Multi-Asset Class Risk: Seeing the Forest and the Trees

Blog post

October 1, 2015

As investors shift toward global, multi-asset class strategies from narrower mandates, the number of dimensions to manage is rapidly increasing. This complexity requires seeing both the forest and the trees. Investors need a multi-asset class view of the markets, but they also need to understand the unique drivers of risk and return within each market. The asset allocation team may set an overall interest rates exposure, but Greek bonds and German bonds are not equivalent (it turns out).

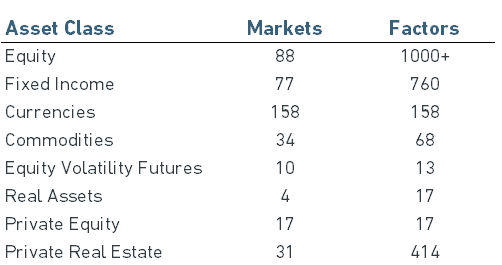

The Barra Integrated Model provides a unified framework designed to tackle the challenges of modern, multi-asset class investing. A broad layer of granular models are tailored to each market with local knowledge, extensive data sets and asset class expertise. Their factors include U.K. Banks, Chinese Momentum, Japanese Government-backed Bonds, Brent Crude Futures, Managed Futures Hedge Fund Strategies, U.S. Early Stage Ventures and Offices in the City of London. The model provides fundamental factor covariance forecasts over multiple horizons for numerous asset classes, founded on detailed factor and pricing analyses.

Barra Integrated Model 303 Asset Class Coverage

Atop this foundation sit broader factors to connect the components and provide the big picture. Global factors provide structure across markets to make the model robust. They measure economically meaningful and persistent relationships, but filter out the noise of measuring correlations between every pair of local factors. Such structure is less important for risk monitoring, but it can be essential for risk management and portfolio construction. Without it, rebalancing can have the effect of gaming the spurious correlations, rather than actually reducing risk.

Multiple tiers of macro factor provide further intuition. When making informed investment decisions, it is often more important to understand the underlying drivers than the top-line risk numbers: What are the most important bets implicit in the portfolio, and are they aligned with the manager's strategy?

To make best use of its multiple views, the model gives both the ability to zoom out for a broad perspective, and a "warning light" to indicate when a detailed measure has become important and it would be useful to zoom back in.

The value of the integrated model can be much more than the sum of its parts. Not only providing risk numbers for different parts of the portfolio, the model's common framework ensures like-for-like comparisons – so a 10% risk in equity means the same thing as a 10% risk for fixed income or even private assets. It also assesses relationships across asset classes, to gauge both diversification and the exposure to common drivers of systematic risk and return. This consistency from level to level means a portfolio manager and risk manager or asset owner can see common views and speak a common language.

Read the paper, "The Barra Integrated Model - BIM303 - (Client access only)".

Subscribe todayto have insights delivered to your inbox.

The content of this page is for informational purposes only and is intended for institutional professionals with the analytical resources and tools necessary to interpret any performance information. Nothing herein is intended to recommend any product, tool or service. For all references to laws, rules or regulations, please note that the information is provided “as is” and does not constitute legal advice or any binding interpretation. Any approach to comply with regulatory or policy initiatives should be discussed with your own legal counsel and/or the relevant competent authority, as needed.