apartment Construction Index.” National Apartment Association, 2019.3Paul Emrath, Caitlin Sugrue Walter “NMHC-NAHB Cost of Regulations Report.” National Association of Home Builders, National Multifamily Housing Council, 2022.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.