Measuring Climate Impact with Total-Portfolio Carbon Footprinting

- Carbon footprinting across multi-asset-class portfolios allows investors to measure and manage financed emissions on their road to net-zero emissions.

- Comparing the financed emissions of the different asset classes, sectors and project types in the investment portfolio can inform decarbonization decisions.

- For the representative indexes and portfolios, corporate bonds had the highest financed emissions, although there was significant variation between segments of the corporate-bond market.

Defining a standard for carbon footprinting

Under the umbrella of PCAF, financial institutions globally are working on a financed-emissions disclosure standard2 based on accounting rules and in line with the Greenhouse Gas Protocol, a global standard for emission footprints. Following the general financed-emission attribution principle, financial institutions account for their financed emissions from the annual emissions of the company or project they finance,3 proportional to their share of investments in the company or project.4 PCAF recommends the disclosure of Scope 1 and 2 emissions across all sectors and separate disclosure of Scope 3 emissions for selected sectors.5

Breaking down financed emissions by asset class

We analyzed the financed emissions of indexes and representative portfolios worth USD 1 million in global equities and sovereign, corporate and municipal bonds using the MSCI Total Portfolio Footprinting solution. Corporate bonds had the highest total financed emissions — including Scopes 1, 2 and 3 — although there was significant variation between segments of the corporate-bond market. For example, the exhibit below shows that USD high-yield bonds were more emission-intensive than USD investment-grade bonds. Sovereign bonds also registered a large carbon footprint, but we should note that all sovereign emissions are currently lumped together in Scope 1.6

Financed emissions across asset classes varied significantly

Scope 1 and 2 and Scope 3 financed emissions for 1-million-dollar hypothetical portfolios, as of June 15, 2022. A representative universe of municipal bonds is weighted by outstanding market value.

The PCAF standard defines a data-quality scorecard, ranging from 1 for highest to 5 for lowest data quality. Quality score 2 is dominant in terms of the outstanding amount for equities and sovereign and corporate bonds,7 which means that emissions are based on either reported emissions or data on the primary physical activity of the company's energy consumption. For lower data-quality scores, missing emission data is estimated based on the company's production or revenue data or, if that is also unavailable, based on sector averages for emission intensity. For instance, municipal bonds' financed emissions are entirely model-driven. Coverage for the analyzed indexes is more than 99% of the market-capitalization weight.

For instance, sector allocations within asset classes are an important driver of financed emissions. As mentioned before, USD high-yield bonds had a larger footprint compared to their investment-grade counterparts. Using Brinson attribution to examine this difference, we see it was driven by a combination of allocation effects (e.g., a larger allocation to the more emission-intensive energy sector for the USD high-yield index) and selection effects (e.g., a higher emission intensity for the utilities, energy and financial sectors in the high-yield portfolio).

Transparency about data quality

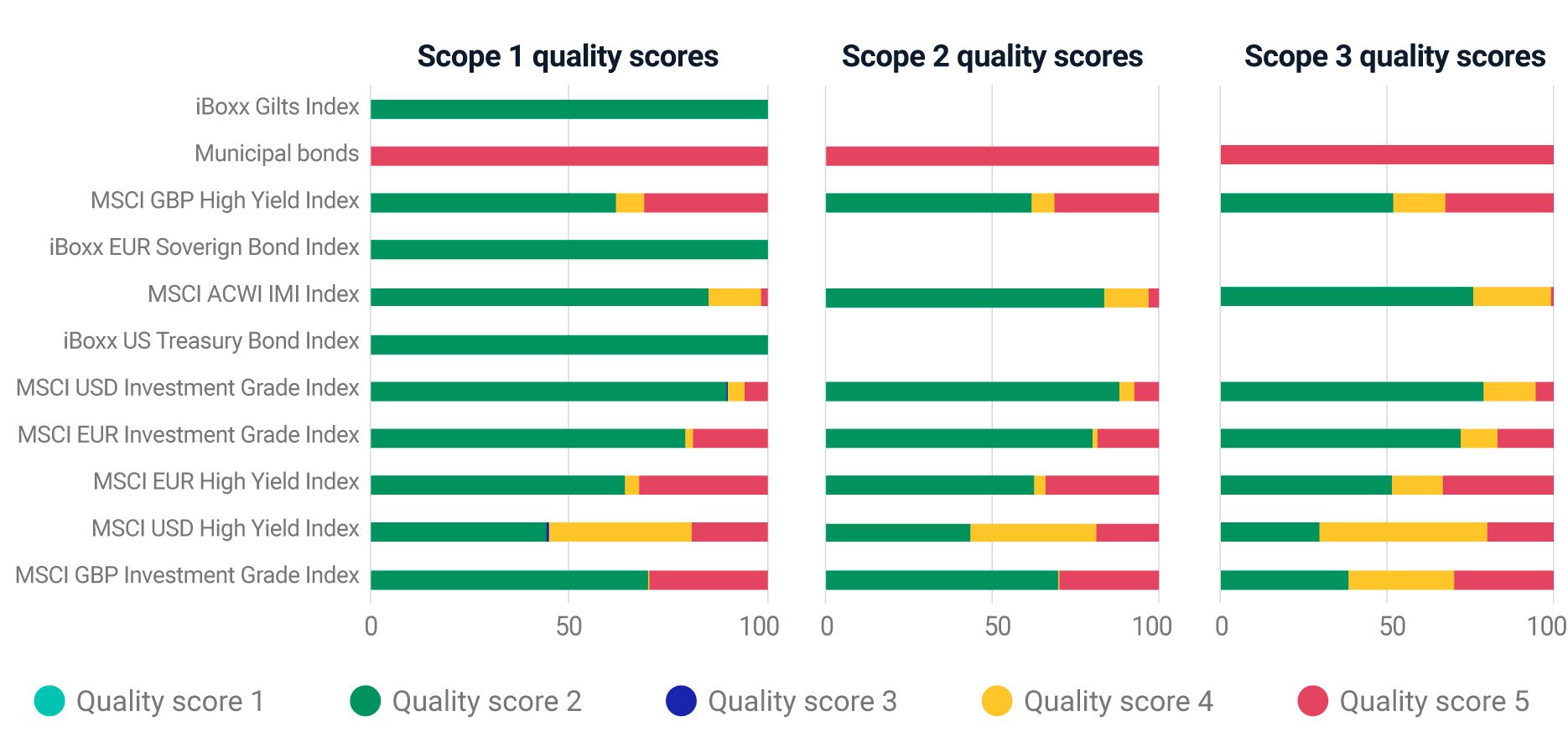

Although the quality of climate-related data reported by issuers is constantly improving, fewer than 40% of companies in the MSCI ACWI Investable Market Index (IMI) disclosed Scope 1 and 2 emissions and fewer than 25% disclosed Scope 3, as of Jan. 20, 2022. Hence, transparency about data quality is key.The PCAF standard defines a data-quality scorecard, ranging from 1 for highest to 5 for lowest data quality. Quality score 2 is dominant in terms of the outstanding amount for equities and sovereign and corporate bonds,7 which means that emissions are based on either reported emissions or data on the primary physical activity of the company's energy consumption. For lower data-quality scores, missing emission data is estimated based on the company's production or revenue data or, if that is also unavailable, based on sector averages for emission intensity. For instance, municipal bonds' financed emissions are entirely model-driven. Coverage for the analyzed indexes is more than 99% of the market-capitalization weight.

Data quality of the underlying financed-emission data

PCAF quality score of Scope 1, 2 and 3 financed emissions of portfolio constituents weighted by outstanding amount in USD. Generally, larger-market-cap issuers report emission data, which explains the larger than 40% market-cap weight of quality-score-2 data. As of June 15, 2022, sorted by total Scope 1, 2 and 3 emissions.Understanding the drivers of financed emissions

Financed emissions not only provide the foundation to set and track net-zero commitments, but to help identify climate-risk drivers in the portfolio across asset classes, sectors and geographies.For instance, sector allocations within asset classes are an important driver of financed emissions. As mentioned before, USD high-yield bonds had a larger footprint compared to their investment-grade counterparts. Using Brinson attribution to examine this difference, we see it was driven by a combination of allocation effects (e.g., a larger allocation to the more emission-intensive energy sector for the USD high-yield index) and selection effects (e.g., a higher emission intensity for the utilities, energy and financial sectors in the high-yield portfolio).

Comparing corporate-bond indexes along sector exposures

Brinson attribution of the difference in financed emissions between the MSCI USD High Yield and MSCI USD Investment Grade Corporate Bond Indexes. As of June 15, 2022. Municipal bonds' emission intensities also varied wildly across different project types. Scope 1 and 3 were the major contributors to our hypothetical municipal-bond portfolio's financed emissions; Scope 2 emissions were an order of magnitude lower. While power utilities were the highest-emitting project type for Scope 1, economic and industrial development and government-related buildings registered the highest Scope 3 financed emissions. The top Scope 2 contributors were energy-consuming facilities such as schools, universities and government facilities.What are the most emission-intensive municipal-bond projects?

Top five contributors by project type in a hypothetical USD 1 million municipal-bond portfolio's financed emissions. As of June 15, 2022.The road to net-zero

Measuring the total financed emissions of financial institutions' broad investment portfolios is an important step toward managing the net-zero journey. Greater transparency into emission intensities across asset classes and sectors may help investors identify opportunities for guiding the decarbonization of their investments and, ultimately, the economy. The authors thank Réka Janosik for her contribution to this blog post. MSCI Total Portfolio Footprinting Net-Zero Alignment: Managing Portfolio Risk Along the Net-Zero Journey Reported Emission Footprints: The Challenge Is Real

Scope 1 and 2 and Scope 3 financed emissions for 1-million-dollar hypothetical portfolios, as of June 15, 2022. A representative universe of municipal bonds is weighted by outstanding market value.

Transparency about data quality

Although the quality of climate-related data reported by issuers is constantly improving, fewer than 40% of companies in the MSCI ACWI Investable Market Index (IMI) disclosed Scope 1 and 2 emissions and fewer than 25% disclosed Scope 3, as of Jan. 20, 2022. Hence, transparency about data quality is key.

The PCAF standard defines a data-quality scorecard, ranging from 1 for highest to 5 for lowest data quality. Quality score 2 is dominant in terms of the outstanding amount for equities and sovereign and corporate bonds,7 which means that emissions are based on either reported emissions or data on the primary physical activity of the company's energy consumption. For lower data-quality scores, missing emission data is estimated based on the company's production or revenue data or, if that is also unavailable, based on sector averages for emission intensity. For instance, municipal bonds' financed emissions are entirely model-driven. Coverage for the analyzed indexes is more than 99% of the market-capitalization weight.

The PCAF standard defines a data-quality scorecard, ranging from 1 for highest to 5 for lowest data quality. Quality score 2 is dominant in terms of the outstanding amount for equities and sovereign and corporate bonds,7 which means that emissions are based on either reported emissions or data on the primary physical activity of the company's energy consumption. For lower data-quality scores, missing emission data is estimated based on the company's production or revenue data or, if that is also unavailable, based on sector averages for emission intensity. For instance, municipal bonds' financed emissions are entirely model-driven. Coverage for the analyzed indexes is more than 99% of the market-capitalization weight.

Data quality of the underlying financed-emission data

PCAF quality score of Scope 1, 2 and 3 financed emissions of portfolio constituents weighted by outstanding amount in USD. Generally, larger-market-cap issuers report emission data, which explains the larger than 40% market-cap weight of quality-score-2 data. As of June 15, 2022, sorted by total Scope 1, 2 and 3 emissions.

Understanding the drivers of financed emissions

Financed emissions not only provide the foundation to set and track net-zero commitments, but to help identify climate-risk drivers in the portfolio across asset classes, sectors and geographies.

For instance, sector allocations within asset classes are an important driver of financed emissions. As mentioned before, USD high-yield bonds had a larger footprint compared to their investment-grade counterparts. Using Brinson attribution to examine this difference, we see it was driven by a combination of allocation effects (e.g., a larger allocation to the more emission-intensive energy sector for the USD high-yield index) and selection effects (e.g., a higher emission intensity for the utilities, energy and financial sectors in the high-yield portfolio).

For instance, sector allocations within asset classes are an important driver of financed emissions. As mentioned before, USD high-yield bonds had a larger footprint compared to their investment-grade counterparts. Using Brinson attribution to examine this difference, we see it was driven by a combination of allocation effects (e.g., a larger allocation to the more emission-intensive energy sector for the USD high-yield index) and selection effects (e.g., a higher emission intensity for the utilities, energy and financial sectors in the high-yield portfolio).

Comparing corporate-bond indexes along sector exposures

Brinson attribution of the difference in financed emissions between the MSCI USD High Yield and MSCI USD Investment Grade Corporate Bond Indexes. As of June 15, 2022.

Municipal bonds' emission intensities also varied wildly across different project types. Scope 1 and 3 were the major contributors to our hypothetical municipal-bond portfolio's financed emissions; Scope 2 emissions were an order of magnitude lower. While power utilities were the highest-emitting project type for Scope 1, economic and industrial development and government-related buildings registered the highest Scope 3 financed emissions. The top Scope 2 contributors were energy-consuming facilities such as schools, universities and government facilities.

What are the most emission-intensive municipal-bond projects?

Top five contributors by project type in a hypothetical USD 1 million municipal-bond portfolio's financed emissions. As of June 15, 2022.

The road to net-zero

Measuring the total financed emissions of financial institutions' broad investment portfolios is an important step toward managing the net-zero journey. Greater transparency into emission intensities across asset classes and sectors may help investors identify opportunities for guiding the decarbonization of their investments and, ultimately, the economy.

The authors thank Réka Janosik for her contribution to this blog post.

Further Reading

Subscribe todayto have insights delivered to your inbox.

1For equities and listed bonds, the methodology relies on the PCAF standard. For sovereign and municipal bonds, it is a proprietary methodology. The methodology for municipal bonds builds on PCAF’s project-finance methodology.2“The Global GHG Accounting and Reporting Standard for the Financial Industry.” Partnership for Carbon Accounting Financials, Nov. 18, 2020.3PCAF outstanding amount for equities is market price times the number of shares, and for corporate bonds the book value of the debt at financial year-end.4For listed assets, enterprise value including cash (EVIC) is recommended by PCAF for measuring total company value. EVIC is defined by the EU Technical Expert Group on Sustainable Finance as the sum of the market capitalization of ordinary and preferred shares at fiscal year-end and the book values of total debt and minorities’ interests. For sovereign bonds, nominal GDP is used to calculate emission intensities. In this blog post, we use the term emission intensity for investment intensity — i.e., emissions over USD invested.5Scope 1 represents direct emissions, Scope 2 emissions are from electricity consumption and Scope 3 emissions originate from the up- and downstream value chain. Disclosure of Scope 3 emissions presents multiple challenges including potential double counting and comparability and reliability issues. Therefore, PCAF advises reporting Scope 1 and 2 emissions separately.6Our analysis is based on PCAF’s draft sovereign-bond methodology, available for public consultation. “Draft new methods for public consultation.” PCAF, November 2021. Currently, MSCI follows the territorial approach for calculating sovereign emissions, and the total Scope 1, 2 and 3 emissions based on countries’ production is reported as Scope 1.7 Verified and unverified emissions are not distinguished in our database at this point, so quality scores 1 (third-party-verified emission data) and 2 are combined under quality score 2. For sovereign bonds’ financed-emission data, PCAF does not prescribe data-quality scoring, but we assign score 2 to it due to its high quality.8Brinson attribution is a performance-attribution methodology based on active portfolio weights. We attributed the difference between financed emissions for USD 1 million portfolios represented by the MSCI USD High Yield and USD Investment Grade Indexes to allocation, selection and interaction effects. For a particular sector, for example, a positive allocation effect for the sector means that the higher financed emissions of the high-yield index can be attributed to its larger allocation to that particular sector than that in the investment-grade index.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.