Markets May Be Vulnerable to Stagflation from Russian Invasion

Blog post

February 28, 2022

- Although global markets for now have been resilient in the face of the war in Ukraine, investors may wish to stay vigilant.

- A potential scenario within our stress test includes the fact that the conflict could drive oil prices up and exert stagflationary pressures on U.S. and European economies.

- A diversified portfolio of global equities, bonds and real estate could end up losing 13%, according to our stress test.

What have we seen so far?

Although global markets have not yet reacted that strongly, Russian financial markets have had a larger reaction compared to when the country annexed Crimea in 2014 — in particular after the last round of sanctions by the European Union and the U.S.1 Despite the 39% drop in Russian equities on Feb. 24, the MSCI World Index was virtually flat that same day, and historically safe-haven assets did not gain dramatically.2 The environment continues to change rapidly, however.

Russian financial markets were impacted strongly by Russia's invasion

Russian markets during the annexation of Crimea in 2014 and the current invasion of Ukraine. Day zero is the day before the invasion. The MSCI World Index and MSCI Russia Index (in local currency) and the RUB/USD exchange rate are normalized to 100 on day zero.

Stagflation stress-test scenarios

Economist Mohamed El-Erian recently wrote: "Stagflationary economic forces have already been released. The vast majority of countries and companies around the world are likely to experience some fall in demand and higher input costs."3 With oil prices around USD 100 per barrel, inflation readings high and the global economy still recovering from the COVID-19 pandemic, these stagflationary pressures significantly add to current economic uncertainty and could move global markets. With those conditions in mind, we outline two scenarios for how this geopolitical conflict could impact global diversified multi-asset-class portfolios.4

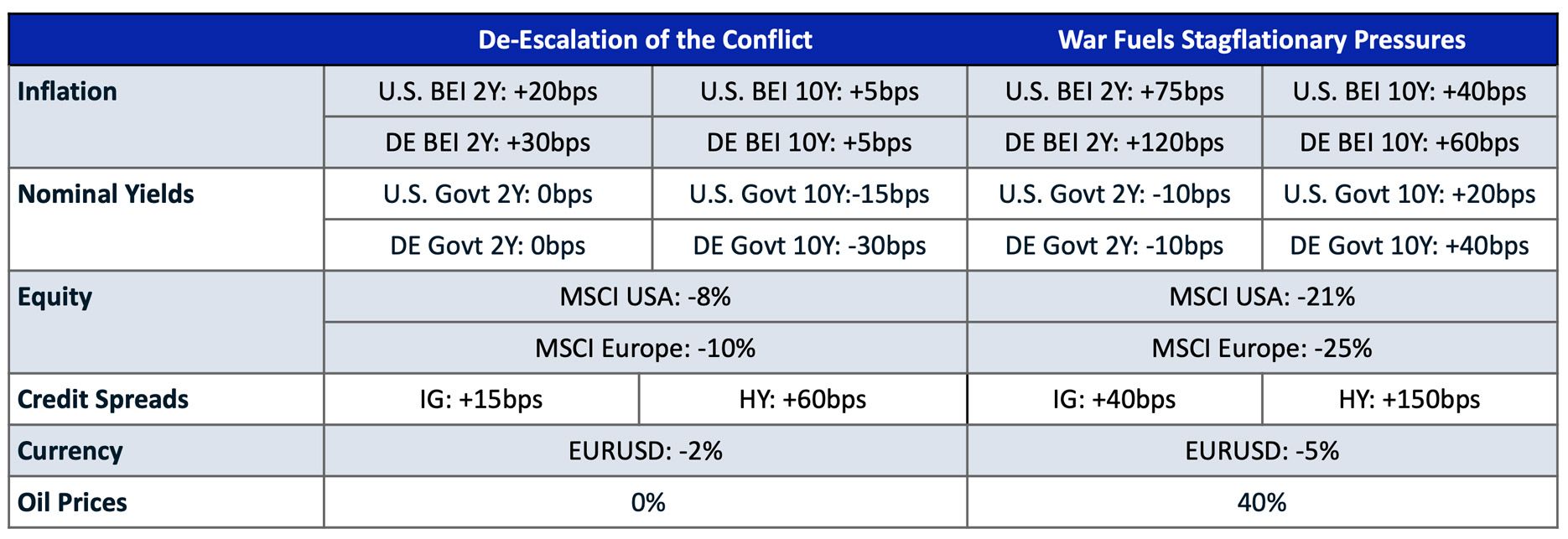

In our optimistic scenario, a ceasefire and de-escalation of the conflict could stabilize energy prices around current levels. Apart from a small short-term impact, there are no persistent inflationary pressures. The hit to economic growth is small, and central banks stick to their plans for tightening monetary policy. The U.S. and German sovereign-yield curves slightly flatten due to slower growth, global equities decline, credit spreads widen and the U.S. dollar strengthens relative to the euro. In the grimmer scenario, the conflict drags on and multiple rounds of long-lasting sanctions are imposed. Energy prices surge to significantly higher levels. Inflation is not only soaring in the short term, but fears of supply-chain bottlenecks push up longer-term inflation expectations. Higher energy prices and lower business and consumer confidence slow economic growth beyond the forecast from the IMF just last month.5 In this scenario, central banks are caught between two fires and cannot postpone monetary tightening for very long. U.S. and German nominal long-term rates go up as long-term inflation expectations rise, but real long-term rates drop as these economies slow down. Equities plunge, credit spreads rise and the U.S. dollar gains versus the euro.

What we assume in our scenarios compared to pre-invasion levels

Scenario assumptions are informed by a combination of our analysis of historical data, external market commentary and subjective judgment. These are not accurate forecasts but hypothetical narratives of how the conflict could affect global multi-asset-class portfolios. Market commentary that has influenced our assumptions: Holland, Ben, Johnson, Scott, Rush, Jamie, Wong, Anna, and Orlik, Tom. "How war in Ukraine threatens the world's economic recovery." Bloomberg, Feb. 25, 2022. "What's next for oil and gas prices as Russia-Ukraine tensions rise?" J.P.Morgan, Feb. 8, 2020. Brower, Derek, Wilson Tin, and Giles Chris. "The new energy shock: Putin, Ukraine and the global economy." Financial Times, Feb. 25, 2022.

Stagflation stress-test results

To assess the potential impact on multi-asset-class portfolios, we created a stress test using MSCI's predictive stress-testing framework to propagate our main assumptions to all other risk factors impacting portfolio returns.6 The exhibit below shows the impact of both scenarios for various asset classes. Note that, while in demand-driven growth slowdowns like the 2008 global financial crisis, U.S. Treasury bonds acted as a cushion to offset losses in equity markets, this time our stress test showed both equities and Treasury bonds could suffer in the stagflationary scenario, as slowing growth coincides with rising prices.

Potential impact across asset classes

Loading chart...

Please wait.

Portfolio impact of the scenarios based on market data as of Feb. 18, 2022. U.S. Treasurys and Treasury inflation-protected securities are represented by Markit iBoxx indexes. Equity markets and corporate bonds are represented by MSCI indexes. Private equity is represented by model portfolios. U.S. real estate is represented by the MSCI/PREA U.S. AFOE Quarterly Property Fund Index. U.K. real estate is represented by the MSCI/AREF UK Quarterly Property Fund Index. The composite portfolio is represented by the following weights: 50% global equities (35% public and 15% private), 10% U.S. Treasurys, 10% U.S. Treasury inflation-protected securities, 10% U.S. investment-grade bonds, 10% U.S. high-yield bonds and 10% U.S. real estate. Source: IHS Markit, MSCI

Although the unfolding tragedy in Ukraine has not rattled global markets, investors remain vigilant. Amid the economic recovery from COVID-19 and high-inflation environment, the U.S. and European economies are vulnerable; and, as noted in the exhibit above, a diversified portfolio of global equities, bonds and real estate could lose 13% under a scenario where stagflationary pressures take the upper hand.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1Martin, Katie, Stubbington, Tommy, and Lockett, Hudson. “Russia sharply increases rates as sanctions send rouble plunging.” Feb. 28, 2022.2Wu, Ethan. “Ukraine is not yet a markets crisis.” Feb. 25, 2022.3El-Erian, Mohamed. “Six factors to guide investors during Ukraine turmoil.” Feb. 26, 2022.4While the Russian financial markets are clearly in distress, this stress test focuses on well-diversified global portfolios. Given the relatively small importance of Russian financial markets in global portfolios (Russia’s weight in the MSCI Emerging Markets Index is only around 3%), we do not stress that market explicitly, but rather focus on modeling the conflict’s direct impact on major global market risk factors.5“World Economic Outlook: Rising caseloads, a disrupted recovery, and higher inflation.” International Monetary Fund, January 2022.6 The results are generated based on this methodology, using MSCI's BarraOne®, whereby we used current correlations to propagate the shocks to a hypothetical multi-asset-class portfolio. MSCI clients can access MSCI’s BarraOne® and RiskMetrics® RiskManager® files for these scenarios on the client-support site.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.