Measuring Liquidity Risk

Blog post

April 23, 2015

After the global financial crisis of 2008, investors and regulators realized that liquidity risk in multi-asset class portfolios could no longer be overlooked. Too many risk models had assumed ample funding and low trading costs, which contributed to the meltdown. p>

In 2013, MSCI introduced LiquidityMetrics, a flexible suite of measures, in response to emerging liquidity regulation across the entire financial industry. With LiquidityMetrics, MSCI introduced not only a methodology, but also a common language for liquidity risk, which was still missing at the time.

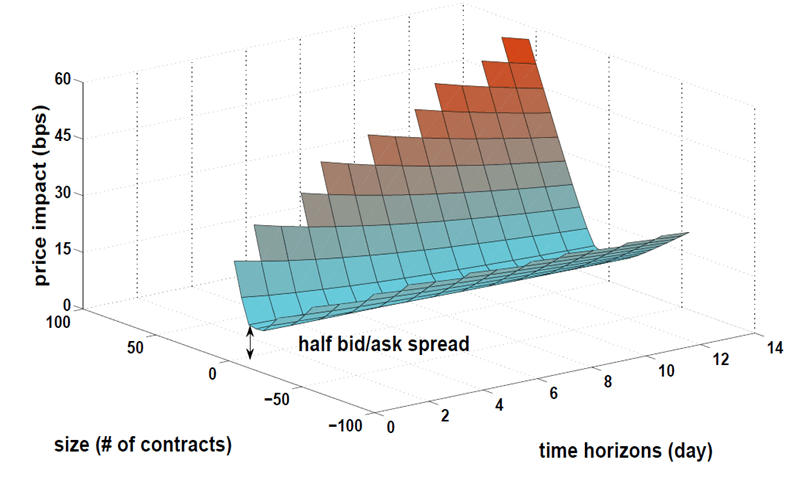

LiquidityMetrics offers portfolio managers and risk professionals a rigorous way to quantify the liquidity risk of financial instruments across all asset classes. LiquidityMetrics looks at an asset's liquidity in its entirety, modelling the interplay between transaction costs, liquidation time horizons and size effects of possible future actions taken on a portfolio. To this end, the liquidity of a given asset is portrayed via its "liquidity surface", defined as the expected transaction cost of an order executed within a specified time horizon (see below exhibit for a hypothetical example).

LiquidityMetrics looks at various aspects of an asset's liquidity, including bid-ask spread, market impact of trades, trading immediacy, market activity and market depth. Available information is employed to describe each asset's liquidity in a way that addresses the multiple dimensions of liquidity, while remaining consistent across multiple asset classes.

An Asset's Liquidity Surface

Applications of the LiquidityMetrics framework are numerous. For example, fund managers can test liquidity of their investments against redemption commitments by estimating the impact of hypothetical redemptions on the net asset value (NAV) of the shares. Attributing this cost to positions, fund managers can profile liquidity across the portfolio, obtaining a liquidity map to support investment decisions. In addition, risk managers can estimate how long it would take to liquidate different portions of a portfolio within specified transaction cost limits, determining time-to-liquidation measures for all positions, as required by several regulators. In contrast, managers can test the capacity of a prospective investment by determining the maximum size that would still satisfy an assigned portfolio liquidity limit.

In short, LiquidityMetrics is a rigorous framework for a quantitative measurement and management of portfolio liquidity, as seen as the interplay between asset liquidity and liquidity commitments. As the above examples suggest, asset liquidity is in turn a trade-off among transaction cost, order size and time horizon effects of a trading activity.

Read the paper, "Introduction to LiquidityMetrics: A Flexible Suite of Liquidity Measures." (Client access only)

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.